![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 39 (Number 45) Year 2018. Page 23

Aleksandr Nikolaevich GOSTEV 1; Tamara Ivanovna TURKO 2; Valerii Filippovich FEDORKOV 3; Sergei Borisovich SHCHEPANSKII 4

Received: 06/06/2018 • Approved: 06/07/2018

ABSTRACT: Based on the results of a specific sociological study, the present article justifies the need for reliable and accurate state accounting and control of the activities of small innovative enterprises at institutions of higher education and scientific organizations as a special activity management system; provides the content and peculiarities of the process methodology; displays the laws, patterns, principles and methods of accounting; develops a technology and indicators of accounting; defines risks, threats, and dangers of unreliable accounting and their relationship to political, economic and other processes; justifies the key findings of the analysis and comparison of innovation activity statistics in Russia and in foreign countries; identifies the strengths and weaknesses of the national state accounting system; analyzes the content of the Russian legal and regulatory framework for public accounting; draws conclusions and recommendations on the implementation of the state accounting procedure. |

RESUMEN: Basado en los resultados de un estudio sociológico específico, el presente artículo justifica la necesidad de una contabilidad estatal confiable y precisa y el control de las actividades de pequeñas empresas innovadoras en instituciones de educación superior y organizaciones científicas como un sistema especial de gestión de actividades; Aporta el contenido y las particularidades de la metodología del proceso. Muestra las leyes, patrones, principios y métodos de contabilidad; Desarrolla una tecnología e indicadores de contabilidad; define los riesgos, amenazas y peligros de la contabilidad no confiable y su relación con los procesos políticos, económicos y otros; justifica los hallazgos clave del análisis y comparación de las estadísticas de actividad de innovación en Rusia y en países extranjeros; identifica las fortalezas y debilidades del sistema contable estatal nacional; analiza el contenido del marco legal y regulatorio ruso para la contabilidad pública; extrae conclusiones y recomendaciones sobre la implementación del procedimiento contable estatal. |

The world economy is moving rapidly to science-based technologies. Science and education in their unity not only remain the basic institution of society, but also become the immediate means of production. Therefore, in this area, state accounting should be accurate, reliable, reasonable and, therefore, performed on a specialized methodological basis.

As is well known, the management of any social phenomenon is a process that is studied to some extent by all sciences. It involves all formal (administrative) and informal (public) organizations, assets and means. Accounting, control is part and a special system of management (Gostev, 2016, p. 109). In this regard, to organize effective management, a comprehensive and qualitative research of the object-subject sphere of the phenomenon studied in this work is required.

The study of the essence, content and practice of the process of state registration of small innovative enterprises (SIEs) at institutions of higher education and scientific organizations to ensure the reliability, verification and accuracy of its results presupposed the use of a complex of theoretical (analysis, synthesis, comparison, analogy, induction, deduction, idealization, modeling, etc.) and empirical methods (survey, expert evaluation, document analysis, observation, etc.). The authors of this article used a complex approach with technologies of system and structural-functional analysis. The results were processed by mathematical and statistical methods to establish relationships and dependencies among the indicators of the processes studied.

As shown by the results of practice examination, the following properties of systems need to be considered in the process of state accounting: the availability of links among the elements; integrity; emergence, divisibility, communication ability, subsidiarity; multifunctionality; flexibility; adaptability; reliability; security, vulnerability, structuredness, dynamism, sustainability, etc. The process of state accounting is influenced by both positive and negative factors, which determines the development and implementation of a special methodology, i.e. definition of a set of laws (from dialectical to the laws governing the management of social phenomena), regularities (the dependencies of phenomena on the surrounding conditions), principles (special accounting rules), and methods (a set of assets, means of influence on the accounting process) of this specific activity. In this regard, reliable, accurate and effective accounting is possible if it is complex, i.e. combines the administrative and mechanistic elements of information control.

The methodology of state accounting, interpreting the basic scientific principles of public management, a priori should include the following laws:

1) Unity and integrity of the accounting system.

2) Provision of the required number of degrees of freedom of the accounting system. The number of degrees is limited by various regulations, customs, traditions, and ideologies. A balance of freedoms is required. The restriction of freedom of accounting can reduce the level of reliability of accounting, while excessive freedom can result in various delicts.

3) The necessary variety of accounting systems. The law allows changing the complex of accounting forms dynamically.

4) Correspondence and correlation of managing and the managed accounting systems. The systems must have uniform structures and functionality. Undoubtedly, the organization of state accounting includes systemic management laws: the more complex is the object, the more varied the accounting structure is; a vital (actualized) need for accounting should be met by a special structure.

