![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 39 (Number 47) Year 2018. Page 19

Liudmila I. KHORUZHY 1; Vladimir M. BAUTIN 2; Yuriy N. KATKOV 3; Elena I. STEPANENKO 4; Boris V. LUKYANOV 5

Received: 28/05/2018 • Approved: 13/07/2018

ABSTRACT: The paper details theoretical aspects of approach to internal controls system. It describes the importance of managerial accounting for efficient management and performance of internal controls. Special attention is paid to connections between cybernetics and modern monitoring and control systems. The adaptive internal controls system is suggested and validated for managerial monitoring and control in agrarian organizations. Implementation of this system into operations of agrarian organizations allows them to efficiently monitor all business processes under varied economy management. |

RESUMEN: En el artículo se revelan los aspectos teóricos de modo de enfocar el sistema de control interno. Se señala el papel de contabilidad de gestión en la organización y ejecución efectiva del control interno. Se presta una atención especial al estudio de la relación entre la cibernética y sistemas modernos de gestión y control. Se propone y argumenta el sistema adaptable de control interno para la ejecución de monitoreo y gestión de la actividad de las organizaciones de agrosfera. La introducción de este sistema en las actividades prácticas de las organizaciones agrarias permite realizar un monitoreo eficaz por todos los procesos de negocio en las condiciones variables de gestión económica. |

One of the reasons for the high costs and low final financial gain of operations of agricultural organizations in Russia are asset losses due to the lack of an efficiently operating internal controls system. However, not all agricultural organizations pay due attention to the management of the internal control system since there are no clear regulatory standards for the implementation of these processes in agricultural entities.

Given that agribusiness is a complex economic system combining both industrial and agricultural operations, for many agricultural organizations it makes sense to approach the internal controls as a system integrated into all business processes of the company and able to generalize the information and bring the results to attention of authorized controllers in due time. Building and running of the internal controls system must promote cooperation between all internal control subjects in order to achieve the goals and key objectives of the company, which are focused on progress and quality improvement as well as minimization of risks, improving the resource management efficiency, and the financial standing of the entity.

The issues of methods and management of internal control and audit are discussed in studies by V.V. Burtsev (2002), P. Druker (1964), M.V. Melnik (2003), B. Ryan (2002) V.P. Suiz (2006), and A.D. Shermet (2006), who focus their attention on managerial and economic basics and areas for development of internal controls in organizations.

The works of N.N. Azanova (2013), S.A. Diveeva (2014), T.V. Kokovkina (2014) are of certain importance in eliminating quite a number of problems in managing, evaluation, and performance of internal control system.

A.A. Alborov (2015), N.G. Belov (2006), G.R. Konzevoy (2015), S.R. Konzevaya (2015), G.Y. Ostayev (2015), and L.I. Khoruzhy (2013) made a notable contribution into developing the internal controls both in theory and practice particularly in agribusiness.

In English, the term CONTROL can mean both to monitor and to manage, and it is a much broader concept including the subsequent corrective actions. Control as a function of management allows you to promptly identify and eliminate those conditions and factors that do not contribute to the efficient performance and achievement of goals. It helps to structurize the activities in an organization or its individual business units, determines which services and units as well as activities contribute to achievement of goals and increase the efficiency of operations. It acts as a means of feedback between the control object and the control system informing of the actual status of the control object and actual performance of the managerial decision. Control is the process that ensures that the actual results match the plan. The control process involves setting targets or standards, against which actual results are compared. During operation the performance indicators are measured from time to time and compared with the target values. Accountant analysts should provide managers with information about this as a feedback, issue regular reports and analyzes in a form that allows managers to determine whether operations are in accordance with the plan or not and to identify those activities, where corrective actions are necessary. In particular, one of the functions of management accounting is to provide managers with economically important information that helps to control costs and improve the efficiency and productivity of operations (Ryan, 1998). Thus, control is a kind of compass, using which you can direct and coordinate the work of all employees in the organization to achieve the goals.

Internal control in organizations is arranged into a system, which is understood as the interaction of subjects of internal control in each separate business unit or business process, which in turn applies methods, rules, and control procedures established by the management of the company to achieve the desired goals.

For global practices it is common to use concept documents developed by the non-profit organization – Committee of Sponsoring Organizations of the Treadway Commission (COSO) as methodological foundation for management of internal controls. COSO risk management model for organizations is considered to be the most effective, widely used in the field, and is taken as the basis for building an internal control system regardless of the industry affiliation. The main idea of this model is to focus on risk management of economic entities and the optimum balance between profits and risks, efficient use of resources, to achieve the main objectives of the company (Shapoval and Kostikova, 2018).

The main objective of the internal control system is to provide reliable information on the economic activities of the organization, identify associated threats and risks.

