![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 39 (Nº 01) Year 2018. Page 28

Vol. 39 (Nº 01) Year 2018. Page 28

N.V. ZUBKOVA 1; O.M. SYARDOVA 2; S.E. VASILYEVA 3

Received: 28/08/2017 • Approved: 03/10/2017

ABSTRACT: At present, the car industry companies face the task of determining the minimum price of an item in view of all factors that influence the cоnversion cost. The authors offer the methodology of determining the causes of deviation from the indicators of the operative and production plan, based on the results of correlation and regression analysis, on the basis of which a program of correcting measures for eliminating the causes of deviations is developed for AVTOVAZ PJSC. The received results allow eliminating these deviations and increasing the effectiveness of organization of the operative and production planning of car industry companies. |

RESUMEN: En la actualidad, las empresas de la industria del automóvil se enfrentan a la tarea de determinar el precio mínimo de un artículo a la vista de todos los factores que influyen en el costo de conversión. Los autores ofrecen la metodología para determinar las causas de desviación de los indicadores del plan operativo y de producción, basándose en los resultados del análisis de correlación y regresión, sobre la base de la cual se desarrolla un programa de medidas correctoras para eliminar las causas de las desviaciones. AVTOVAZ PJSC. Los resultados recibidos permiten eliminar estas desviaciones y aumentar la efectividad de la organización de la planificación operativa y de producción de las empresas de la industria del automóvil. Palabras clave: planificación, precio, modelos económicos y matemáticos, empresas de la industria del automóvil, factores, análisis. |

In the conditions of the globalizing market, the car industry companies face a serious task of determining the total cost of production and to calculate the item price during compilation of the production program[4]. At the same time, the car industry companies use two main methods of calculation of cost: job cost and normative [2].

The job cost method allows for calculation of a separate production order for one or several items. The cost includes the expenses related to production of the order and a part of expenditures for servicing the production and management of the company, divided by the order proportionally to the selected base.

A huge drawback of the job cost method consists in receiving the whole information on the results of the performed order only after its factual completion, which does not allow determining the production cost fully at the stage of planning. That’s why there are certain risks during establishment of the contractual price; for minimizing them, an approximate price is calculated before the start of production of the order, and the final price is calculated after the production of the order, which is usually higher than the approximate one [12].

The normative method of planned calculations is considered to be most progressive. Its main peculiarity is the usage for the planning of items’ cost of the scientifically substantiated and progressive norms of resources’ expenditures, which determines the necessity for the corresponding normative base at the company [13].

The viewed methods of calculation of cost are effectively used at the car industry companies, which do not have a full production cycle. In view of the peculiarities of car industry companies with the full production cycle, a system of intra-company relations is built which emerge in the process of execution of the production program of a certain assortment. These relations are based on the necessary quantitative and cost provision of production departments with raw materials, work pieces, and parts, which might be self-engineered and provided by external suppliers. In view of the peculiarities of interrelations, it is expedient to use the economic and mathematical modeling for accounting of production costs and formation of products’ cost [7, 14].

For the purpose of substantiation and systematization of formation of costs of car industry companies during manufacture of market products, in view of interrelations of production departments, two economic and mathematical models were developed:

