![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 39 (Number 16) Year 2018 • Page 40

Оlga N. GRABOVA 1; Alexander Evgenievich SUGLOBOV 2; Oleg Gennadievich KARPOVICH 3

Received: 28/02/2018 • Approved: 05/03/2018

2. Theoretical And Methodological Bases Of The Study

ABSTRACT: Innovations are sustainably introduced in tax systems, while the present stage of the states’ development requires a new understanding of the doctrine of development, goals and principles of reforming the tax system as a complex institution interacting with the surrounding institutional environment and economic relations. This work analyzes the state of tax relations and evaluates the current state of the Russian tax system on the basis of objective economic indicators and cross-country comparisons. The necessity of applying the method of the evolutionary and institutional theory synthesis for studying the tax system dynamics is justified. The relationship between the evolution of the tax system, institutions, economic relations and forms of socioeconomic dynamics is formulated and presented as a model, while the primary and indirect fields of influence of the tax system on the forms of socioeconomic dynamics are singled out. Strategic development goals and principles of reforming the tax system are proposed. Risks and reserves of improving the tax system efficiency in the information society are identified. |

RESUMEN: Las innovaciones se introducen de forma sostenible en los sistemas tributarios, mientras que la etapa actual del desarrollo de los estados requiere una nueva comprensión de la doctrina del desarrollo, los objetivos y principios de reformar el sistema tributario como una institución compleja que interactúa con el entorno institucional y las relaciones económicas circundantes. Este trabajo analiza el estado de las relaciones tributarias y evalúa el estado actual del sistema tributario ruso sobre la base de indicadores económicos objetivos y comparaciones entre países. La necesidad de aplicar el método de síntesis de la teoría evolutiva e institucional para estudiar la dinámica del sistema tributario está justificada. La relación entre la evolución del sistema tributario, las instituciones, las relaciones económicas y las formas de dinámica socioeconómica se formula y presenta como un modelo, mientras que se destacan los campos de influencia primarios e indirectos del sistema tributario sobre las formas de la dinámica socioeconómica. Se proponen objetivos de desarrollo estratégico y principios para reformar el sistema tributario. Se identifican los riesgos y las reservas para mejorar la eficiencia del sistema tributario en la sociedad de la información. |

The tax system requires constant attention and monitoring both from the state and from the standpoint of scientific interpretation for a few reasons. First, the interests of the state are realized through the tax system; taxes are a financial expression of the state existence. Being part of the mechanism producing the socially significant public goods – education, healthcare, pensions, – taxes undoubtedly reflect the interests of the entire society and all citizens. However, this is a system described by a clash of interests of the state and business. Business is seeking to minimize its tax costs through legal and sometimes semi-legal and illegal ways. However, entrepreneurs do not always realize the major social responsibility of business – paying taxes. This occurs due to imperfection of the tax legislation and possible immaturity (both social and financial economic) of Russian business, and due to the special way and conditions for the development of large business in Russia. This is why configuration and improvement of the institutions and mechanisms of the tax system become one of the important aspects of overcoming the disunity of interests, the growing gap between the poor and the rich in Russian society. Secondly, the importance of external factors in the tax system development is increasing under current conditions – including "tax havens" of individual states and other more favorable economic conditions that facilitate capital migration from Russia, and even economic sanctions do not hinder this process. It must be recognized that the world economic and social integration processes that cause the high mobility of capital and labor force compel states to pursue a tax policy that can be called "competitive" in relation to the entire civilized world. Therefore, the course of the Russian tax system development should be built taking into account a variety of internal and external factors.

Comprehension of the tax burden, its gravity, dynamics and development trends should rely on the existing provisions of economic theory.

During the development of fiscal tax theory and practice, two approaches to substantiating institutional changes in the tax system and regulating the economy through fiscal methods have been developed. One of them is based on the theory of the English scientist John Maynard Keynes (2007). The idea of this approach is that "effective demand" is the main factor of economic growth. Taxes also play an active role in stimulating demand, and certain fiscal measures are implemented depending on the phase of the business cycle. In the phase of crisis, it is necessary to increase costs and reduce taxes; when the economy enters the recovery phase, it is proposed to reduce costs and increase bite of taxes.

Another approach to fiscal theory and regulation arose in opposition to Keynes's theory and was called the "supply-side economy". This theory shifts the focus of fiscal policy from budget spending to taxes. It is assumed that personal income tax and corporate taxes should be reduced to stimulate production. Proponents of the "supply-side economy" turn to the Laffer curve to illustrate the validity of their arguments, which shows that the bite of taxes has the optimal value – the limit, exceeding which leads to a decrease in revenues to the budget. According to this theory, the optimal amount of the bite of taxes should not exceed 35% of the added value, and the task of revitalizing business (primarily investment) activity should be solved by alleviating the tax burden (although Laffer does not deny that he borrowed the ideas from the J.M. Keynes’s concept).

