![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 39 (# 06) Year 2018. Page 29

Aliya Serikbaevna DOSMANBETOVA 1; Yengilik Dosjanovna BAISHEVA 2; Nursulu Sultaniyarovna NURKASHEVA 3

Received: 30/11/2017 • Approved: 15/11/2017

ABSTRACT: This article contains researches on applying international financial reporting standards in the Republic of Kazakhstan. The goal of this research is to consider prospects of applying new IFRS (International Financial Reporting Standard) taking into account factors of indefiniteness at Kazakh enterprises. The research included the following main tasks: • To consider the process of IFRS becoming in the Republic of Kazakhstan, • To analyze indicators of applying and problems of developing IFRS in the Republic of Kazakhstan, • To reveal the main risks and indefiniteness of the Kazakh financial system functioning, and • Based on generalizing opinions of the expert community, to define advantages and disadvantages of applying new IFRS when forming financial reporting in the context of growing risks and indefiniteness. As a result of the researches, the following conclusions have been made: • Kazakhstan has already carried out a number of progressive reforms in the corporate financial reporting, such as public financial reporting, and introduction of three-level system of financial reporting, as well as change of the audit regulation; it is gradually moving to creating a system of audit and control of certified professional associations. • Implementation of IFRS has a positive impact on the quality of financial reporting, improves the veracity and transparency of the provided information. • Standards of the Kazakh legislation comply with international or national financial reporting standards. However, risk management is not a top priority task of the Kazakh legislation in the area of accounting and financial reporting. • In the context of the growing global risks, accounting and objective estimation of indefiniteness of Kazakh enterprises functioning, including inadequacy of the real economic situation, incompatibility of information, incoherence of regulation, etc. acquire a special urgency. |

RESUMEN: Este artículo contiene investigaciones sobre la aplicación de normas internacionales de información financiera en la República de Kazajstán. El objetivo de esta investigación es considerar las perspectivas de la aplicación de nuevas NIIF (Norma Internacional de Información Financiera) teniendo en cuenta los factores de indefinición en las empresas kazajas. La investigación incluyó las siguientes tareas principales: • Considerar el proceso de adopción de las NIIF en la República de Kazajstán, • Analizar los indicadores de aplicación y los problemas de desarrollo de las NIIF en la República de Kazajstán, • Revelar los principales riesgos e indefinición de la República de Kazajistán funcionamiento del sistema financiero, y • Basado en opiniones generalizadas de la comunidad de expertos, para definir las ventajas y desventajas de aplicar nuevas NIIF cuando se forman informes financieros en el contexto de riesgos crecientes e indefinición. Como resultado de las investigaciones, se han llegado a las siguientes conclusiones: • Kazajstán ya ha llevado a cabo una serie de reformas progresivas en los informes financieros corporativos, como informes financieros públicos, y la introducción de un sistema de informes financieros de tres niveles, así como como cambio de la regulación de auditoría; gradualmente se está moviendo hacia la creación de un sistema de auditoría y control de asociaciones profesionales certificadas. • La implementación de las NIIF tiene un impacto positivo en la calidad de los informes financieros, mejora la veracidad y la transparencia de la información proporcionada. • Las normas de la legislación kazaja cumplen con las normas de información financiera internacionales o nacionales. Sin embargo, la gestión del riesgo no es una tarea de máxima prioridad de la legislación kazaja en el área de la información contable y financiera. • En el contexto de los crecientes riesgos globales, la contabilidad y la estimación objetiva de la indefinición de las empresas kazajas que funcionan, incluida la insuficiencia de la situación económica real, la incompatibilidad de la información, la incoherencia de la regulación, etc. adquieren una especial urgencia. |

Globalization creates conditions for global economies contingence and forming the unified economic space where its members will apply the unified system of financial accounting and reporting (Ivanchenkova and Perevedentseva 2017).

In accordance with the global changes of accounting standards, financial reporting standards have also been improved in the Republic of Kazakhstan. Kazakhstan is a developing economy that is strongly liberalized. The country moved from the centralized bureaucratic planning applied in the post-Soviet area, refused from trade barriers, reduced the number of state enterprises, and formed the financial sector to contribute to the growth of private capital movement. The increase in the inflow of direct investments in the country’s economy caused the need to provide accountability of Kazakh enterprises to international investors and made IFRS an important issue for corporations and regulating bodies.