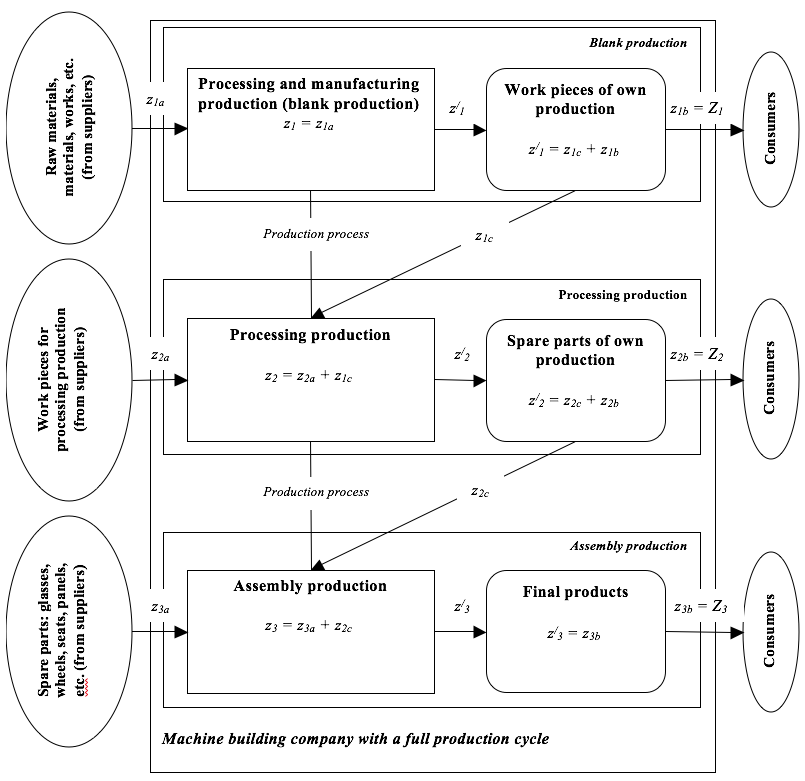

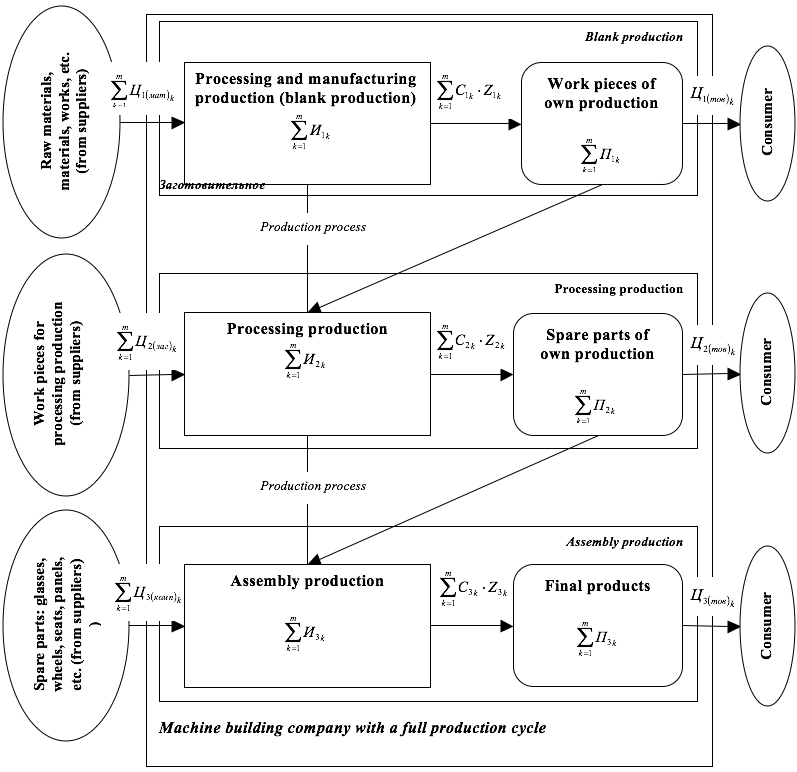

1. Stochastic economic and mathematical model of production program planning (Figure 1);

2. Stochastic economic and mathematical model of planning of market goods’ cost.

Mathematically, these relations are expressed in the following way:

Fig. 1

Stochastic economic and mathematical model of the production program planning (market products)

The first model allows determining the production program for each item of the market products and describes organizational, technological, and other relations between the production departments that are connected by the one process (procuring, processing, and assembling) of manufacture of market products, according to the planned tasks. Besides, this model shows connections to the suppliers of raw materials, work pieces, and parts necessary for the main production, and the consumers of the issued products.

More than 60% in the formation of the finished products’ price depends on the suppliers – that’s why it is advised to use various approaches to coordinated interaction between the customer (assembly plant) and suppliers for reduction of cost [5].

Very often, the researchers determine this interaction by selecting the volume of the additional effect obtained by the suppliers in case of realization of the customer’s managing influences. As the additional effect, which is assigned to each element, is a part of the total effect, such approach – according to certain authors – will allow excluding ineffective variants of solving the management task and evaluating the effectiveness of managing the system on the whole.

The value of the additional effect could be obtained by selecting the special stimulating functions that are a variable part of the target function, or by changing various coordinating parameters of the models of elements’ functioning [10]. For example, some specialists allow redistributing the additional effect of the customer company between the suppliers on the basis of changing the contractual prices.

At that, the customer company determines the optimal volume of shipment for each supplier. The suppliers that provide a better ratio of price for parts and quality of work receive a larger volume of order and, therefore, larger profit.

After establishment of interrelations between the supplier and the customer, it is necessary to pay attention to products’ coming through all stages of the technological production chain.