At the same time, the tax system development is defined by global and internal trends based on the actions of various interests. The mechanism for the realization of interests is always related to institutions and economic relations in society. Therefore, it is very useful to resort to evolutionary institutional theory (Grabova 2007; Nelson and Winter 2002; Hodgson 2003).

Special attention is currently paid to tax research methods (Kireenko 2015) and certain aspects of taxation: regional tax potential (Tsepelev and Kakaulina 2015); impact of certain taxes on the firm's business (Conrad 1999), territories and state (Burgess and Stern 1993), international capital flow (Giovannini 1990) and taxpayer behavior (Sutter and Weck-Hannemann 2003); applied research of various tax function realizations (Carroll and Yinger 1994; Hettich and Winer 2006), optimal taxation (Slemrod 1990). In the opinion of the authors, theoretical and methodological approaches to the taxation theory, on the basis of which prognostic models could be built, are poorly understood (Bank and Suglobov 2014; Frecknall-Hughes and Kirchler 2015; Granqvist and Lind 2005; Veselovsky, Suglobov, Abrashkin, Khoroshavina and Stepanov 2016; Veselovsky, Suglobov, Khoroshavina, Abrashkin and Stepanov 2015).

A tax system is an institution operating in certain economic relations, corresponding or not corresponding to these economic relations. Perfect correspondence between institutions and economic relations is impossible; there is always some asymmetry in the development of these systems. It can be said that the asymmetry is "natural" in the evolutionary interdependent development of these systems, and these systems are "tuned" with small iterations. Such a gradual reform with small iterations ensures the stability of both the tax system and the system of economic relations. In this case, stability is a condition for active business development, which does not have to divert its financial, labor and other resources from solving the core tasks – implementation of the business mission. "Revolutionary", profound transformation processes in the tax system are usually associated with similar processes in economic relations.

If the latest Russian history is analyzed, such transformational processes occurred during a period of dramatic changes in economic relations – the well-known transition from a command-administrative economy to a market economy, during the reforms of the 90s. It was a period when everyone learned to "swim" in a market economy. Many failed to "swim out" and went bankrupt. There were many reasons for this, but one of them was the "draconian" taxation system, which combined high taxes and severe sanctions for non-payment of these taxes, and even situations when regulations in fact had a "retroactive effect," when official publication (apparently, due to bureaucratic delays) occurred after the regulation effective date.

Over its short development path, the Russian tax system has evolved into a fairly harmonious system. The basic tax rates for VAT, personal income tax and corporate profits tax are comparable with or even lower than the level of similar taxes in leading countries. The tax burden on the Russian economy was almost always lower than the average for the member countries of the Organization for Economic Cooperation and Development (OECD) for the period from 2009 to 2014 as well (Table 1).

Table 1

Tax burden on the economy in some member states of the Organization for E

conomic Cooperation and Development (OECD) in 2009-2014, % of GDP

OECD states |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

UK |

32.32 |

32.80 |

33.58 |

33.05 |

32.93 |

32.57 |

Germany |

36.09 |

34.98 |

35.70 |

36.38 |

36.53 |

36.13 |

Italy |

42.06 |

41.84 |

41.88 |

43.88 |

43.88 |

43.64 |

Canada |

31.36 |

30.44 |

30.24 |

30.72 |

30.54 |

30.82 |

US |

22.97 |

23.18 |

23.56 |

24.05 |

25.41 |

26.00 |

Finland |

40.93 |

40.79 |

42.03 |

42.68 |

43.74 |

43.85 |

France |

41.32 |

41.58 |

42.86 |

44.13 |

45.03 |

45.22 |

Switzerland |

27.13 |

26.50 |

27.02 |

26.90 |

26.86 |

26.65 |

Sweden |

44.08 |

43.22 |

42.51 |

42.56 |

42.85 |

42.70 |

Japan |

26.96 |

27.57 |

28.61 |

29.41 |

30.31 |

n/a |

Average for OECD |

32.68 |

32.78 |

33.29 |

33.79 |

34.15 |

34.44 |

Russia |

30.88 |

31.12 |

34.50 |

32.49 |

31.80 |

31.89 |

Russia (excluding oil and gas revenues) |

22.69 |

22.48 |

23.75 |

22.12 |

21.86 |

21.72 |

Source: Major areas of the tax policy for 2017 and the target period of 2018 and 2019