Over the recent decade, Kazakh enterprises have paid special attention to generalizing and estimating business practice of accounting and implementing top quality accounting standards on the international level, as well as financial reporting in accordance with international standards. Accounting standards are an important infrastructure on the capital markets used by investors when taking investment decisions to estimate business efficiency and financial status of enterprises. The change of Kazakh enterprises over to international financial reporting standards is substantiated by the need to improve the quality of the provided information for taking management decisions and transparency of financial flows for the existing and potential investor’s, as well as other creditors when taking decisions about providing enterprises with resources.

During their operation, all enterprises inevitably face various kinds of indefiniteness related to certain events or circumstances.

Dynamic development of the external economic environment and complication of terms and conditions of running business in the Republic of Kazakhstan cause the need to provide top quality information about indefiniteness and potential risks. At the same time, changing over to IFRS is a rather difficult process for most of Kazakh enterprises. It requires the involvement of additional labor, financial and time resources. According to the researches, when changing over to IFRS, Kazakh enterprises face the following basic problems: the deficit of personnel that has relevant competences, a rather high cost of consultants’ services and/or training of their employees, the need to modernize/replace software, additional expenses for collecting and processing the initial information, formation of the internal audit system, etc.

Conceptual basics of disclosing information in accordance with international standards (IFRS) suppose compliance with the principle of circumspection expressed in the form of cautiousness when taking judgments in the context of indefiniteness (Miu and Ozdemir 2017).

At the same time, the quality of reporting of numerous Kazakh enterprises does not always comply with the IFRS users’ and developers’ expectations. In this case the information about indefiniteness of the situation and possibility to continue its activity is either not disclosed or disclosed partially. Most of enterprises do not do their best to make their financial reporting as transparent as possible. They do not think it is important to use the IFRS regulation that implies reasonability of providing additional information that is not obligatory for disclosure but is required to understand the described phenomena and events. At the present time voluntary changes in the accounting policy are applied retrospectively unless it is impossible.

One of the urgent tasks of financial management of Kazakh enterprises is to make it consistent with international accounting standards and to reflect factors of indefiniteness and risks that occur as a result of changes in the area of taxation, environment, competitors’ conduct, technological processes, political and economic situation in the country, etc.

The growing recognition of IFRS as a basis for financial reporting is a fundamental change for accounting professionals (Chung and Park 2017). There are more and more countries that require or permit the use of IFRS to make financial reporting of public companies (Gassen 2017).

The process of establishing international standards started several decades ago within the efforts of industrially developed countries on creating standards that could be used by developing and small countries that were not able to define their own accounting standards (Gordon, Henry, Jorgensen and Linthicum, 2017a).

In the context of globalization, the regulating bodies, investors, large companies and auditing companies started realizing the importance of having common standards in all areas of financial reporting (Martínez and Ortiz 2004).

A number of researchers note that financial reporting based on national accounting standards can fail to comply with informational needs of international investors and creditors whose solutions have an international nature (Sinnewe, Harrison and Wijeweera, 2017).

At the same time, a number of researches show that accounting systems must show differences in culture, economic systems, and institutional conditions (Cascino, Clatworthy, García Osma, Gassen, Imam and Jeanjean 2014). Some research works were devoted to the impact of institutional and cultural factors in the context of developing economies.

On April 1, 2001 the Council on International Accounting Standards adopted IFRS. They aim at adopting a unified set of top quality, clear and applicable, generally recognized standards of financial reporting based on accurately formulated principles.

During the research made in the late 2007 by the International Federation of Accountants (IFAC), a great majority of top managers from all over the world agreed that the unified set of international standards was important for the economic growth (Gordon, Henry, Jorgensen and Linthicum, 2017b). 90% of 143 leaders from 91 countries who answered this question said that the unified set of international financial reporting standards was “very important” or “important” for the economic growth in their countries.

At the present time there are rather many researches devoted to aligning national and international standards of accounting and forming financial reporting (Palea, and Scagnelli 2017). The main research problems include issues related to collecting and preparing top quality information to make financial reporting (Effect of information quality due accounting regulatory changes: Applied case to Mexican real sector, 2017), as well as methodological aspects of financial analysis (Sinnewe, Harrison and Wijeweera 2017).