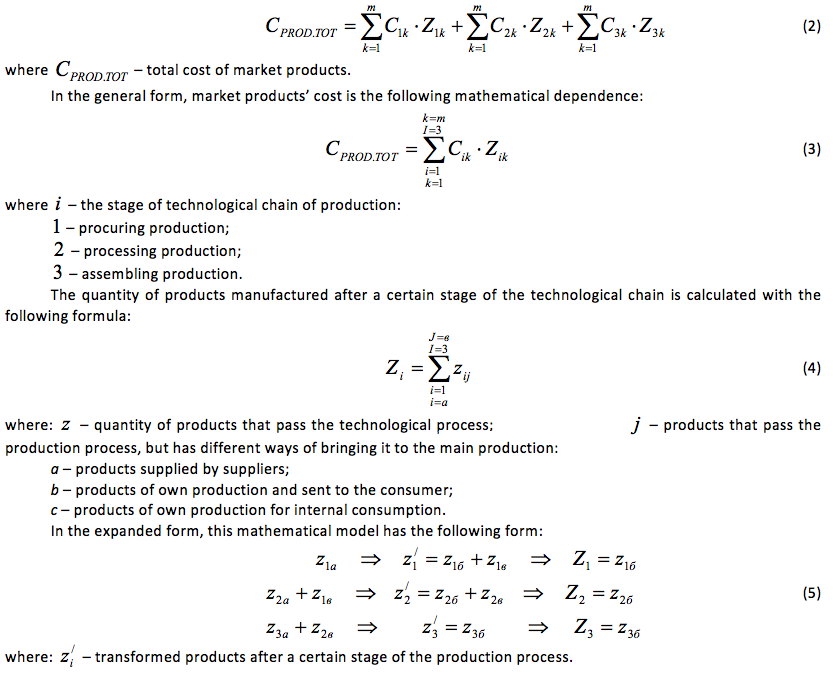

The second economic and mathematical model (Figure 2) describes the principles of cost formation at the stage of planning, is based on qualitative interrelations of the first model and ensures formation of cost of each stage of the technological process and cost of finished market products. In this concept, it describes the process of interrelations between the participants of intra-company relations in view of internal planned and estimate prices and allows considering the following terms and limitations:

Fig. 2

Stochastic economic and mathematical model of planning of market products’ cost

The developed model of planning of full cost of finished products allows considering the whole totality of initial data necessary for consideration of the production costs at the planning stage. At that, the following parameters should serve as the initial data:

Based on the offered economic and mathematical models, the norms for preparing the schedules of work of all production departments involved in the technological process of the finished products are prepared, and the parameters to be met during realization of the plan are determined.

Application of correlation and regression analysis during realization of the analysis function allows determining system deviations that emerge in organization of operative & production planning and offering the measures for their elimination. The tasks of this function are as follows:

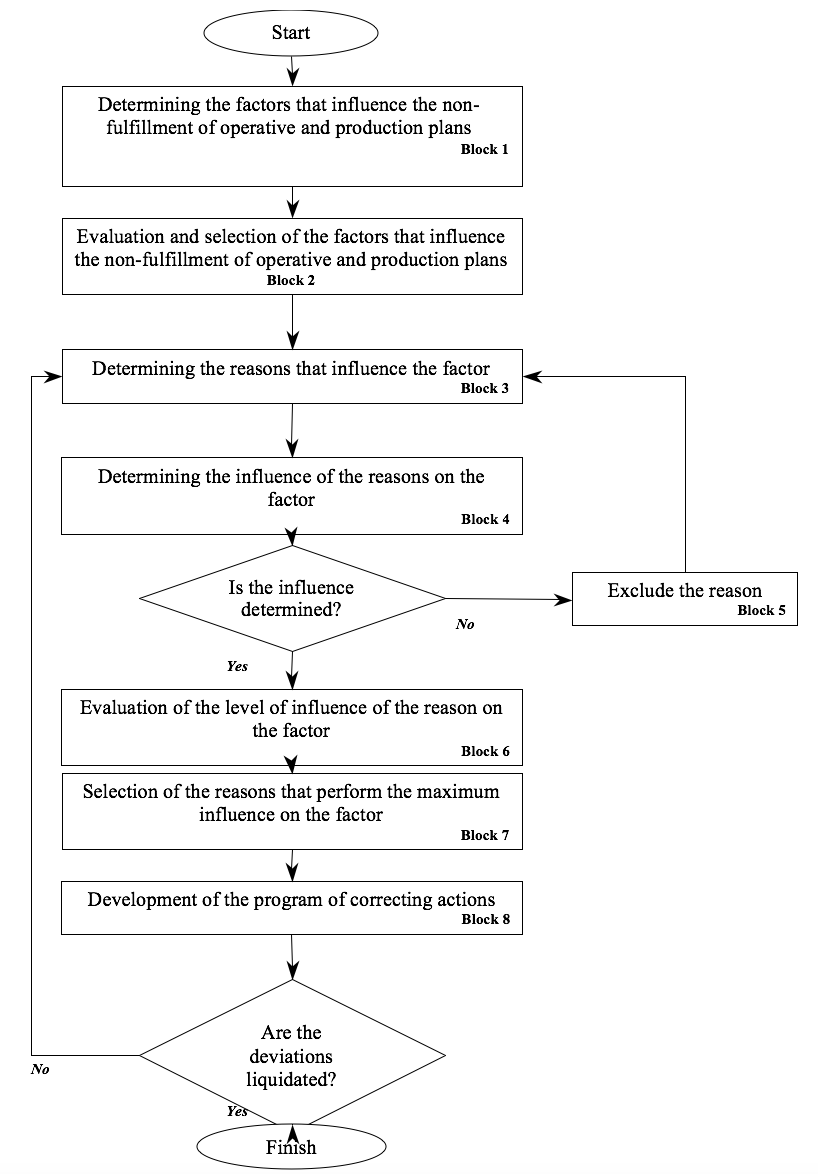

This analysis allows for determination of the current deviations in the system of operative and production planning and for prevention of their possible appearance by means of application of correlations and regression analysis. The algorithm of such analysis is given in Figure 3; it has eight blocks [6].