The data from Table 1 indicate a certain proportionality of the Russian tax system and its similarity with European models. Integrating into Europe, Russia was originally focused on some copying of the European tax systems; moreover, it was also predetermined by the lack of historical experience in building a tax system in market conditions. These data also reveal the uniqueness of the US economy and its advance in opportunities for real sector development due to a reduced tax burden. (Uniqueness of the US lies in the fact that it did not introduce the European VAT and applied sales tax instead, which did not lead to high inflation and price growth). Of course, the proportions of tax rates and tax burden do not indicate the absolute values of GDP indices in general and per capita, for which Russia is much inferior to the leading countries.

The tax burden varies considerably by industry and type of activity in the Russian Federation, and in accordance with the methodology of the Russian Union of Industrialists and Entrepreneurs (RUIE), it varied as follows over the period from 2008 to 2014: agriculture, hunting and forestry – from 3.2 to 5.2%, fishing and fish farming – 11.1-16.4%, mining operations – 58.1-76.8%, processing production – 24.1-32.2%, production and distribution of energy, gas and water – 22.9-31.4%, construction – 18.1-21.7%, wholesale and retail trade – 10.9-16.6%, hotel and restaurant business – 15-19.2%, transport and communications – 22-26.4%, financial activities – 17.3-25.4%, real estate operations – 17.5-23.9%, state administration, military security and social security insurance – 7.6-9.3%, education – 19.1-28.7%, healthcare and social services – 13.1-20.5%, other utilities, social and personal services – 18.5-24.6% (Major areas of the tax policy for 2017 and the target period of 2018 and 2019).

At the same time, the RUIE method differs from similar methods used by international organizations and does not allow for cross-country comparisons. This method involves comparing the amount of tax payments to the consolidated budget of the Russian Federation (net of personal income tax) and insurance premiums with an integrated indicator – gross added value (net of depreciation). Personal income tax is often deducted in various methods of analyzing the tax burden, because organizations act as a tax agent for the payment of personal income tax under the law, and individuals are taxpayers. At the same time, there is no doubt that personal income tax impacts the activities of any business, and payment of personal income tax also means withdrawal of financial resources from business. Therefore, personal income tax will add significantly to the tax burden in labor-intensive industries.

Tracking the movement of value in international economic transactions is also required in terms of strengthening the state and ensuring economic security. The indicators of business development here are still worrying for Russia (Table 2).

Table 2

Net import (-), export (+) of capital by the private sector in 1997-2016 in the Russian

Federation (according to the balance of payments of the Russian Federation,

according to the APB methodology), bln US dollars

Years |

Total |

Banks |

Other sectors |

1997 |

18.4 |

-7.6 |

26.0 |

1998 |

22.6 |

6.4 |

16.2 |

1999 |

19.5 |

4.4 |

15.1 |

2000 |

23.1 |

1.7 |

21.4 |

2001 |

13.6 |

4.0 |

9.6 |

2002 |

7.0 |

3.0 |

4.0 |

2003 |

0.3 |

-12.8 |

13.1 |

2004 |

8.6 |

0.7 |

7.9 |

2005 |

0.3 |

3.7 |

-3.4 |

2006 |

-43.7 |

-27.9 |

-15.8 |

2007 |

-87.8 |

-50.5 |

-37.3 |

2008 |

133.6 |

84.5 |

49.1 |

2009 |

57.5 |

32.4 |

25.1 |

2010 |

30.8 |

-22.8 |

53.6 |

2011 |

81.3 |

27.5 |

53.8 |

2012 |

53.9 |

-7.9 |

61.8 |

2013 |

60.3 |

17.3 |

43.0 |

2014 |

152.1 |

86.0 |

66.1 |

2015 |

57.5 |

34.2 |

23.3 |

2016 |

15.4 |

5.3 |

10.1 |

Total for the period |

624.3 |

181.6 |

442.7 |

Source: Net import / export of capital by the private sector in 1994-2016 and January-September 2017

It can be seen that business unambiguously responded to the economic crisis of 2008-2010 and the active deployment of sanctions against Russia in 2014 by the migration of capital from the Russian Federation. As the authors understand, only large and financial capital is basically capable of migration, while the flow of both bank capital and capital of the real sector is poorly controlled by the state. Therefore, it is necessary to build a system of institutions to combat capital outflow along with building an efficient tax system, because this is capital which should basically work for the benefit of the country it has been created in, using the natural and human resources of the Russian Federation.