These laws will be implemented if one follows the principles of regulation for any activity. The public accounting system, as shown by the results of practice observation, should respect the following principles: the principle of scientificity (to use the available theoretical knowledge); the principle of reliability (it is inadmissible to provide false data and operate with untested data and information about the enterprise); the principle of substantiality (all the data is important for assessing the quality of the company's operation); the principle of prudence (caution in analytical work with data and information, for example, in forecasting the prospects of SIEs; the principle of continuity (records are kept constantly); the principle of immediacy (the timeliness of action taken); the principle of continuity; the principle of complexity; the principle of unity of command and collegiality in activities; the principle of motivation; the principle of democratization of management; the principle of key element; the principle of control, etc.

The results of the practice analysis show that adherence to the principles of state accounting, including in case of SIEs, is possible in various ways (methods). The more methods are used in the accounting process, the more reliable, more accurate and more justified the results are. It is obvious that accounting by one method (for example, declarative) will subsequently lead to systemic mistakes in assessing the quality and trends of the company's development. Therefore, the most reliable accounting results can be obtained using complex theoretical and empirical methods (for example, see above the methods used in this study).

The analysis of foreign and domestic experience shows that the empirical basis for accounting can be data from tax inspections, audit materials of internal and external audit, proceedings from production meetings, enterprise plans, media materials, the results of participant observation, innovation projects content, patents, research and development (R&D) costs, compliance with international standards, etc.

As is known, in the context of integration of socio-economic and other relations, the level of global competition increases, and the advantage is given to a state that has greater scientific potential and quickly ensures its practical implementation. In Russia, the success of the national innovative development depends, primarily, on the effectiveness of business, science and education cooperation, including in the development of universities' innovation infrastructure and the creation of SIEs in accordance with the Federal Law No. 217-FZ (2009).

This normative document defines the right of state universities and scientific institutions, including subordinate state academies of sciences, to act as founders of economic societies engaged in the practical application (implementation) of the results of intellectual activity, the rights to which belong to these organizations. These institutions have also received the right, without the consent of the property owner, with notification of the Ministry of Education and Science of Russia, to be founders (including jointly with other persons) of economic societies (ESs) and economic partnerships (EPs), the activity of which consists in practical application (implementation) of intellectual property, exclusive rights to which belong to these institutions of education and science.

The adoption of the Federal Law No. 217-FZ has allowed including budget scientific and educational institutions in innovative activities and has become a significant stimulus for the development of the public sector of science and innovation.

At present, the activities of SIEs in higher education, in addition to the above-mentioned law, are directly or indirectly regulated by: Part 1 of the Civil Code of the Russian Federation (No. 51-FZ of November 30, 1994); Federal Law of January 12, 1996 No. 7 "On Non-Profit Organizations"; Federal Law of August 23, 1996 No. 127 "On Science and State Science and Technology Policy"; Federal Law of February 8, 1998 No. 14 "On Limited Liability Companies"; Federal Law of August 8, 2001 No. 129 "On State Registration of Legal Entities and Individual Entrepreneurs"; Federal Law of July 26, 2006 No. 135 "On Protection of Competition"; Federal Law of July 24, 2007 No. 209 "On the Development of Small and Medium-Sized Business in the Russian Federation"; Federal Law of November 27, 2010 No. 310 "On Amendments to Article 346.12 of the Tax Code of the Russian Federation"; Federal Law of March 1, 2011 No. 22 "On Amendments to Article 5 of the Federal Law "On Science and State Science and Technology Policy" and Article 17.1 of the Federal Law "On Protection of Competition"; Federal Law of December 29, 2012 No. 273 "On Education in the Russian Federation" (2012); Federal Law of December 29, 2015 No. 408-FZ "On Amendments to Certain Legislative Acts of the Russian Federation" (2016); Federal Law of July 3, 2016 No. 250-FZ (Article 18); Federal Law of July 3, 2016 No. 243-FZ, Subparagraph 1, Article 427 of the Tax Code of the Russian Federation (Part 2, Section VIII, Chapter 34), etc.

The legislative power, providing the activities of federal executive regulation in the sphere of innovation economy, continues to improve the normative legal base for SIE management.

For instance, the Federal Law of July 3, 2016 No. 250-FZ (Art. 18) has eliminated the Federal Law of July 24, 2009 No. 212-FZ "On Insurance Contributions to the Russian Federation State Pension Fund, Social Insurance Fund of the Russian Federation, Federal Compulsory Medical Insurance Fund"; Federal law of July 3, 2016 No. 243-FZ, subparagraph 1, Art. 427 of the Tax Code of the Russian Federation (Part 2, Section VIII, Chapter 34) has established reduced tariffs for insurance contributions for ESs (EPs) created in the scientific and educational sphere, including mandatory pension insurance in 2017 – 8.0%, in 2018 – 13.0%, in 2019 – 20.0%.