This research will critically consider the problems of applying IFRS in the Republic of Kazakhstan and their impact on the quality of financial reporting of enterprises in the context of indefiniteness. It will be achieved by the secondary analysis of results of periodic research on estimating risks of the Kazakh financial system, results of questioning Kazakh enterprises published on the website of the Depository of Financial Reporting of the Kazakh Ministry of Finance, as well by the analysis of the data collected during the interview of auditors from foreign companies who perform their activity in Kazakhstan.

In Kazakhstan the process of changing over to IFRS started before adopting the relevant legislation and has been taking place for 10 years. Requirements for gradual changing over to IFRS in the Republic of Kazakhstan were defined: financial sector – since January 1, 2003, joint stock companies – since January 1, 2005, and other public organizations – since January 1, 2006.

Now the Republic of Kazakhstan applies three types of IFRS depending on the type and scale of the company’s activity.

Local or foreign companies registered at the Kazakh stock exchange must make financial reporting according to IFRS and US GAAP.

US GAAP are permitted for use according to the requirements of the National Bank of the Republic of Kazakhstan (NT of the RK) for listing companies if, for example, securities were issued according to the US legislation.

In spite of it, all local companies and branches of foreign companies registered in the RK in accordance with the Kazakh legislation must make and publish financial reports according to IFRS in compliance with the Accounting Law (Law of the Republic of Kazakhstan “On Accounting and Financial Reporting” dated February 28, 2007).

Subjects of large business and public companies must provide a full package of IFRS reporting forms, such as

Report about financial state as on the end of the period, Report about profits, losses and other aggregated income,

Report about changes in the own capital,

Report about monetary flows, Report about changes in the own capital for the period,

Notes including a short review about basic provisions of the accounting policy and other explanatory information, and

Comparative information for the previous period.

IFRS for organizations of the public sector (IFRS of PS) that was developed by IFAC for applying in the state sector to provide transparency and succession of financial reporting.

Today IFRS of PS is the most progressive non-binding standard that allows making and providing fuller and more veracious information about facts of economic transactions. In accordance with the Budgetary Code of the Republic of Kazakhstan (Articles 115-118 and 245) and Order of the Minister of Finance of the Republic of Kazakhstan No. 393 dated August 3, 2010, since January 3, 2013 all state establishments have changed over to a new system of accounting.

Since January 1, 2013 small and medium-sized enterprises specializing in the organization of exchange operations with foreign currency have also changed over to International standards (IFRS for small and medium-sized business).

As on 2016 there are 16 IFRS (taking into account IFRS 16 and IFRS 15 that were not put into operation) and 29 IAS (in addition to the standards that are obligatory for applying, there are explanations that describe how to apply standards).

It is necessary to note that IFRS 15 “Revenues from Contracts with Customers” will be introduced since January 1, 2018. It will become the only resource of requirements to recognizing revenues for all types of organizations specializing in any type of activity.

IFRS 15 replaces all existing management requirements in IFRS, such as IAS 11 “Construction Contracts”, IFRS18 “Revenues”, IFRS 13 “Fair Value Measurement”, interpretation of IFRIC 15 “Agreements for the Construction of Real Estate”, interpretation of IFRIC 18 “Transfer of Assets from Customers” and SIC 31 “Revenue – Barter Transactions Involving Advertising Services”. It is applied in relation to the revenues that occur from contracts with customers if they are concluded within other standards, for example IAS 17 (or IFRS 16 “Contracts” after applying them).

IFRS 15 is more regulated than the current requirements of IFRS on recognizing revenues and contains additional requirements to recognizing information. This standard will have an impact on subjects in all areas of the industry. Adopting it will be an important step for Kazakh enterprises that apply IFRS, and probably, will require changing the systems and processes of the current accounting. Thus, successful implementation of this standard will require the estimation and plan of managing changes.

Nowadays international accounting standards as well as international standards of auditing (ISA) are a part of the national system of regulation. They must be published in the Kazakh or Russian language by the organization that has a written permit for the official translation and (or) publication of IFRS/ISA in the Republic of Kazakhstan obtained from the International Accounting Standards Board, and IFAC Council, respectively. The Ministry of Finance of the Republic of Kazakhstan has the relevant agreement with the International Accounting Standards Board, and IFAC about translating from the English into Kazakh or Russian languages. The translation of IFRS into the Kazakh language must be verified and confirmed by an independent expert. After that the translations are sent to the International Accounting Standards Board /IFAC.