In accordance with O. Williamson's theory of "institutional economics" (Williamson 2000), the tax system must belong to the second level of the institutional environment that defines the formal rules of the game, especially property rights. The frequency of changes in these norms is 10 to 100 years. But at the same time, both by virtue of the frequency of changes in the norms and by virtue of its nature, the tax system predetermines the so-called strategy of "playing the game" and patterns of behavior of economic actors – participants in transactions, and therefore belongs to the third level of institutions, according to the Williamson's theory.

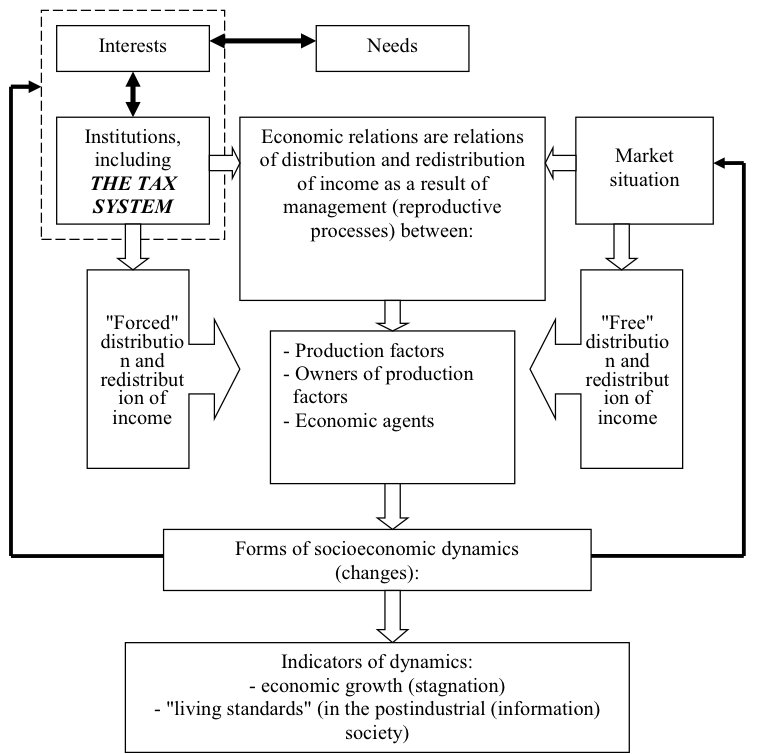

However, norms and institutions cannot be considered apart from economic relations – therefore, an analysis based on the synthesis of institutional and evolutionary theory becomes useful (Grabova 2007). This analysis implies that the tax system is built into a complex system of interaction between institutions, economic relations and market situation. This interaction results in the constant improvement of the tax system and its innovative renewal preserving the key elements – "genes" that ensure its own stability and stability of the economic system. "Tax norms" here appear as genes that are constantly screened through interaction with economic relations and forms of socioeconomic dynamics and predetermine the survival of the entire macrosystem – the state – at a specific historical period in the development of economic relations (see Figure 1).

The needs and interests are highlighted in this scheme as drivers of the society development. It is quite logical to ask the following question with regard to the tax system: in whose interests is the tax system built? Of course, it is a result of some compromise between business, society and the state. But one can often hear arguments around the fact that business pays taxes, while public goods are used mainly by the poor. Of course, from the regulative point of view, taxes are officially paid by business, but taxes themselves are part of the taxable value that is created not only by business but by the merging factors of production, labor being the most important of them.

The authors did not use the traditional systematization of economic relations as relations regarding the production, distribution, exchange and consumption in this case, but these phases are meant, since the authors point to reproductive processes. Besides, the tax system plays an important role precisely in terms of the distribution of benefits in society and allocation of resources that drive the forms of socioeconomic dynamics. Allocation and distribution processes are important, since they further predetermine the investment potential of businesses, organizations and the possibility of consumption by individuals, which contributes to economic growth and living standards in the country.

Primary and indirect fields of influence of the tax system on the forms of socioeconomic dynamics should be singled out. For example, the tax system has the greatest, predominant influence on such dynamics as structural changes (including sectoral and interbudgetary); forms of ownership (legal), types of economic entities by the scale of their activities (national and transnational, large, medium, small business and self-employment); technical, technological and organizational changes; dynamics of price proportions. The tax system can have indirect, not primary or weak influence on the social, demographic, political and value dynamics.

It must be noted that stable inefficient institutions, norms of economic behavior and inefficient economic relations emerge in the process of institutional development and reforms aimed at increasing the efficiency of the economic system, including in Russia. In contrast to efficient norms, this phenomenon has different names in the literature: the blocking effect, “locking”, lock-in (D. North 1997), "institutional traps" (Polterovich V.M. 2004), anomalies (Scarzhinskiy M.I. 2005), dysfunction of the institution, economic dysfunction (Sukharev O. 2002).