Key elements of internal controls are: control environment, risk assessment, internal control procedures, information and communication, and internal control evaluation (Burtsev, 2002).

Control environment is a set of principles and standards for the operations of the economic entity. These principles and standards give a common understanding of internal control and requirements to its arrangement at a level of an economic entity. Control environment should reflect the management culture of the economic entity and create the proper attitude of the staff to the company and internal control operations (Alaverdova, 2014).

Risk assessment is a process of identifying and analyzing risks, that is, combining the likelihood and consequences of failure by an economic entity to achieve the objectives of its business. By identifying such risks the economic entity must make appropriate decisions to manage these risks. Risk management is possible by creating the necessary control environment, selecting and structurizing separate internal control procedures, choosing methods and ways to evaluate the results of internal control as well as inform the staff.

Internal control procedures are based on the principles and standards that make up the control environment of the economic entity and are applied as dictated by its characteristics. The economic entity may apply such internal control procedures as documenting; confirmation of compliance of several objects (documents) or compliance with the established requirements; authorization of business operation items, which confirms the legality of such item; reconciliation of data; delineation of powers and rotation of duties; physical audit; supervision; procedures related to computer processing of data and data systems; etc. (Boboshko, 2015).

Without quality and timely information it is impossible to ensure the proper functioning of internal controls and the ability to achieve its goals. Information system should be able to maintain accounting records and compile accounting (financial) statements. Distribution of the information necessary for making managerial decisions and implementing internal controls is performed by means of such internal control element as communication.

Internal control evaluation is performed for all other elements of internal control in order to determine their efficiency and delivery as well as the need for changes to individual elements. The scope and nature of methods and ways to evaluate the internal controls are established by the head of the economic entity or the head of the relevant business unit (Butyrin, 2011).

In order to achieve the objectives of the structural design of a system for monitoring and developing indicators of the effectiveness of the internal control system at agricultural organizations, there are two ways of managing the control services:

a separate structure in the form of an internal control department under the supervision of the General Director;

all departments and services of the company are endowed with control functions.

The choice depends on the anticipated scope of work, structural and industry specific features of the company, territorial disunity, qualifications of personnel, etc.

The procedure for arrangement of internal controls including duties and powers of business units and personnel is determined by the head of the economic entity depending on the nature and scale of the company and features of its management system. When building the internal controls it is assumed that internal controls will be present at all levels of management of the economic entity and in all its divisions, all personnel will participate in the internal control in accordance with their functions and powers, and the usefulness of internal control must be consistent with the costs of its building and running.

The goal of this study is to generalize the theoretical foundations and build an adaptive system model of internal controls with a cybernetics component for agrarian organizations.

In order to achieve the said goal the following problems have to be solved:

- review and generalize the theoretical aspects of internal control approaches and based on the works of Russian and foreign authors;

- outline the grounds for the using management accounting as the data base for efficient internal controls system;

- shape the adaptive internal controls system to monitor and control the performance of agrarian organizations.

This paper was prepared using the following research methods: monographic, calculation and design, abstract and logical, method of comparison, and simulation method.

The efficiency of managerial decisions largely depends on the reliability of the financial statements, but in any organization there is a possibility of data corruption in reports. The reasons include errors in the processing and accounting of primary and consolidated documents, misconduct of personnel, etc. In this regard, there comes a need to build such an internal control system that will be able to adapt to the business conditions, respond in a timely manner to any changes, and run automatically. To solve this problem we suggest the management accounting system as an information and instrumental basis.

Management accounting is the dominant type of control. There are several reasons for this. First, all organizations need to have, and in aggregated form, results on a wide range of multiple activities using the common indicators. Perhaps the best indicators here would be monetary indicators. Second, profitability and liquidity are the most important characteristics that testify to the degree of success of all organizations; therefore, financial indicators in these areas and closely related neighbors are closely monitored by shareholders and other persons interested in the performance of the organization. Therefore, naturally, managers tend to monitor performance indicators in terms of money. Thirdly, financial indicators allow managers involved in alternative option analysis to take a single approach when making decisions. The option of action will be favorable for the company only if as a result of its choice and implementation its financial performance indicators run higher. Fourth, measurement of results in monetary terms gives managers a greater degree of autonomy. When the results of managers in a generalized form are presented as financial indicators, it allows managers to choose the action they deem most appropriate and contribute to the desired results. Finally, the results expressed in terms of money continue to be an effective indicator even in conditions of uncertainty, when it is not clear which course to take. In other words, financial results become a mechanism that indicates whether the actions taken by the organization are beneficial for the business.

References on management types of control traditionally see the results-based management as an analogue of a simple cybernetic system. To understand the contents and functionality of such systems, let's look at the concept of 'cybernetics'.