Small and medium-sized companies, as well as state enterprises based on the right of operative management make financial reporting in accordance with IFRS for small and medium-sized business, or in accordance with the full package of IFRS. Issues related to the application of IFRS, development of proposals for improving the legislation of the Republic of Kazakhstan on financial reporting and other related matters are discussed at the meetings of the Advisory Board, which is both a consultative and an advisory body.

The accounting policy of enterprises must select the full package of IFRS, IFRS for small and medium-sized business, or the national standard developed by the Ministry of Finance of the Republic of Kazakhstan in 2013. The new national standard of the Republic of Kazakhstan can be applied only by small (micro-) enterprises and financial organizations that carry out only exchange operations.

According to the statistical data of the financial reporting depositaries, today in Kazakhstan the number of companies that have changed over to IFRS is 3,680 public interest entities, including 1,270 enterprises with the right of economic management, 1,100 joint stock companies, 639 companies with the state participation, and 320 financial organizations. For 2003-2016, 15,293 auditor reports were made. In 2008 the fast annual growth of their number was observed.

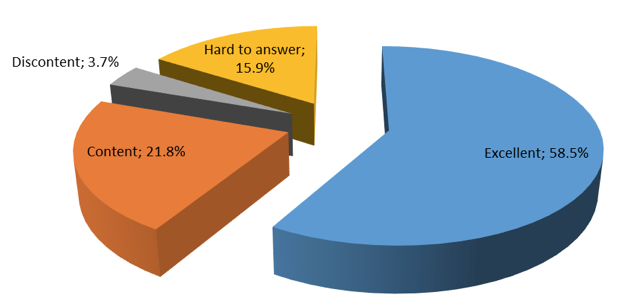

According to the results of the poll published by the Depositary of Financial Reporting of the Ministry of Finance of the Republic of Kazakhstan, the majority of Kazakh enterprises approve and positively estimate the implementation of IFRS in the Republic of Kazakhstan (Figure 1).

Figure 1

How do you estimate the use of IFRS?

There are 3.7% of those who do not support international standards. Others estimate the use of international standards as satisfactory, and some respondents did not answer the question. At the same time 58% of respondents think that the implementation of IFRS has a positive impact on the country’s economy. 23% cannot see the relation between applying IFRS and the economic situation.

61% of respondents agree that the implementation of IFRS (reforming the Kazakh accounting to make it closer to international standards) improves the quality of financial (accounting) reporting.

At the same time respondents note that nowadays the Republic of Kazakhstan has simultaneously accounting, tax accounting and IFRS on the legislative level. In many companies there is management accounting. To a certain degree, it improves the labor intensity of making the company’s reports, and as a consequence, financial burden increases.

Some respondents note that IFRS affects the national economy because it was developed by foreign organizations.

Nevertheless, the majority of Kazakh enterprises (86.7% of respondents) noted that standards of the Kazakh legislation did not have contradictions with international or national financial reporting standards. Besides, many respondents noted that there were no events or operations in the enterprise activity that would make it impossible to apply the requirements of international or national financial reporting standards.

Nevertheless, a greater part of specialists think that IFRS improves veracity and transparency of financial reporting regardless of the geopolitical situation in the country. The majority of respondents think that the state must support accountants and auditors in implementing IFRS (60%). It says about a high level of passivity of the professional community. If to speak about the companies that already use IFRS to make their reports, to reveal risks (create provisions) due to the existing geopolitical situation, the majority of specialists also rely on the assistance of the Ministry of Finance.

Summarizing, it is possible to note that the most positive thing is that the majority of Kazakh enterprises using IFRS treat the estimation of its impact responsibly, and they are based on international standards – a universal financial language that takes into account the best experience of various states based on the interests of financial reporting users.

It is necessary to note that as a whole, the Kazakh financial system is characterized by unsustainable development and a rather high level of various types of risks. Thus, according to members of the financial market and practicing experts in economy and finances, in 2016 the most serious risks include the macro-economic risk because of the growth of the inflation level, and the decrease in export revenues, as well as the credit risk due to the increase in the credit worthiness of economic agents (Results of polling members of the financial market, 2016).

According to experts, in 2016 the Kazakh economy recovery was prevented by non-regulated geopolitical conflicts that had taken place in 2014-2015, maintainable low prices on exchanging markets and external shocks stipulated by the decrease in the tempos of the global economy growth.