Figure 1

Relationship of the evolution of the tax system, institutions, economic relations

and forms of socioeconomic dynamics (developed by the authors)

Evolutionary institutional theory provides toolkit for analyzing the dysfunctions and defects in the economy development in this case as well. The tax system and economic relations that develop under its influence are not an exception, and therefore it is necessary to carry out constant analysis of the influence of the tax system on the development of the economy in general and its separate sectors in particular. At the same time, dysfunctions usually arise due to a set of institutional factors, the tax system being one of them. Such a set of factors adversely affects the development of the industry or a separate sector (factor) of economic development.

For example, we observe the fading dynamics of the alcoholic beverage industry development with the wavy recurring bankruptcies of enterprises, lack of modernization and high depreciation of the fixed assets in this industry in the post-reform period (reforms of the 90s). This is explained not just by the tax system (although excises and other taxes "eat up" almost all of the proceeds), but also by inefficient institutions of state regulation and management in this industry. As a consequence, these enterprises cease to play the role of the main budget-forming taxpayers for many provincial cities poorly developed in industrial terms. There are also negative consequences in Russia in the form of mass poisonings with alcohol-containing liquids. On the one hand, lack of systemic institutional regulation of innovation activities generates many inefficient projects that have turned into "shoveling" state money, but on the other hand, they do not contribute to the innovation-driven growth of the commercial sector in accordance with modern requirements.

As it has been shown, the tax system includes a complex system of socioeconomic dynamics and depends on the level of economic relations development. As a state institution, the tax system must be efficient, and strategic priorities for its development must be consistent with the priorities of the state and society. At the present stage, the concretization of strategic goals or even the doctrine of the tax system development is required. The authors believe that two key factors of the tax system development that have equal significance must be taken into account.

The first is that the national tax system has an external economic environment, which is determined both by interstate economic relations and even more by the level of the tax system development in other countries, the attractiveness of these systems for business in terms of tax burden and interaction with tax administration bodies. At the current stage of a virtually barrier-free flow of capital, the national tax system must be competitive at the cross-country level. Of course, "preservation of national capital" in the form of financial and human resources should be ensured not only by the tax system, but by all interconnected and co-dependent institutions.

Internal economic relations are the second factor defining the long-term prospects for the development of the Russian tax system. While the first factor (which can be conditionally called "external") dictates a strategic goal that can be interpreted solely on the basis of economic criteria, the second factor of development predetermines the formulation of strategy priorities from a socioeconomic standpoint. The authors believe that the tax system appears to be a unique institution at this point. Its uniqueness lies in the fact that this institution can and should ensure not only its "direct" functions (fiscal, regulatory, etc.), but also functions and goals aimed at realizing the public interests: consolidation of society, public confidence in the state, and realization of the justice ideas. These ideas and goals for the tax system are no less important than economic ones, since they promote the development of a harmonious, solidary and patriotic society. The idea and strategic goal of justice must be especially important for Russian society, since it is an heir of the Soviet society, where these ideas were undoubtedly realized, but under completely different conditions, other institutions and economic relations: the system of incomes for all citizens depended on the socially necessary labor; socially significant public goods – education, healthcare – were accessible to every citizen. It can be said that the idea of justice was implemented systematically, and this system collapsed in the 90s. This is why horizontal and vertical justice in the Russian perception is supplemented by the realization that there are few elements of justice that determine the accumulation of social capital in society in the market conditions; it is a truncated, sequestrated system at the time. Today, it is a system basically consisting of two main subsystems: a subsystem of the socially significant public goods provided by the state (which is reproduced through the tax system mechanism), and the tax system that must bear elements of justice within itself. This means the withdrawal of natural rents and super-profits in favor of the entire society through the taxation system. This is partially realized, but not everything.

The principles of building a tax system are usually discussed. Despite the diversity of national taxation systems, these principles are universal for economically developed countries at the present stage. The methodological foundation of these rules is related to the birth of an economic theory as a science and to the name of Adam Smith (Smith, n. d.), the founder of political economy. He outlined four basic principles in his paper, which are still not obsolete: 1) principle of justice, interpreted as the universality of taxation and the uniformity of the tax distribution among citizens in accordance with their incomes; 2) principle of certainty, which can be interpreted as the prominence of all the tax elements for a taxpayer; 3) principle of convenience, which requires that the tax be levied at a convenient time and in a convenient way for a taxpayer; 4) principle of economy, which involves minimizing the costs of levying taxes and maximizing the revenues of the state budget.