The analysis of the main regulatory legal acts regulating the activity of subjects of innovation activity and the frequency of their refinement suggests the need for development of a special legal code.

It is obvious that in the market economy conditions, SIEs are the best form of practical verification (examination) of scientific and technical developments, inventions, rationalizations. They are the most effective experimental platform, the production laboratory of higher education and research institutes (Metodika postroeniya "Reitinga vuzov RF – 2017", 2017). Such enterprises stimulate the search activity of scientific personnel, create jobs for talented youth, reduce the flow of specialists' migration to the Western economy and make the specialties obtained at higher educational institutions attractive.

The results of practice examination show that SIEs, like all new systems, are subject to special risks. They are currently experiencing complex economic relations, being the desired target of various competitors; therefore, they must be considered and receive state support and protection. Such enterprises stabilize political and public relations. For example, the development of innovative technologies significantly increases the level of both economic and political activity of the population, which, of course, leads to their social and economic stability. For example, the results of correlation analysis show a strong and stable relationship between the number of SIEs in higher education and the growing number of applicants (k = 0.72), the number of violations (k = 0.69) and students' activity in the university life (k = 0.61). And the results of the regression analysis (simple linear regression) showed that the lower the level of entrepreneurship development (SIEs are part of the business sector), the lower the level of legitimacy of state power and, accordingly, the quality of the process of ensuring all types of the national security. The fact is known that after the tax pressing carried out in 2012, 674 thousand entrepreneurs have left the business (Orekhin, 2016). Presumably, even more unregistered people were living for such earnings, who also quit their jobs. At the same time, even according to the official figures, the turnout of the electorate for municipal elections has decreased from 43% in 2012 to 35% in 2014 (Demchenko, et al., 2016, p. 87). Undoubtedly, a significant part of citizens who ignored the elections is an active part of society – entrepreneurs.

The above-mentioned points to the need for continuous capacity building for the management of the SIE system. Here it is necessary to fulfill the well-known law of management of public systems: the more complex the object is, the more complex the management system is (Demchenko & Gostev, 2013, p. 117). Certainly, the main element of the management algorithm is control (accounting). Public funding, tax incentives, organization of additional jobs, provision of various other advantages to SIEs in the social and economic sphere place an obligation on the federal executive authorities to organize and implement permanent systematic administrative control of the activities of institutions of higher education and scientific organizations.

The experience of innovation activities in foreign countries is of great interest. The results of the analysis of scientific literature (Gostev, 2016; Gostev & Demidova, 2015; Gostev & Serikova, 2016; Demchenko, et al., 2016; Turko, et al., 2016; Teivans-Treinovskis, et al., 2017; Fedorkov, et al., 2017; Shchepanskiy, et al., 2016) show that it is extremely diverse. This fact might be explained by the socio-economic characteristics of certain countries. The study of Western accounting experience, control and organization of the companies' vital functions show that they are based on highly developed public relations regulated by centuries-old traditions of civil society (Gostev & Serikova, 2016, p. 78).

The results of the documentary analysis of practice in specific countries of the Western civilization (England, USA, Germany, and France) show that these countries implement systematic administrative and public accounting (control) for similar enterprises. Thus, if the government provides direct funding of research and development work on creation and use of innovations in the form of subsidies (about 50% of enterprises' costs in USA and France are budget-paid), it organizes accounting work and uses such indicators as: "financial control", "number and size of soft loans", etc. Thus, in Germany, preferential loans for general technological innovations account for up to 50% of the funds that the enterprise spends for these purposes, and in Italy – up to 80% of the cost of the innovative project for a period of up to 15 years (Turko, et al., 2016, p. 11199). Of course, this package includes proportional funding of organizations that exist directly at universities and other producers of innovative products. There are other accounting indicators: requests for tax breaks and vacations (indirect incentives the activities for business activities that ensure the implementation of scientific achievements); preferential treatment of depreciation (accelerated equipment depreciation, especially for high-tech equipment); preferences or full exemption from tax payments for the import of scientific and high-tech equipment; venture capital activity (capital, mainly provided by external private investors to finance new ventures); maturity of innovative infrastructure (organizational system to promote innovation: scientific and technological parks, innovation incubators, technology transfer centers, technopolises, clusters, etc.); tax exemptions and deferrals for payment of patent fees (in the United States up to 50% of protection documents cost is paid from the budget funds. Northwest University in the US earns about $200 million a year, while one of the Russian leading universities (according to the survey of 2016) – the National Research Mordovia State University – earned 5.8 million rubles in 2015); profit margins obtained using intellectual property (licenses, patents and know-how are taxed at a reduced rate) and so on. There is a special accounting indicator – the involvement of veteran specialists in science and education in the innovative activity. The results of documents (scientific publications) analysis showed that, for instance, in all the developed countries, there are counseling centers serviced by retirement-age specialists. Thus, in the USA there are 389 such consulting points, counting up to 11,400 of senior age specialists (Orekhin, 2016).