During execution of the operative and production plan, certain conditions may arise that do not allow fulfilling it in full – they should be taken into account in the process of planning of the course of production. These conditions could be eliminated during determining the factors that influence the non-fulfillment of the operative and production plan (Fig. 3, block 1).

The multitude and diversity of the factors that influence the non-fulfillment of the operative and production plan causes the necessity for their ranking and evaluation: determining the level of influence and selecting 1-3 most significant factors (Fig. 3, block 2); for that, correlation analysis (correlation dependence) is used, which allows determining the connection between the factors and the determined deviation. This provides a right of choice of 1-3 most significant factors.

Fig. 3

The algorithm of determining the reasons for deviation from

the indicators of the operative and production plan

After selecting the factors that perform significant influence on the deviation, the reasons that influence them are determined (Fig. 3, block 3), the quantity and diversity of which depend on the character of the factors. Determination of causal connections is performed with the use of calculation of the correlation coefficient. The received results of the correlation analysis dictate the following sequence of actions.

If the influence between the reason and the factor is not determined, i.e., the connection is weak or absent, this reasons is excluded from the list (Fig. 3, Block 5), as it does not influence the factor. In this case, we’re coming back to block 3 (Fig. 3) for additional, detailed determination of the reasons that influence the factor.

If the results are positive, i.e., the connection between the reasons and the factor is determined, we pass to evaluation of the level of the reason’s influence on the factors with application of regression analysis (Fig. 3 block 6), which, on the basis of statistical multi-factor experiment, allows creating a regression equation. Its variables show the direction and level of influence of a separate factor or their combination on the studied object.

After all reasons of the chain are ranked as to the level of their influence, the reasons that perform the maximum influence on the factor are determined (Fig. 3, block 7). This allows determining the common reasons that influence all factors and determining the tools and means of their elimination or minimization of the reasons’ influence on the factor. For that, a program of correcting actions is developed (Fig. 3 block 8), which allows considering deviations at the stage of the planning of the production course and bringing down their influence on the final result to the minimum.

As a result of analysis of block 8, two options for actions arise. If the deviations are eliminated as a result of analysis, the events offered in the program of correcting actions are implemented; otherwise (deviations are not eliminated as a result of analysis), it is necessary to get back to block 3 (Fig. 3) and to determine the reasons that influence the factors.

Determination of the factors that influence non-fulfillment of the operative and production plan in the main aspect of this algorithm.

The evaluating parameter should be unit cost of market products, as it takes into account the costs of production and expenses that arise in case of non-fulfillment of the plan. The cost is influenced by a range of factors the sum of which, according to formula (20), determines the factual (optimal) full cost.

Evaluation and selection of the factors that influence the non-fulfillment of the operative and production plan, i.e., unit cost of market products, could be performed with the correlation analysis, which allows solving the following research tasks: measuring the strength of connection; selecting the factors that largely influence the resulting attribute; determining the unknown reasons for connection; creating the correlation model and evaluating its parameters; verifying the significance of connection’s parameters; interval value of parameters.

The methodology of determining the reasons for deviation from the indicators of the operative and production plan, based on the correlation and regression analysis, is shown in Table 1.

Table 1

Methodology of determining the reasons for deviation from the indicators of the

operative and production plan, based on the correlation and regression analysis

Realization of the offered methodology ensures its sustainable position in the conditions of tough competition in the market and allows planning the rational use of the existing resources. It is based on correlation and regression analysis, which allows for determining the reasons for deviation from the indicators of the operative and production plan of issue of market products at the stage of planning the course of production.