In the opinion of the authors, current principles of taxation are most fully presented by the authoring team led by I.A. Maiburov (2010) and the authoring team led by A.E. Suglobov (2015).

Let’s cite them in order to supplement them in accordance with the challenges of reforming the tax systems in general and in Russia in particular at the present stage. The set of principles is systematized in three groups. It probably does not make sense to disclose their essence in full, but the authors will provide some comments in regard to the problems and logic of the study. The first group includes "economic" principles: justice (horizontal and vertical), efficiency (or economy), proportionality (tax burden accounting), plurality of tax bases, universality for those who fall under the notion of a taxpayer, and principle of interest accounting (formulated by I.A. Maiburov, a very important principle for the evolutionary institutional theory of taxation, but the essence and content of this principle requires correction). The second group is principles that have "legal" base: principle of taxes established by laws, priority of tax legislation (a fairly rigid principle from the standpoint of reforming and systemic support of the state institutional environment), principle of the availability of all elements of tax in law, principle of denial of retroactivity of the tax law, principle of neutrality as the absent elements of discrimination on any grounds in the tax system, including the equality of the state and the taxpayers. The third group is organizational principles: unity of the tax system throughout the state, certainty (for example, laws should not be interpreted arbitrarily by executive bodies), principle of mobility or elasticity of taxation (principle of the operational possibility of the fiscal function strengthening or weakening), principles of stability, tax federalism, publicity and momentariness of taxation.

The historical evolution of taxes teaches that the tax system as an institution depended on the level of the society development: formation, production and economic relations, productive forces and degree of the state development in general. As the economic science emerged, taxes were increasingly systematically interpreted. At a certain stage, economic science itself began to play an increasingly important role in the practice of taxation. The most striking current example of this is VAT as a tax and added value as an object of taxation. Can the history be appealed, if the current theory and practice of taxation are understood? It is extremely difficult from the standpoint of objects of taxation, as they have strongly evolved. However, the appeal to history is justified from the standpoint of regularities in processes occurring when alienating part of the income received from the main sources – rent, profit and wages – in favor of the state.

Moreover, taxation depends on the level of scientific and technological progress, on the conditions of a postindustrial society, increasingly realized as information, at the present stage as never before. Creation and movement of value is increasingly carried out through information technology. In the opinion of the authors, these flows both within the individual state and between the states are poorly regulated from the standpoint of taxation. New technology has generated new opportunities for tax evasion, since the mechanism for monitoring the movement of value and objects of taxation by the state has not been built. Indeed, there are huge reserves for increasing tax revenues here. This requires to improve institutions of value taxation in the IT space. Cost is created due to various types of content (software products, databases, websites, etc.) in the modern world; information currently creates value, and this is not similar to intangible assets understood at the level of development of the current legislation in the Russian Federation.

Another field of development of the tax system in the IT space is improvement through the control over the movement of familiar goods through online stores and other information marketplaces, as well as with other sources of taxation. It must be acknowledged that the insufficient regulation and imperfection of the control mechanisms for movement of such a value for Russia is even dangerous, and the danger is not so much internal as external, defined by international economic relations, since countries possessing information technology and industrial products (including consumer products) are able to "pump out" finance from Russia with a double benefit: in terms of capital inflows and gains from tax evasion in Russia.

At the same time, Russia has prepared and implemented innovation in the transfer and storage of data associated with any product sale, i.e. trade turnover made outside of information technology will have to be duplicated through information systems and databases. The authors believe that such duplication of information is inexpedient. Besides, it is hard to say whether modern IT technology will be able to secure such an information flow in a qualitative way. At the same time, it will be necessary to solve many tasks related to transfer, storage and, most importantly, processing and analysis of this information, which will already be associated not only with the limit of information resources, but also with the limit of human resources in the tax authorities and in related industries (for example, to ensure electronic document flow).

The authors also suggest to add principles of reform to the principles of building a tax system. From the standpoint of the evolutionary institutional methodology, the authors believe that the tax system should be reformed taking into account the "part dependence" principle, depending on the previous development trajectory. This is a principle of continuity in the tax system development, because the breakdown of institutions leads to destabilization of business in the first place, and hence all the resulting negative consequences: tax evasion, "shadowing", migration of capital, etc. Secondly, this principle of continuity presupposes building of its own national taxation system that is understandable and accepted by society. In this case, the practice of the leading countries should really be perceived as experience, not a model for blind copying. Even if certain norms work efficiently in an economically highly developed country, this does not mean that the same norms will strike roots and have an effect in Russia. For example, the construction of a progressive scale can be seen in the system of income taxation for German citizens, on the basis of whether a citizen is married (officially or civilly) or not. This might be a fair system for Germany, but for Russia it is completely unacceptable. Thirdly, this principle should not reject the laws of dialectics and evolutionary institutional theory, according to which there are circumstances that require significant reforms at a certain stage. These reforms in the tax system should be carried out with the least losses for society, state and business. This will be facilitated by an active discussion of future reforms and projects in the scientific and business community with free access to these materials for all stakeholders.