By the way, there is the Ministry of Veterans in the USA (with the number of veterans around 40 million) (Gostev & Demidova, 2015, p. 114), which facilitates the organization of work in the field of science and innovation.

At present, the Russian authorities have created administrative conditions for automated (mechanic, formal) accounting for the development of innovative activities of budgetary scientific and educational organizations. As mentioned above, one of the basic laws of social management is that any topical social problem should be solved by a special structure (organization, institution) particularly created for this purpose. Therefore, accounting must necessarily be carried out by a specialized structure, including a complex of diverse assets and means. The importance of such an organization is beyond doubt. Currently, this function is performed by the Federal State Budget Scientific Institution "Research Institute – Republican Research and Consulting Center of Expertise" (SRI FRCEC). The registration of notifications is entrusted to this organization by the order of the Ministry of Education and Science of the Russian Federation of January 24, 2014 No. 43 "On Organization of Accounting for the Notices on Establishment of Economic Societies and Economic Partnerships in the Ministry of Education and Science of the Russian Federation". In 2014, a technical model was developed – the interactive information system "Accounting and Monitoring of Small Innovative Enterprises in Scientific and Educational Sphere". This system hosts and updates: the database of ESs (EPs); quarterly registers; title documents; the procedure for notifications accounting on the establishment of ESs (EPs).

According to the Decree of the Government of the Russian Federation of March 4, 2011 No. 146 (2011) and the Order of the Ministry of Education and Science of Russia of February 14, 2014 No. 117, the Register form was approved, which contains the following information: a) full and abbreviated (if applicable) name of the scientific institution (educational institution of higher education) that has created an ES (EP), along with its department affiliation; b) full and abbreviated (if available) company name of the ES (EP); c) the address (location) of the permanent executive body of the ES (EP); d) primary state registration number, under which the record on creation of a legal entity has been made assigned to the ES (EP); e) taxpayer identification number assigned to the ES (EP); e) the number and date of registration of the ES (EP) as an insurer in the regional bodies of the Pension Fund of the Russian Federation and the Social Security Fund of the Russian Federation; g) the date of inclusion in the register; h) the date of exclusion from the register.

The information system "Accounting and Monitoring of Small Innovative Enterprises in the Scientific and Educational Sphere" provides automated recording of notifications on the establishment of ESs (EPs); storage, processing, updating of information, publication on the site, automatic formation of the Register, reports to the Ministry of Education and Science of Russia, as well as monitoring their activities. Notifications on the establishment of ESs (EPs) are shown in the Tab "ES (EP) Database" on the main page of the website mip.extech.ru and are updated online. The information on previously established ESs (EPs) is available both in the general database and via the user menu for the authorized users.

All the accounting procedures for the establishment of ESs (EPs) as well as updates on their current state are performed on the above website.

Each user (participant in the process) receives a unique identifier (login and password), which is his permanent pass for authorization on the website. System users are representatives from universities and research institutes responsible for creation and operation of ESs (EPs).

When completing the online registration form for the ES (EP), the following information on the ES (EP) and its parent organization is entered in the database of notifications on the establishment of ESs (EPs) of the Ministry of Education of Russia: the full name and number of OGRN, address, priority directions for development, critical technologies, codes of OKVED (the All-Russian Classifier of Types of Economic Activity), size of authorized (depositary) capital of the ES (EP), the date of transition to the simplified tax system, the license type, the number of license agreement, the Rospatent number, the type and name of the result of innovation activity (RIA), the number of a title document to the RIA, information on the statement of RIA on the balance sheet of accounting, the monetary value of RIA under the license agreement in rubles, etc.

The accuracy of the data is confirmed by documents uploaded by the representatives of the parent institution in pdf format to the system:

– Extract from the Unified State Register of Legal Entities (EGRUL). The date of issuance must correspond to the date of ES registration.

– Certificate of Primary State Registration Number (OGRN).

– Notice of registration in the territorial bodies of the Pension Fund of the Russian Federation.

– Notification of registration in the Social Insurance Fund of the Russian Federation.

In addition, data are presented confirming the rights of the holder of rights to the RIA:

- The title page of the patent, if the RIA is an invention, utility model, industrial design (registration of the RIAs in Rospatent), selective achievement (if the RIA is registered in the Ministry of Agriculture of the Russian Federation).