Cybernetics is the science of control processes in complex dynamic systems based on the theoretical foundation of mathematics and logic (generally, in formal languages), as well as on the use of computer technology (computers). The main method of cybernetics is the simulation method for systems and control processes.

Cybernetics, as it were, exist independently of technical means – computers taking the same position in relation to cybernetics as physical instruments with respect to physics. Cybernetics creates structure from unstructured problems. Cybernetics develops the principles of automated machine engineering and explores the possibilities of automation with their help of processes of mental labor.

When describing the functioning of a simple cybernetic system, authors often use a mechanical model, e.g. a thermostat, used by the central heating system for control. Such control system includes the following elements:

1. Process (maintaining the room temperature) is constantly monitored by means of an automatic controller (thermostat).

2. Deviations from the preset level (the desired temperature) are detected using an automatic controller.

3. Control actions begin in the event that the expected result (temperature) does not match the preset level. The automatic controller changes the initial parameters including the preheater if the temperature falls below a preset level. When the result (temperature) matches the preset level, the heater is turned off.

The final result of the process is continuously monitored: if the result deviates from the specified level, the supply of initial utilities is automatically adjusted. Emmanuel et al. (1990) argue that in order to talk about the controllability of any process, it is necessary to meet four conditions. First, there must be a process to be controlled. Without a goal to be achieved or a task to be solved control becomes meaningless. Secondly, the result of the process should be measurable given the characteristics of the controlled process. In other words, there must be some mechanism to make sure that the process goes in the given direction. Thirdly, it is necessary to have a process model that allows to predict its progress, to identify the reasons for which the expected result may not be obtained, and to propose corrective action with an appropriate assessment of efficiency. Finally, there should be an opportunity to take these action resulting in elimination of the deviation of the registered parameters from the target ones. If at least one of the above conditions fails, it is impossible to say that the process is under control.

The results-based management is much like the thermostat operation model. Standards are first defined for performance indicators, which are monitored by control systems. Then it compares target and actual parameters and identifies the resulting deviation, which becomes a signal for response, i.e. control action (Drury, 2013).

Operation of a simple cybernetic system is known as feedback control. Feedback control includes: control of product output compared to the target result and action in case of deviation, if necessary. Considering the specifics of feedback in cybernetic systems, L.A. Petrushenko (1967) points out that the cybernetic concept of feedback does not end in notion of inverse action or to the concept of a physical feedback channel. For cybernetic systems, not every feedback is important, but first and foremost one that provides a controlling feedback through the transfer of relevant information. The result of the controlling action is to maintain the state of the system or enhance it. Feedforward control rather than comparing the actual results with the specified ones provides estimates of the expected result to one or another point in the future. If these estimates differ from the scheduled indicators, appropriate actions are taken to reduce the future differences to a minimum. The main goal here is to establish control before any deviations of the target result appear. In other words, in case of feedforward control potential errors can be eliminated, i. e. actions are taken to avoid them, while in the case of feedback control actual errors are identified after they are done, and the adjustments are made so that in the future the results obtained match the preset values.

To implement the feedforward control a predictive model with a sufficiently high degree of reliability of future results is required, since without it the corrective action taken can not only fail to minimize the expected deviation, but, on the contrary, take it higher, i.e. worsen the situation. The main drawback of the feedback control is that when it is applied, an error is allowed to occur. If error detection is fast enough, then there is no big trouble since the required corrective actions in this case are taken in due time. In other words, feedforward control is preferable when the time interval between the detection of a deviation and its occurrence is significant. Preparation of estimates can be classified as a feedforward control operation. To the extent that the results obtained differ from the scheduled ones, consideration of alternative options takes place, and eventually such estimates are prepared, which as expected will be implemented with the specified targets. An example of feedback control is the comparison of actual results with estimates to identify deviations from the estimate and implement corrective actions. Thus, management accounting systems combine elements of both feedback and feedforward approaches (Katkov, 2010).

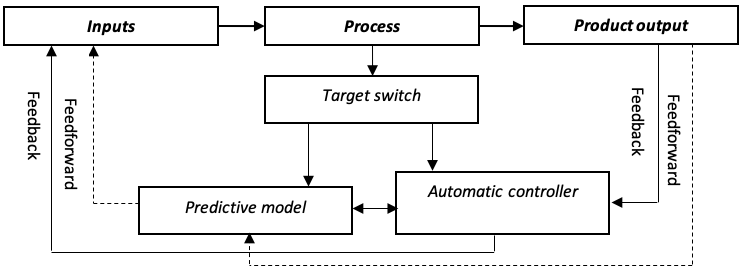

In connection with the above, we have developed a model of an adaptive internal control system with a cybernetic component, which in its core combines both feedforward and feedback controls (Figure 1).