The next principle is the principle of "benevolence", or the principle of openness and hand-on assistance to business and every taxpayer. This principle should be manifested in preventing violations and reducing penalties and other sanctions for an unintentional violation of tax laws. Violations can be prevented through interviews with taxpayers, through the arrangement of advisory services directly in tax authorities. These advisory services may be chargeable, but the level of their cost should be lower than that of private tax advisers. It is also a great reserve for improving the quality of tax relations and increasing the income of tax inspections and tax inspectors through additional services. In the opinion of the authors, the area of tax advice should primarily belong to professionals with the official status of tax inspectors. Besides, it will raise the level of wages of tax inspectors, which is currently very low and does not match the qualifications of these specialists, will increase the prestige of this profession and reduce staff turnover.

Another principle follows from this – the "adequacy" of punishments to the committed violations in the tax field. This principle assumes the reduction of "punitive" measures and norms of legislation. The authors do not advocate the absence of punishments or connivance in case of committing serious economic crimes. The point at issue is that the economic equivalent of the damage caused to the state must be calculated in each individual case, its compensation to the state should be obligatory, but it is all should be done mainly within the Administrative Code.

It is necessary to introduce the principle of the tax system comparability with the tax systems in the leading countries in terms of tax structure and tax burden to make it competitive at the global level. At the same time, the tax system in Russia loses its uniqueness in the main elements and may be deprived of certain priorities.

It is required to take the principle of the modern IT technology adequacy in reforms into account due to the development of the current information society. The field of innovation in the tax system in this regard was described above.

Due to the fact that the institutional system in a certain field always has many areas overlapping with systems in other fields, it is necessary to take into consideration the principle of "complementarity" (consistency and additionality) with related systems of institutions, such as the regulatory accounting regime, system of regulating the economic administrative violations and criminal offenses, labor legislation, etc. when reforming the tax system.

Of course, the principle of adequacy to modern economic relations must be taken into consideration due to the complex dynamics of modern economic relations, when the movement of value and property becomes more complicated under the influence of internal and external (international) factors, and due to increased capital mobility in reforming. In this case, economic relations should be analyzed in terms of realizing the interests of various levels: for an individual (for the analysis of personal income tax, self-employment as a form of business or as a form of survival – the latter should not(!) be taxed at all), firm, region, transnational companies (TNCs), consolidated taxpayer groups (CTG), state and society.

Overall, the current stage of the tax system development in Russia is described by being close or even reproducing European taxation systems in the structure of taxes and the tax burden (except for the progressive scale of income taxation used in Europe and the US). Such "non-uniqueness" contributes to the integration of our country into the international economy, on the one hand, while, on the other hand, it does not allow for maneuvers of the advancing development in this institutional system. Besides, the dynamics and ongoing reforms in the tax system should be evaluated from various parameters: from the standpoint of realizing the interests of society, influencing the institutional environment and economic relations, socioeconomic dynamics, proportional development of industries, regions and areas of modern value drivers, which should ensure Russia's strategic advantages on the world stage.

Bank S.V. and Suglobov A.E. (2014). Tactical and strategic modelling of the corporate financial performance indexes. World Applied Sciences Journal, 29(5), 683-688.

Burgess R. and Stern N. (1993). Taxation and development. Journal of Economic Literature, 31(2), 762-830.

Carroll R.J. and Yinger J. (1994). Is the property tax a benefit tax? The case of rental housing. National Tax Journal, 47(2), 295-316.

Conrad K. (1999). Resource and waste taxation in the theory of the firm with recycling activities. Environmental and Resource Economics, 14(2), 217-242.

Frecknall-Hughes J. and Kirchler E. (2015). Towards a general theory of tax.

Social and Legal Studies, 24(2), 289-312.

Giovannini A. (1990). International capital mobility and capital-income taxation: theory and policy. European Economic Review, 34, 480-488.

Grabova O.N. (2007). Evolyutsionno-institutsionalnaya teoriya dinamiki ekonomicheskikh otnosheniy [Evolutionary institutional theory of the dynamics of economic relations]. Kostroma: KSU named after N.A. Nekrasov, pp. 327.