- A certificate (if the RIA is registered with Rospatent).

- A computer program, a database, a topology of integrated microcircuits.

- If the RIA is not registered with Rospatent, then an order or an extract from the protocol of the scientific council (scientific and technical council) is required to introduce the confidentiality (business secret) regime, or an extract from the minutes of the meeting of the expert commission, or an extract from the register of the results of intellectual activity of the university (research institute) with the specification of the validity term for the commercial secret regime.

- A document confirming the registration of the RIA as an intangible asset on the parent organization's account (an inventory card from the accounting department with the signature of the accountant or a certificate with the signature of the accountant).

- A license agreement if the RIA is a computer program, a database, a topology of integrated microcircuits or know-how.

– A license agreement registered with Rospatent (or the Ministry of Agriculture of the Russian Federation) and a certificate of registration ("Appendix to the patent with a registration number ...") if the RIA is an invention, a utility model or an industrial design.

The data is additionally checked by the system administrator for reliability, accuracy, compliance with the legislation and, in case of assigning the status "Corresponds to 217-FZ", the ES (EP) is transferred from temporary to the main notification database and is entered in the Register. Thus, the Register is formed as a result of work of the accounting and verification database for notifications on creation of ESs (EPs), which subsequently send notifications generated by this system to the Ministry of Education and Science of the Russian Federation.

The Register does not include ESs (EPs), if there is no information on the license contract conclusion, if at the time of the ES (EP) registration the founder has only deposited some funds, if the RIA type does not comply with the legal norms, if the agreement on the alienation of the RIA has been drawn up.

As can be seen, in practice the system created by SRI FRCEC, in fact, does not only record applications (declarative presentation of data), but also implements administrative and public control over its reliability. For example, the organizations responsible for the implementation of public control include scientific (scientific and technical) councils of the universities, research institutes, and various expert commissions. Of course, the range of such organizations could be expanded, which corresponds to such a methodology as providing the required number of degrees of freedom and diversity of accounting systems.

Until 2017, the Register was sent quarterly to the Ministry of Education and Science of the Russian Federation for its further transfer to the Pension Fund of the Russian Federation and the Social Insurance Fund of the Russian Federation, and since the 1st quarter of 2017, in accordance with the Decree of the Government of the Russian Federation of February 4, 2017 No. 136 – to the Federal Tax Service of the Russian Federation. Thus, the system of administrative accounting is being improved.

The register for the next quarter, signed by the Deputy Minister of Education and Science of the Russian Federation, is published in the information system "Accounting and Monitoring of Small Innovative Enterprises in the Scientific and Educational Sphere" in the "Registry" tab.

The analysis of the Register contents showed that in the first quarter of 2017 it contained information on 2,645 ESs (EPs), in the 2nd quarter – on 2,678, in the 3rd quarter – on 2,709, in the 4th quarter – on 2,753.

The Ministry of Education and Science of Russia is instructed to submit an annual list of ESs (EPs) in the unified register of subjects of small and medium-sized business, the main activity of which is the practical application (implementation) of RIA. The format of the information (the structure of the information format file) is defined and approved by the order of the Federal Tax Service of Russia of 16 March 2016 No. MMV-7-6/145. On this basis, on July 1, 2017 the Federal State Budget Scientific Institution SRI FRCEC has formed a list of such ESs (EPs) in the xml format, which contained information on 2,470 ESs (EPs).

The document analysis results showed that the work to increase availability of the mip.extech.ru for administrators and users continues unabated. For example, changes were made to the registration of users.

In accordance with Article 9 of the Federal Law of the Russian Federation No. 152-FZ of July 27, 2006 "On Personal Data", by the Order of the Federal Service for Supervision of Communications, Information Technologies and Mass Communications in the Central Federal District of July 6, 2017 No. 170 the Federal State Budget Scientific Institution SRI FRCEC was included in the register of operators performing the processing of personal data under the registration number 77-17-006120. In this regard, upon registration the system now requests consent to the storage and processing of personal data.

The results of the accounting analysis show that there are no registered economic partnerships (EPs) in the database. It is likely that this form of incorporation is either not interesting for the founders or does not have full legal provisions regarding the responsibility of co-founders in force majeure cases. As of November 1, 2017, 2,884 notifications on the establishment of ESs have been included in the database, of which: 2,611 were created in 303 universities, 273 – in 133 research institutes. The largest number of SIEs was organized in the Ministry of Education and Science of the Russian Federation. There 206 founding universities (47.14% of all founders) have created 2,196 SIEs (75.62% of the total number). In the Federal Agency for Scientific Organizations, 237 SIEs (8.16%) have been established in 118 research institutes (27%).