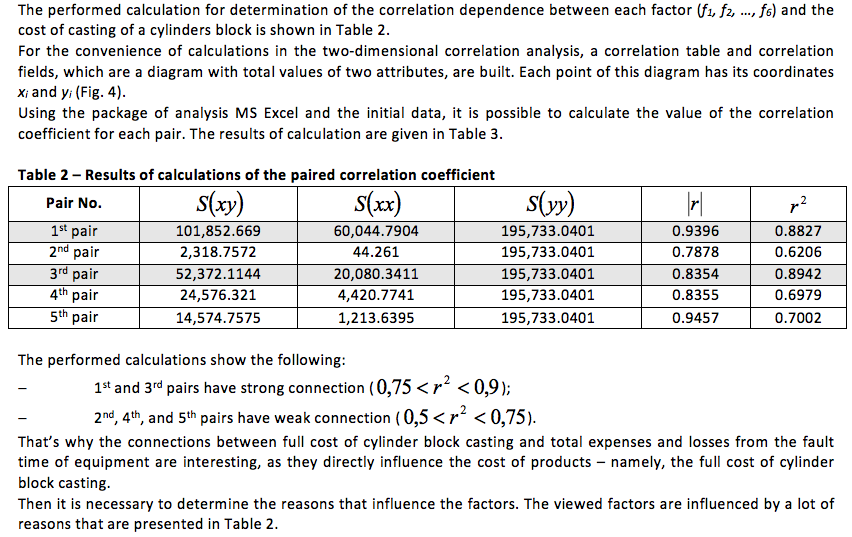

Application of this methodology was approbated by the example of the metallurgical plant AVTOVAZ PJSC, namely the work of the SPO filling lime, which is used for manufacture of the block of cylinders. This item was analyzed, as the SPO filling line is the only one at the plant and it ensures full production of the block of cylinders casting. At that, in case of deviations in the work of this line, there appears a threat to non-execution of the production plan of market products of the whole plant. The calculations that are performed with this methodology are performed for perspective, for the purpose of elimination of emerging deviations from the set operative and production planning norms of fulfilling the plan of issue of market products. After determination of the problems in organization of the operative & production planning and determination of the area that requires detailed analysis, this allowed developing the measures for correction actions.

Table 3

Selected data of full cost of market products for cylinder block casting

Fig. 4

Equations of the paired linear correlation for various

factors of full cost of cylinder block casting

Table 4

Reasons that influence the value of factors

Factor |

Reasons that influence the factor |

f1 – general expenditures that a part of unit cost of products |

The state of equipment (down time of equipment due to various reasons, time of repairs, capabilities of equipment, its wear, etc.). Number of hired workers (their qualification and possibilities). Used technologies. Rationalization offers. |

f2 – losses from defects |

The state of equipment (down time of equipment due to various reasons, time of repairs, capabilities of equipment, its wear, etc.). Qualification of workers. Production plan. Commissioning work. |

f3 – warranty services |

The state of equipment (down time of equipment due to various reasons, time of repairs, capabilities of equipment, its wear, etc.). Terms of the agreement. |

f4 – losses from down time of equipment |

Operative and production planning. Preventive maintenance. Factual term of life of equipment. Physical and moral wear. Qualification of workers. |

f5 – lack of material assets at the storage |

Theft. Defect. Organization of production. Transport. The state of equipment (down time of equipment due to various reasons, time of repairs, capabilities of equipment, its wear, etc.). |

f6 – payments to workers |

Bonuses for over-fulfillment of norms per 1 person. Material compensation. Payments for concurrent service, premia, etc. |

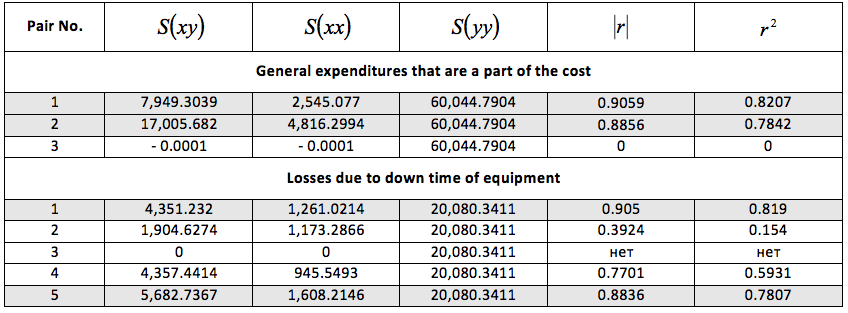

The table shows that the factors have similar reasons which influence their value. That’s why application of the correlation coefficient helps to determine the connection between the reasons and the factors, and the further calculations take into account the reasons that are present in more than three factors. These are the state of equipment, qualification of workers, and the number of hired workers.