The decrease in the volumes of export and direct investments initiated negative factors and stipulated slowing down of the Kazakh economy development, and worsened the state of the real sector down to the level of households.

In order to decrease macro-economic risks, the state maintained the 2016 GDP by implementing programs on financing top priority areas. In spite of the considerable volume of funds obtained within the economy development programs, the most of these funds was focused on maintaining the working capital of various subjects. Financing of the working capital allows maintaining the financial state of the company in the short-term period. At the same time it does not allow solving accumulated system problems, particularly, a high dependence of producers on the import of intra-branch consumption commodities.

In its turn, it slows down the speed of the economy diversification, does not contribute to creating new jobs, and in the near future it can cause the growth of inflation and credit risk.

In 2016 such factors as the growth of inflation, decrease in the purchasing power, worsening of the financial state of small and medium-sized enterprises, as well as the decrease in the collateral value had a considerable impact on the focus of credit risk.

In the context of the credit risks growth, Kazakh financial establishments had to pursue tough credit policy and the possibility of crediting by own bank funds for borrowers was decreased. Lending services were mainly provided for the existing clients who performed their activity in the areas that were subject to crisis least of all and maintained their client base.

Experts forecast that in 2017 the aptitude of the Kazakh financial system to external shocks will continue and the growth of the credit portfolio of the banking system will be refrained by low tempos of the economy recovery.

According to estimates of financial experts, an increase in the level of inefficient loans will cause a growth of expenses for forming provisions. Along with low indicators of profitability, assignation for provisions will worsen the ability of banks to generate capital at the expense of internal sources. The pressure on capital at the expense of provisions will increase the needs of banks in new funds from their shareholders.

It is necessary to note the negative impact of market risks on the profitability of financial enterprises. The re-estimation of the value of the resource base in the foreign currency maintains a high aptitude of banks to losses from the currency rate change. 2016 displays a considerable decrease in the value of market instruments of hedging currency risks. At the same time now regulating requirements on managing the currency risk implemented during the period of fixed currency rate do not allow hedging the existing currency risks.

As a whole, it is necessary to note that the decrease in the sustainability of the country’s financial system is influenced by structural misbalances in economy, and system problems of the banking sector such as a high concentration of credit risk and lack of the long-term funding market.

In the context of unsustainable development of the national financial system, problems of accounting and providing objective and full information about risks and indefiniteness that are peculiar of various companies become especially urgent.

To maintain the integrity of the system of accounting and financial reporting, it is necessary to define development risks, including inadequacy of a real economic situation, incompatibility of information, regulation incoherence, etc. In addition to this, it is necessary to analyze risks related to information used when taking economic relations.

The analysis of the requirements of Kazakh and international financial reporting standards to risks showed that the Kazakh legislation in the area of accounting did not contain issues on risk management as one of its primary tasks. Most often it is explained by the fact that the risk itself is not an object of accounting.

It is important to note that according to the modern theory of risks, a risk is a consequence of indefiniteness. Since accounting recognizes not only past events, but also those that can occur, it is possible to say with certainty that indefiniteness is peculiar of many facts of the economic life. Besides, indefiniteness can be related to the estimation of consequences of the economic life facts. If indefiniteness is considerable, the need to disclose such information in accounting reports is obvious.

Many international financial reporting standards contain requirements of recognizing information about risks in accounting and reporting. They pay much attention to accounting the recognition of risks and indefiniteness. It is related to both methods of accounting and problems of disclosing such information in financial reporting. The focus of requirements of international standards on recognizing information about prospects of developing enterprises is also specified.

Kazakh enterprises that already use or plan to change over to IFRS must pay attention to new standards that must be taken into account when preparing financial reporting for the annual reporting periods than start on January 1, 2017 or later.

Thus, IFRIC 23 somehow explains taxation positions. According to this explanation, in case of indefiniteness in the tax accounting to recognize and estimate income taxes, IAS 12 “Income Taxes” is applied, rather than IAS 37 “Provisions, Contingent Liabilities and Contingent Assets” stipulated by changes of currencies exchange rates. In case of indefiniteness when specifying income taxes, IAS 12 is applied rather than IAS 37 “Provisions, Contingent Liabilities and Contingent Assets”.

Indefiniteness when recognizing the income tax occurs when the company applies an approach to recognizing taxes, and at the same time there is indefiniteness whether the taxation body will accept it as legal. For example, the decision to deduct some expenditures or not to include one income article in the taxation declaration causes indefiniteness when recognizing the income tax unless the taxation legislation permits such decision (Hope, and Vyas 2017).