The ES' founders have established the right over 2,885 RIAs in the authorized capital. This fact suggests that the commercialization of RIA becomes a condition of ES (EP) establishment.

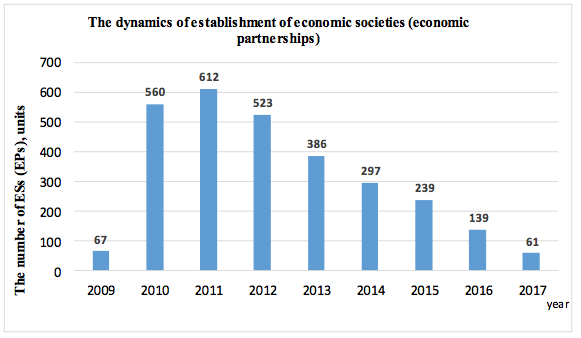

The results of the data analysis for the registration of notifications on establishment of ESs (EPs) show that there has been a steady trend of an annual reduction in the number of new organizations since 2011 (Figure 1), which reflects, first, the need to create more effective mechanisms for managing this area; and secondly, probably to strengthen the government control over the quality and effectiveness of such organizations and the responsibility for presenting inaccurate information. In addition, unified programs of Russian and Western universities have created conditions for migration of personnel to the Western countries. In this regard, it should be concluded that the current provision of conditions for establishment and development of SIEs should be systematic, complex and apply to all state and public structures.

Figure 1

The dynamics of establishment of economic societies (economic partnerships)

year by year (as of November 1, 2017)

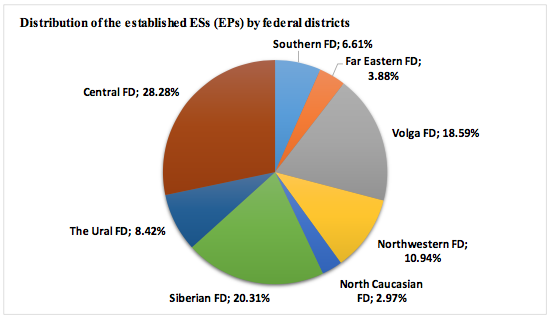

Other results have been determined. Thus, the largest number of ESs was created in the Central, Siberian and Volga Federal Districts (Figure 2).

Figure 2

Distribution of the established economic societies

and economic partnerships by federal districts

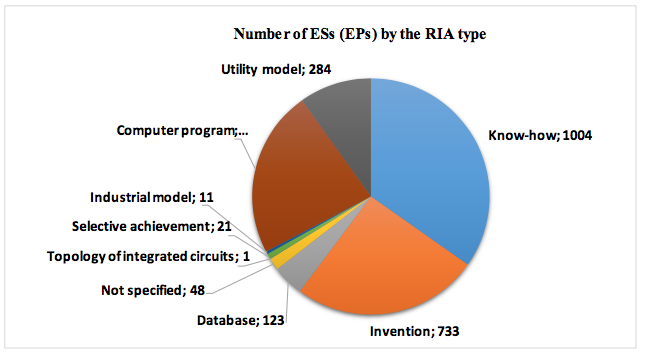

And the most successfully implemented results of intellectual activity have become know-how, inventions and computer programs (Figure 3).

Figure 3

Number of economic societies and

economic partnerships by the RIA type

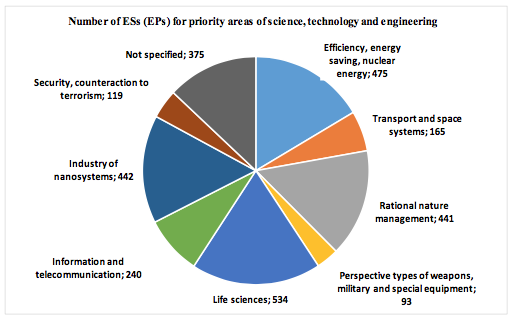

The most priority areas for the development of science, technology and engineering with the greatest number of ESs were: "life sciences", "energy", "industry of nanosystems", rational nature management (Figure 4).

Figure 4

Number of economic societies and economic partnerships

for priority areas of science, technology and engineering

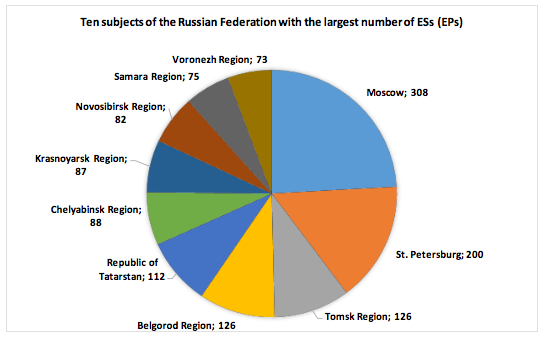

The largest number of ESs was created in the following subjects of the Russian Federation: Moscow, St. Petersburg, and the Tomsk Region (Figure 5).