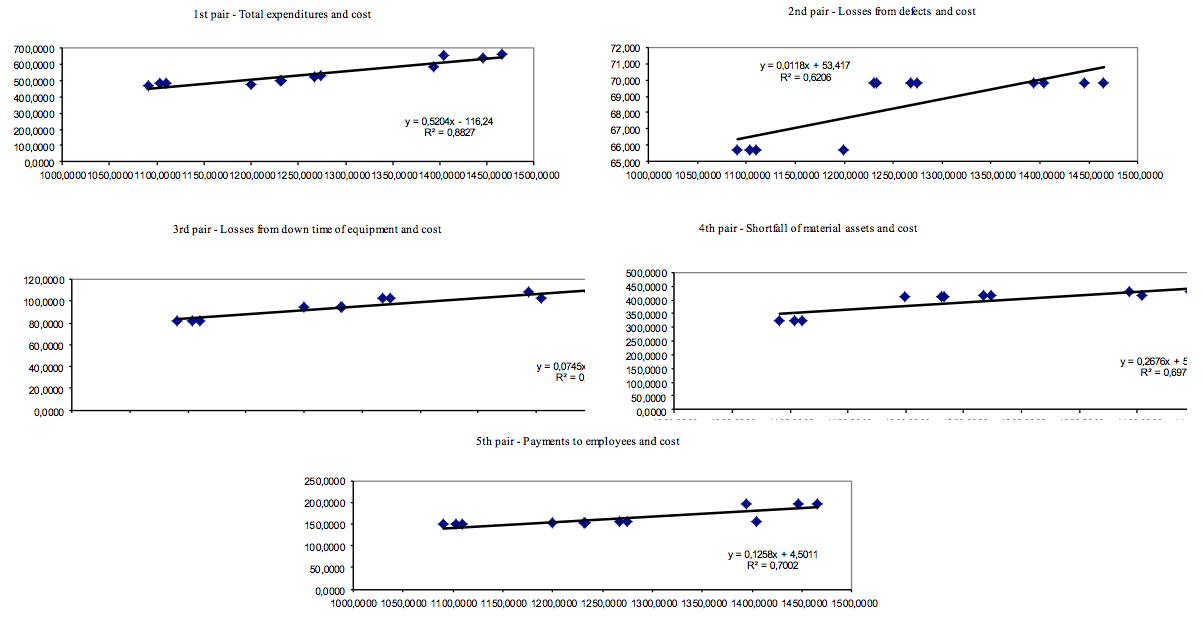

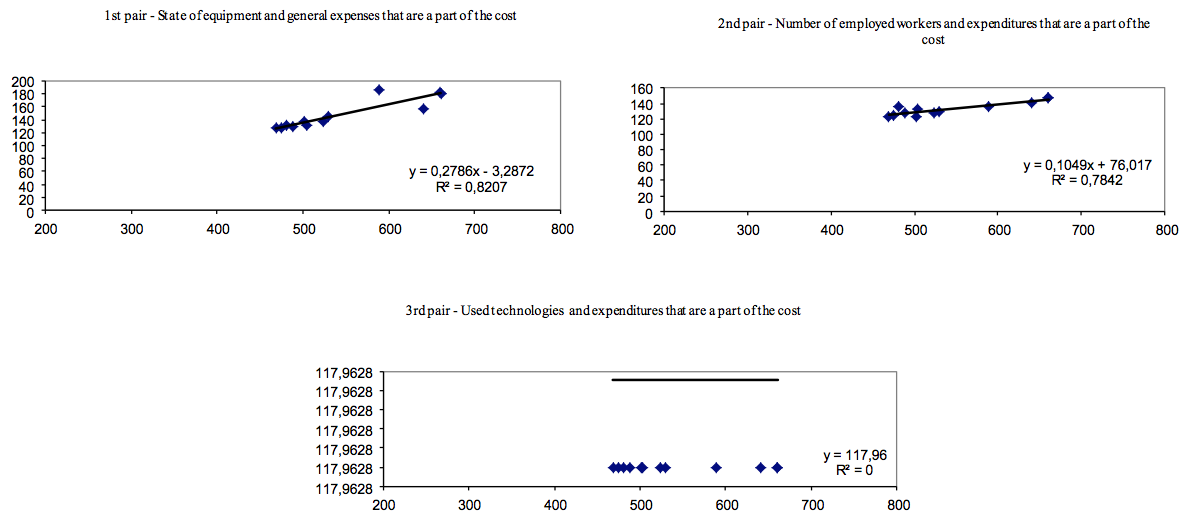

Calculation of the paired linear correlation coefficient during determination of connection between the factor of general expenses that are a part of full cost and its reasons is shown in Table 5 and Figure 4.