Granqvist R. and Lind H. (2005). Excess burden of an income tax: what do mainstream economists really measure? Review of Radical Political Economics, 37(4), 453-470.

Hettich W. and Winer S.L. (2006). Analyzing the interdependence of regulation and taxation. Public Finance Review, 34(4), 355-380.

Hodgson D. (2003). Ekonomicheskaya teoriya i instituty: Manifest sovremennoy institutsionalnoy ekonomicheskoy teorii [Economics and Institutions: A Manifesto for a Modern Institutional Economics]. Moscow: Delo, pp. 464.

Keynes J.M. (2007). Obshchaya teoriya zanyatosti, protsenta i deneg [The General Theory of Employment, Interest and Money]. Moscow: Eksmo, pp. 960.

Kireenko A.P. (2015). Methods of investigating taxation in today’s foreign literature. Journal of tax reform, 1(2-3), 209-234.

Maiburov I.A. (2010). Nalogi nalogooblozheniye [Taxes, taxation]. Moscow: UNITY-DANA, pp. 559.

Nelson R. and Winter S. (2002). Evolyutsionnaya teoriya ekonomicheskikh izmeneniy [An Evolutionary Theory of Economic Change]. Moscow: Delo, pp. 536

Net import / export of capital by the private sector in 1994-2016 and January-September 2017. https://www.cbr.ru/statistics/credit_statistics/bop/outflow.xlsx (Access date: 18.02.2017.)

North D. (1997). Instituty, institutsionalnyye izmeneniya i funktsionirovaniye ekonomiki [Institutions, Institutional Change and Economic Performance]. Moscow: Fund of the economic book "Nachala", pp. 180.

Osnovnyye napravleniya nalogovoy politiki na 2017 god i planovyy period 2018 i 2019 godov [Major areas of the tax policy for 2017 and the target period of 2018 and 2019]. Information from the official website of the Ministry of Finance of the Russian Federation. http://minfin.ru/ru/document/?id_4=116206 (Access date 18.02.2017).

Polterovich V.M. (2004). Institutsionalnyye lovushki: yest li vykhod? [Institutional traps: is there a way out?]. Social sciences and modernity, 3, 5-16.

Scarzhinskiy M.I. (2005). Sistemnyye defekty ekonomicheskikh otnosheniy. Postanovka problemy [Systemic defects of economic relations. Statement of the problem]. Problems of the new political economy, 3.

Slemrod J. (1990). Optimal taxation and optimal tax systems. Journal of Economic Perspectives, 4(1), 157-178.

Smith A. (n. d.). Issledovaniye o prirode i prichinakh bogatstva narodov [An Inquiry into the Nature and Causes of the Wealth of Nations]. Moscow: Eksmo, pp. 960.

Suglobov A. E. (2015). Nalogi nalogooblozheniye [Taxes, taxation]. Moscow: UNITY-DANA, pp. 544.

Sukharev O. (2002). Kontseptsiya ekonomicheskoy disfunktsii i evolyutsiya firmy [Concept of economic dysfunction and evolution of the firm]. Issues of economics, 10, 70-81.

Sutter M. and Weck-Hannemann H. (2003). Taxation and the veil of ignorance - a real effort experiment on the laffer curve. Public Choice, 115(1-2), 217-240.

Tsepelev O. and Kakaulina M. (2015). Modeling the impact of taxes on economic growth with regional resource potential. American journal of applied sciences, 12(5), 345-354.

Veselovsky M.Y., Suglobov A.E., Khoroshavina N.S., Abrashkin M.S. and Stepanov A.A. (2015). Business angel investment in russia: problems and prospects. International Journal of Economics and Financial Issues, 5(S), 231-237.

Veselovsky M.Ya., Suglobov A.E., Abrashkin M.C., Khoroshavina N.S. and Stepanov A.A. (2016). Managing Russian science-intensive enterprises in the emerging new technological paradigm. International Review of Management and Marketing, 6(S5), 16-22.

Williamson O. E. (2000). “The New Institutional Economics: Taking Stock, Looking Ahead”. Journal of Economics Literature, XXXVIII, 595-613.

1. Federal State Budgetary Educational Institution of Higher Education "Kostroma State University" (KSU), Russian Federation

2. Federal State Budgetary Educational Institution of Higher Education "Financial University under the Government of the Russian Federation", Russia. E-mail: a_suglobov@mail.ru

3. State Budget Institution of Higher Education “Russian Customs Academy”, Russia