Figure 5

Ten subjects of the Russian Federation with the largest

number of economic societies and economic partnerships

As can be seen, the accounting information system is of great practical importance for the country's innovation economy, since it contains information that allows identifying the actively developing innovative activities of the territory, identifying the most relevant RIA and priority areas for the development of science, technology and engineering.

The main results of the research, described in the article, were submitted for evaluation to the Roster of Experts of the Federal State Budget Scientific Institution "Research Institute – Republican Research and Consulting Center of Expertise" (Federal State Budget Scientific Institution SRI FRCEC), with 4,208 of accredited experts; were discussed at the XI International Scientific and Practical Conference "Production Management: Theory, Methodology, Practice" (Novosibirsk, December 7, 2017). Positive feedback was received.

State accounting, including the registration of notifications for the establishment of SIEs, is part of the management system, which is implemented according to a special methodology, including general and particular laws of social management, principles and methods.

The number of annually established ESs (EPs) decreases, which on the one hand demonstrates the completeness of RIA implementation in practice, and an increase in the level of standards for the accounting of SIE; on the other hand – of the inadequate effectiveness of state regulation of this process.

High rates of quantitative growth were replaced by stabilization. The first result of the inventory of ESs (EPs) established by the institutions of higher education became apparent to decide on the expediency of those units, the development prospects of which are disputed. This process is connected not only with economic reasons, but also with the inadequate human capacity of higher educational institutions, ready to engage in entrepreneurial activities.

A transition to the new principles of state policy with respect to the innovation activity of ESs (EPs) is required.

1. Considering the importance of innovative development in the interests of ensuring national security, it is necessary to develop and propose to the legislator a special code containing systematized norms regulating the innovative activity of the most important social and economic branches of the country.

2. To ensure accounting of opinions and judgments of participants in the educational process on activities and status of innovative enterprises in the system of state accounting of SIEs at institutions of higher education and scientific organizations.

The research was performed within the framework of the state assignment No. 074-00497-18-02 of the Ministry of Education and Science of the Russian Federation for 2018 under the project "Methodological support of measures for monitoring and state registration of small innovative enterprises in institutions of higher education and scientific organizations" (Code: 29.12269.2018 / 12.1).

1. Gostev, A.N. (2016). Obshchestvennye mekhanizmy vovlecheniya naseleniya v sistemu razrabotki obrazovatelnoi politiki Rossiiskoi Federatsii [Social Mechanisms of Public Involvement in the Development of the Educational Policy of the Russian Federation]. Sotsiologiya obrazovaniya, 8,80-100.

2. Gostev, A.N., & Demidova, S.S. (2015). Obshchestvennyi control proizvodstvennykh kompanii: sostoyanie, formy [Public control of Production Companies: State, Forms]. Vestnik Adygeiskogo gosudarstvennogo universiteta. Seriya "Regionovedenie: filosofiya, istoriya, sotsiologiya, politologiya, kulturologiya", 3, 108-116.

3. Gostev, A.N., & Serikova, V.P. (2016). Upravlenie vysshim obrazovaniem: Rossiiskie traditsii: Monografiya [Higher Education Governance: Russian Tradition: Monograph]. Moscow: Modern Humanitarian Academy. (p. 177).

4. Demchenko, T.S., & Gostev, A.N. (2013). Upravlenie informatsionno-psikhologicheskoi zashchitoi sotsialnoi organizatsii: Monografiya [Management of Information and psychological Protection of Social Organization: Monograph]. Moscow: Modern Humanitarian Academy. (p. 224).

5. Demchenko, T.S., Kasyuk, A.Y., Andrerzhanova, G.V., Gostev, A.N. et al. (2016). Kachestvo stolichnogo obrazovaniya v otsenkakh osnovnykh subektov obrazovatelnogo protsessa. Monografiya [Quality of the Metropolitan Education in Assessments of the Key Subjects of the Educational Process. Monograph]. Moscow: RU-SCIENCE. (p. 294).