Figure 1

Model of an adaptive internal control system with a cybernetic component

Source: the authors

Such a system due to joint relations and a combination of two different data flows is called an adaptive internal controls system. The presented system meets the requirements of management accounting o the fullest extent possible and contains author elements such as 'target switch', 'predictive model', and 'automatic controller' making the system universal for various processes.

'Target switch' element is necessary for the system to switch depending on the content of the process to feedforward or feedback. It makes the control system self-sufficient and autonomous.

'Automatic controller' element performs correction functions making the control system cybernetic and interacts with both feedback and feedforward. It changes the initial parameters depending on the developing situation and maintains the system in a stable state.

'Predictive model' element is there for the feedforward communications, allows to prevent errors before they happen, and targets management accounting from the past to the future, therefore strengthening its strategic aspects.

Summing up the above, the following conclusion can be made. Given the product diversity and complexity of agricultural organizations, it is advisable to look at the internal control system for such organizations as an adaptive system integrated into all business processes. Introduction of an adaptive internal control system with a cybernetic component into the management accounting structure makes the process of monitoring the data flows within the accounting and analytical system automatic, which makes it self-sufficient and efficient.

Therefore, an adaptive system of internal control based on cybernetic communications will quickly eliminate shortcomings in the operation of agricultural organizations and prevent fraud or errors as well as increase the responsibility of internal controllers for their own performance, which will positively affect the quality of accounting and activities in the organization as a whole.

Azanova, N.N. (2013). Indices evaluation totality of economic resources of industrial enterprise. Discussion, 1(31), 44-52.

Alaverdova, T.P. (2014). Building internal control for an economic entity. Naukovedenie Internet Magazine, 6(25).

Belov, N.G. (2006). Control and audit in agriculture: textbook. Moscow: Finance and Statistics.

Boboshko, V.I. (2015). Control and audit: textbook. Moscow: Yuniti.

Butyrin, V.V. (2011). Technical aspects of finding economic costs of production of agricultural products. Accounting in Agriculture, 10, 40-42.

Burtsev, V.V. (2002). Internal controls: basic concepts and behavior. Management in Russia and Abroad. 4.

Diveeva, S.A. (2014) Issues of building an internal controls system in cooperative society. Young Scientist, 4.2, 92-96.

Drury, K. (2013). Management and cost accounting: kit for students of higher education. Moscow: Yuniti-Dana.

Drucker, P.F. (1964). Controls, control and management, in Management Controls: New Direcctions in Basic Research, McGraw-Hill.

Emmanuel, C., Otley, D. and Merchant, K. (1990). Accountion for Management Control, International Thomson Business Press.

Kakovkina, T.V. (2014). Audit control: theoretical and technical basics. Moscow: Yuniti.

Katkov, Yu.N. (2010). Building a cybernetic control system for the the purposes of management accounting. Vestnik BGU, 3, 198-202.

Khoruzhy, L.I. (2013). Management accounting in agriculture: textbook for students of higher agricultural education. Moscow: INFRA-M.

Melnik, M.V., Panteleev, A.S., Zvezdin, A.L. (2003). Audit and control: Textbook. Moscow: FVK-PRESS Publishing House.

Ostaev, G.Y., Kontsevaya, S.R., Kontsevoy, G.R., Alborov, A.A. (2015). Setting up and methods of internal cost control in agriculture. Accounting. Analysis. Audit, 3, 93-108.

Petrushenko, L.A. (1967). Feedback concept. Moscow: Thought.

Ryan, B. (1998). Strategic accounting for managers. Moscow: Audit, Yuniti.

Sheremet, A.D., Suiz, V.P. (2006). Audit. Moscow: INFRA-M.

Shapoval, E.V., Kostikova, A.M. (2018). Development of internal tax control as an element of the internal controls system. Economics, Management, Finance. 167-170

1. Department of Accounting, Russian State Agrarian University – MAA named after K.A. Timiryazev, Moscow, Russia. Contact e‑mail: 07@timacad.ru

2. Department of Management, Russian State Agrarian University – MAA named after K.A. Timiryazev, Moscow, Russia. Contact e‑mail: horuzhiy@list.ru

3. Department of Economic Security, Analysis and Audit, Russian State Agrarian University – MAA named after K.A. Timiryazev, Moscow, Russia. Contact e‑mail: kun95@yandex.ru

4. Department of Accounting, Russian State Agrarian University – MAA named after K.A. Timiryazev, Moscow, Russia. Contact e‑mail: Stepanenkoel5455@yandex.ru

5. Department of economic cybernetics, Russian State Agrarian University – MAA named after K.A. Timiryazev, Moscow, Russia. Contact e-mail: ration@mail.ru