Explanation of IFRIC 23 is applied to all aspects of recognizing the income tax when there is indefiniteness in relation to the taxable income or loss, taxation bases without assets and liabilities, taxation losses and credits, and taxation rates.

Every case of indefiniteness when recognizing a tax is considered separately or with other cases as a group depending on what approach forecasts the indefiniteness permit best of all. The factors that company can take into account in this case include the way it defines and stipulates its position when recognizing a tax, and the approach that, to its mind, the taxation bodies must apply during the inspection.

When reporting in accordance with IFRS, enterprises must estimate the impact of indefiniteness by using the method that provides the most veracious forecast as to permitting indefiniteness: the method of the most probable value, or the method of expected value.

The use of the most probable value method can be substantiated if possible outcomes have a binary nature or are focused within one figure. The use of the expected value method can be substantiated if there is a range of possible outcomes that do not have a binary nature and are not focused on one figure.

According to experts of the financial market, one of urgent areas is the improvement of IFRS in the context of increasing credit risks and indefiniteness in the activity of financial enterprises (Bulletin of IFRS, 2017). Since 2018 authors of international reporting will start applying IFRS 9 “Financial Instruments”. Banks will see to changing over to this standard most of all. They operate financial instruments more often than companies from other areas.

In their activity Kazakh banks have been taking into account requirements of the Basel Committee on Banking Supervision to statistical models of the risk estimation for 15 years. At the same time the implementation of IFRS 9 requires authors of financial reporting to additionally interpret and synchronize the used estimations of risk.

The main changes made by IFRS 9 in the existing regulations include the change of accounting the incurred losses into the expected ones. Now, in case of the primary recognition, the estimation of expected losses during 12 months is used, and in case of considerable worsening of the credit risk – the estimation of full expected losses, i.e. for the whole period that corresponds to the urgency of the financial instrument.

New regulations of accounting depreciation will become obligatory along with other requirements of IFRS 9 since 2018, but they can be applied prior to maturity. Changing over from IAS 39 to IFRS 9 will touch on not only methodology of accounting and reporting but also business processes and accounting systems.

The standard can also have an impact on the classification and estimation of financial assets. It may result in changing the volatility of income and loss indicators for the period and own capital and as a consequence, key indicators of efficiency. To achieve it, it is necessary to synchronize a new approach with the current approach of banks to stress testing. A new model of expected credit losses will have an impact on the value of the created provisions. Since in this model macroeconomic impacts are important, the level of provisions will considerably depend on the state of economy. The system of estimating losses that will deal with large volumes of data to make forecasts will also change and become more complicated.

In spite of the fact that the majority of the market members find it difficult to accurately define the scale of the change of the provisions value when changing over to IFRS 9, experts agree that the provisions will grow from 30 to 50% (Tata Consultancy Services Limited, 2014).

Crediting small, medium-sized and corporate business is also expected to grow up to 50% (Fifth international research on applying IFRS in banks), and in some segments like mortgaging and retail lending, the growth may achieve 80-250%.

Experts of the financial market think that changing over to IFRS 9 can stabilize the banking system at the expense of serious increase in provisions and as a consequence – improvement of financial sustainability of certain banks. At the same time financial institutions will have to face a number of difficulties. These are the creation of systems for the aggregated calculation based on large databases, change of the organizational structure of banks, as well as negative impact of the growth of provisions for key indicators of efficiency. Since business models of many banks will be low-margin, maybe even loss making, these players will have to leave the market.

The research of applying IFRS in the Republic of Kazakhstan made herein makes it possible to make the following conclusions:

The majority of Kazakh enterprises approve and estimate the implementation of IFRS in the Republic of Kazakhstan positively. Many respondents noted that the implementation of IFRS improved the quality of financial (accounting) reporting.

Nowadays the standards of the Kazakh legislation comply with the standards of international or national standards of financial reporting. However, the Kazakh legislation in the area of accounting does not contain issues on managing risks as one of the primary tasks.

At the same time some respondents note difficulties in implementing IFRS. They considerably increase labor capacity of the company’s reporting, and consequently the financial burden also increases.

The high level of passivity of the professional community of accountants and auditors in mastering IFRS. Due to the current geopolitical situation, the majority of specialists rely on the state support.