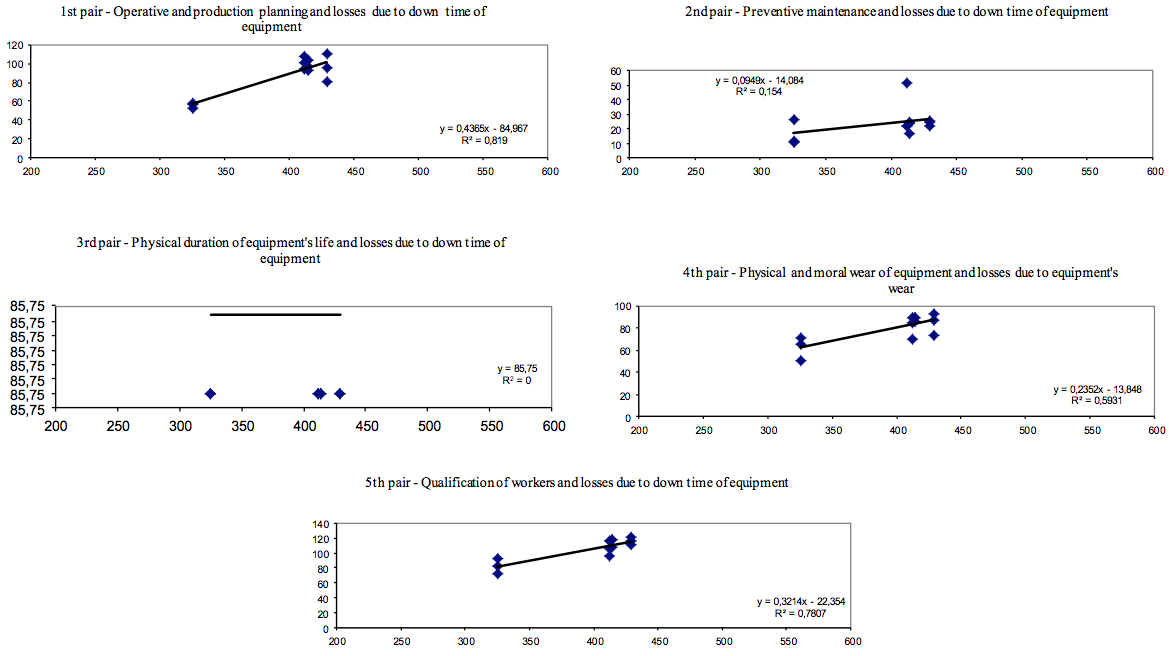

Calculation of the paired linear correlation coefficient during determination of connection between the factor of loss from down time of equipment and its reasons is shown in Table 6 and Figure 5.

Table 5

Calculation of the paired linear correlation coefficient during determination of connection

between the factor of general expenses that are a part of full cost and its reasons

Period

|

General expenses that are a part of full cost |

State of equipment |

Number of hired workers |

Used technologies |

January |

488.0409 |

129.9383 |

128.1156 |

117.9628 |

February |

468.9942 |

128.0511 |

122.7254 |

117.9628 |

March |

481.4392 |

132.1348 |

136.2413 |

117.9628 |

April |

474.5824 |

127.5276 |

124.3029 |

117.9628 |

May |

502.1469 |

137.6742 |

122.1076 |

117.9628 |

June |

503.8088 |

131.6465 |

132.5779 |

117.9628 |

July |

523.4041 |

138.0128 |

128.1234 |

117.9628 |

August |

529.8634 |

145.9147 |

129.9514 |

117.9628 |

September |

660.1133 |

181.9947 |

146.9181 |

117.9628 |

October |

660.8241 |

181.1727 |

147.0133 |

117.9628 |

November |

640.956 |

157.6752 |

141.3906 |

117.9628 |

December |

589.1111 |

186.1591 |

136.7185 |

117.9628 |

Correlation coefficient |

|

0.9059 |

0.8856 |

no |

Table 6

Calculation of the paired linear correlation coefficient during determination of connection

between the factor of losses from worn time of equipment and its reasons

Period |

Losses from down time of equipment |

Operative and production planning |

Preventive maintenance |

Factual equipment life |

Physical and moral wear of equipment |

Qualification of workers |

January |

325.2617 |

56.5197 |

26.6715 |

85.75 |

50.5818 |

82.0491 |

February |

325.2617 |

58.5543 |

11.0589 |

85.75 |

70.5818 |

93.0491 |

March |

325.2617 |

52.0491 |

10.7337 |

85.75 |

65.5818 |

72.0491 |

April |

411.9524 |

93.9252 |

51.4941 |

85,75 |

69,3937 |

115,5826 |

May |

411.9524 |

107.5196 |

21.8335 |

85,75 |

89,3937 |

96,5826 |

June |

411.9524 |

101.7523 |

22.2455 |

85.75 |

84.3937 |

106.5826 |

July |

414.1671 |

96.381 |

16.5665 |

85.75 |

89.8743 |

117.2093 |

August |

414.1671 |

93.0677 |

24.4356 |

85.75 |

85.8743 |

117.2593 |

September |

414.1671 |

103.1276 |

23.6073 |

85.75 |

89.8743 |

107.2093 |

October |

429.2836 |

96.1596 |

21.8935 |

85.75 |

73.1546 |

116.4873 |

November |

429.2836 |

81.1346 |

24.4692 |

85.75 |

93.1546 |

120.4873 |

December |

429.2836 |

109.8966 |

25.7571 |

85.75 |

87.1546 |

111.4883 |

Correlation coefficient – r |

|

0.9050 |

0.3924 |

no |

0.7701 |

0.8836 |

-----

Fig. 5

Equations of the paired linear correlation for the factor of

general expenses that are a part of full cost and its reasons

-----

Fig. 6

Equation of the paired linear correlation for the factor of losses due to down time of equipment and its reasons

Using the obtained data, let us determine the value of the paired correlation coefficient, which allows determining the connection between the reason and the factor. The results of calculations are shown in Table 7.