6. Metodika postroeniya "Reitinga vuzov RF – 2017" [Methodology for Determining the "Rating of Russian Universities – 2017"]. (2017). Retrieved from http://docplayer.ru/68162325-Metodika-postroeniya-reytinga-vuzov-rf-2017-po-pokazatelyam-vostrebovannosti-produktov-deyatelnosti.html

7. Postanovlenie Pravitelstva Rossiiskoi Federatsii No. 146 "O vedenii reestra ucheta uvedomlenii o sozdanii khozyaistvennykh obshchestv, sozdannykh byudzhetnymi nauchnymi i obrazovatelnymi uchrezhdeniyami vysshego professionalnogo obrazovaniya, i poryadke ego peredachi v organy kontrolya za uplatoi strakhovykh vznosov" [The Decree of the Government of the Russian Federation No. 146 "On Keeping the Register of Account Notification of Creation of Economic Societies Created by Budgetary Scientific and Educational Institutions of Higher Professional Education, and the Manner of Its Transfer to the Bodies of Control over Payment of Insurance Contributions"]. Sobranie Zakonodatel’stva Rossiiskoi Federatsii [SZ RF] [Collection of Legislation of the RF] 07.03.2011, No.10, Item 1416.

8. Orekhin, P. (2016, July 26). Rossiya na nelegalnom polozhenii [Russia in an Irregular Situation]. Retrieved from https://www.gazeta.ru/business/2016/07/21/9703877.shtml

9. Turko, T.I., Gostev, A.N., & Shchepanskiy, S.B. (2016). Social Mechanisms in Elaborating Russian Educational Policy: Legal Monitoring. International Journal of Environmental and Science Education, 11(18), 11195-11218.

10. Teivans-Treinovskis, J., Lavrinenko, O., & Jefimovs, N. (2017). Issues in the Area of Secure Development: Trust as an Innovative System's Economic Growth Factor of Border Regions (Latvia-Lithuania-Belarus). Journal of Security and Sustainability Issues, 6(3), 435-444.

11. Federalnyi zakon No. 217-FZ "O vnesenii izmenenii v otdelnye akty Rossiiskoi Federatsii po voprosam sozdaniya byudzhetnymi nauchnymi i obrazovatelnymi uchrezhdeniyami khozyaistvennykh obshchestv v tselyakh prakticheskogo primeneniya (vnedreniya) rezultatov intellektualnoi deyatelnosti" [Federal Law No. 217-FZ "On Amendments to Certain Legislative Acts of the Russian Federation on the Establishment of Budget Scientific and Educational Institutions, Business Entities with a View to Practical Application (Implementation) of the Results of Intellectual Activity"]. Sobranie Zakonodatel’stva Rossiiskoi Federatsii [SZ RF] [Collection of Legislation of the RF] 03.08.2009, No. 31, Item 3923.

12. Federalnyi zakon No. 273-FZ "Ob obrazovanii v Rossiiskoi Federatsii"[Federal Law of the Russian Federation No. 273-FZ "About Education in the Russian Federation"]. Sobranie Zakonodatel’stva Rossiiskoi Federatsii [SZ RF] [Collection of Legislation of the RF] 31.12.2012, No. 53 (I), Item 7598.

13. Federalnyi zakon No. 408-FZ "O vnesenii izmenenii v otdelnye zakonodatelnye akty Rossiiskoi Federatsii" [Federal Law No. 408-FZ "On the Amendments to Individual Legislative Acts of the Russian Federation"]. Sobranie Zakonodatel’stva Rossiiskoi Federatsii [SZ RF] [Collection of Legislation of the RF] 04.01.2016, No. 1(I), Item 28.

14. Fedorkov, V.F., Turko, T.I., Fakhurdinov, O.V., & Timokhin, A.A. (2017). Analiz ucheta malykh innovatsionnykh predpriyatii, sozdannykh v sfere obrazovaniya i nauki [Analysis of Accounting for Small Innovative Enterprises Established in Education and Science]. Innovatikaiekspertiza, 2(20), 24-32.

15. Shchepanskiy, S.B., Glisin, F.F., Kaluzhnyi, V.V., & Melnik, P.B. (2016). Criteria for Evaluation and Planning of Science Foundation Activity. International Review of Management and Marketing, 6(S3), 190-194.

1. Scientific Research Institute – Federal Research Centre for Projects Evaluation and Consulting Services), Antonova-Ovseenko St. 13, b. 1, Moscow, Russia, 123317. E-mail: gostevan@inbox.ru

2. Scientific Research Institute – Federal Research Centre for Projects Evaluation and Consulting Services), Antonova-Ovseenko St. 13, b. 1, Moscow, Russia

3. Scientific Innovation Measures of the Federal State Budget Scientific Institution, Scientific Research Institute – Federal Research Centre for Projects Evaluation and Consulting Services), Antonova-Ovseenko St. 13, b. 1, Moscow, Russia

4. Kutafin Moscow State Law University, Sadovaya-Kudrinskaya St. 9, Moscow, Russia