Taking into account unsustainability of developing the financial system and rather high level of various types of risks, Kazakh enterprises must pay attention to such new standards as IAS 12 and IFRS 9 that must be taken into account when making financial reports.

Cascino, S. and Clatworthy, M., García Osma, B., Gassen, J., Imam, S. and Jeanjean, T. (2014). Who Uses Financial Reports and for What Purpose? Evidence from Capital Providers. Accounting in Europe, 11(2), 185-209

Chung, H. and Park, S.O. (2017). Voluntary Adoption of the IFRS and Industry-Level Comparability: Evidence from Korean Unlisted Firms. Emerging Markets Finance and Trade, 53(7), 1654-1666

Effect of information quality due accounting regulatory changes: Applied case to Mexican real sector [Efecto en la calidad de la información ante cambios en la normatividad contable: caso aplicado al sector real mexicano]. 2017. Contaduria y Administracion. 62(3), 761-774

Gassen, J. (2017). The effect of IFRS for SMEs on the financial reporting environment of private firms: an exploratory interview study. Accounting and Business Research, 47(5), 540-563

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L. (2017a). Flexibility in cash-flow classification under IFRS: determinants and consequences. Review of Accounting Studies. 22(2), 839-872

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L. (2017b). Review of Accounting Studies. 22(2), 839-872

Hope, O.K. and Vyas, D. (2017). Private company finance and financial reporting. Accounting and Business Research, 47(5), 506-537

Ivanchenkova A. A. and Perevedentseva M. A. (2017). Protsess vnedreniya Mezhdunarodnykh standartov finansovoy otchetnosti (MSFO) v Rossii [Process of implementing international financial reporting standard (IFRS)]. Young Researcher, 18, 146-148.

Martínez C., I. and Martínez, E. O. (2004). International financial analysis and the handicap of accounting diversity. European Business Review, 16(3), 272-291

Miu, P. and Ozdemir, B. (2017). Adapting the Basel II advanced internalratings- based models for international financial reporting standard. Journal of Credit Risk. 13(2), 53-83

Natsionalnyy Bank Respubliki Kazakhstan. Vospriyatiye sistemnykh riskov uchastnikami finansovogo rynka Kazakhstana. Rezultaty oprosa uchastnikov finansovogo rynka [National Bank of the Republic of Kazakhstan. Perceiving system risk by members of the financial market of Kazakhstan. Results of the poll of members of the financial market]. 2016.

Palea, V. and Scagnelli, S.D. (2017). Earnings Reported under IFRS Improve the Prediction of Future Cash Flows? Evidence from European Banks. Australian Accounting Review. 27(2), 129-145

Pyatoye mezhdunarodnoye issledovaniye po voprosam primeneniya MSFO v bankakh. Poisk sobstvennogo puti [Fifth international research on applying IFRS in banks. Search for own way]. [Electronic resource]. http://www2. deloitte.com/ru/ru/pages/ financial-services/archive/ fifth-banking-ifrs-survey. html

Sinnewe, E., Harrison, J.L. and Wijeweera, A. (2017). Future Cash Flow Predictability of Non-IFRS Earnings: Australian Evidence.Australian Accounting Review. 27(2), 118-128

Tata Consultancy Services Limited “An Overview of the Final Version of IFRS 9 Financial Instruments”, 2014. http://www.tcs.com/ SiteCollectionDocuments/ White-Papers/IFRS-Financial-Instruments-1214-1.pdf

Vestnik MSFO. Razyasneniye KRMFO (IFRIC) 23 vnosit nekotoruyu opredelennost v otrazheniye neopredelennykh nalogovykh pozitsiy [Bulletin of IFRS. Explanation of IFRIC 23 makes indefinite taxation positions definite]. July 2017. http://www.pwc.ru/ifrs-news.

Zakon RK “O bukhgalterskom uchete i finansovoy otchetnosti” ot 28 fevralya 2007 g. No. 234-III [Law of the Republic of Kazakhstan “On Accounting and Financial Reporting” No. 234-III dated February 28, 2007].

1. "Almaty Management University", The Republic of Kazakhstan, Almaty, st Rozybakieva, 227; E-mail: adosmanbetova@mail.ru

2. "University of International Business", The Republic of Kazakhstan, Almaty, st Abai, 8а

3. "University Narxoz", The Republic of Kazakhstan, Almaty, st Zhandosova, 55