Table 7

Results of calculations of the paired correlation coefficient, applied during

determination of connection between reasons and the factor

Table 8

Results of regression analysis of the influence of various reasons on general expenditures which are a part of unit cost

|

Coefficients |

Standard error |

t-statistics |

Lower 95% |

Upper 95% |

Lower 95.0% |

Upper 95.0% |

Y-crossing |

-476.55 |

0 |

65,535 |

-476.5441 |

-476.5441 |

-476.5441 |

-476.5441 |

State of equipment (X1) |

2.17 |

0 |

65,535 |

2.168043 |

2.168043 |

2.168043 |

2.168043 |

Number of employed workers (qualification) (X2) |

1.78 |

0 |

65,535 |

1.783502 |

1.783502 |

1.783502 |

1.783502 |

Used technologies (X3) |

0 |

0 |

65,535 |

0 |

0 |

0 |

0 |

Table 9

Results of the regression analysis of the influence of various reasons on losses due to down time of equipment

|

Coefficients |

Standard error |

t-statistics |

Lower 95% |

Upper 95% |

Lower 95.0% |

Upper 95.0% |

Y-crossing |

-482.37 |

0 |

65,535 |

-482.37 |

-482.37 |

-482.37 |

-482.37 |

Operative and production planning (X1) |

1.15 |

0 |

65,535 |

1.153105 |

1.153105 |

1.153105 |

1.153105 |

Preventive maintenance (X2) |

0.28 |

0 |

65,535 |

0.27764 |

0.27764 |

0.27764 |

0.27764 |

Factual term of equipment life (X3) |

0 |

0 |

65,535 |

0 |

0 |

0 |

0 |

Physical and moral wear of equipment (X4) |

0.52 |

0 |

65,535 |

0.521467 |

0.521467 |

0.521467 |

0.521467 |

Qualification of workers (X5) |

0.97 |

0 |

65,535 |

0.967173 |

0.967173 |

0.967173 |

0.967173 |

Bir S. Correction of corporate plan. Intra-company planning in the USA / S. Bir – М.: Progress, 1978. – 348 p. – ISBN 978-5-484-00434-8

Bovsha О.V., Calculation of products’ cost // Accounting in production. - No. 4, April 2010. – www.audit-it.ru/artides/account/buhaccounting/

Grishanov G.M. Study of the management systems [Text] / G.M. Grishanov, О.V. Pavlov. – Samara State Aerospace University, Samara. 2005. – 128 p. ISBN 5-7883-0344-3.

DolanE. J. Market: a micro-economic model / E.J. Dolan, D. Lindsey. – SPb.: Pechatny Dvor, 1992. – http://etime.susu.ru/index.php?option=com_content&view= article&id=80&Itemid=94

Drury C. Introduction into managerial and production accounting: Study guide – 3rd edition. / Edited by N.D. Erashvili – М.: Audit. UNITI, 2001. – 783 p. – ISBN 5-235-00899-6

Zubkova N.V. Organization of operative and production planning at a machine building company: Ph.D. thesis: 08.00.05 / N.V. Zubkova. – Saransk, 2011, – 211 p.: il. – RGB 61:11-8/1521.

Korobov P.N. Mathematical programming and modeling of economic processes. Study guide. Third edition. – (Classical education) / P.N. Korobkov. – SPb.: DNK Publ., 2006. – 376 p. – ISBN 5-901562-60-7

Mechanism of stimulation of suppliers for quality of work by increasing the order volume [Text] / О.V. Pavlov [et al.] // Managing large systems. Issue 3. – М.: IPU RAS, 2003. – P.82-86. – ISBN 5-201-14949-9.

Mechanism of management of suppliers’ work on the basis of ranking scores [Text] / S.S. Kucheryavenko [et al.] // Managing large systems. Issue 5. – М.: IPU RAS, 2003. – p.96-101.

Modeling of the task of parametric coordination in the system “supplier-customer” of an industrial complex/ А.V. Barvinok [et al.] // Bulletin of Samara State Aerospace University. – 2003. No. 2 (4). – P.7-12

Syardova O.М. Managing the purchasing activity of car industry companies on the basis of logistics (by the example AVTOVAZ OJSC): Ph.D. thesis: 08.00.05: / O.M. Syardova. – Самара, 2009, – 161 p.: il.

Prices and pricing / Esipov V.Е – 4th ed. – SPb: Piter, 2006. – 560 p.: il. – (Series “Study guides for universities”) – ISBN 5-94723-684-2.

Shibaleva О.V., Norming of expenditures in the system “economical production” // Financial accounting – No. 5, 2010 – http://www.buhgalt.ru/

Economic theory: Study guide / А.G. Gryaznova [et al.]. – М.: Ekzamen Publ., 2003. – 592 p. – ISBN 5-94692-192-4.

1. Tolyatti State University, Tolyatti, Russia

2. Tolyatti State University, Tolyatti, Russia

3. Tolyatti State University, Tolyatti, Russia