![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 40 (Number 10) Year 2019. Page 15

LIMAREV, Pavel V. 1; LIMAREVA Yulia A. 2; SHKURKO, Natalja S. 3; SLOZHENIKINA N.S. 4; EREKLINTSEVA E.V. 5 & GAFUROVA, Vasilya M. 6

Received: 19/12/2018 • Approved: 03/03/2019 • Published 31/03/2019

6. Estimation of variable costs

ABSTRACT: Nowadays, information is one of the main products in all markets, from local to global ones. However, there is still no consistent theory that would take into account the specifics of the information product as a commodity and that satisfy all economists. Although information has been used as a commodity for quite a while and on a large scale, pricing for information products is carried out inconsistently, this means a considerable inconvenience to both producers and consumers. Therefore, pricing must necessarily consider the prime cost of information products, even when there is no profit from the sale of these products or it is not obvious. The goal of this research is to develop principles for calculating the prime cost of information distributed on publicly available media. |

RESUMEN: Hoy en día, la información es uno de los principales productos en todos los mercados, desde los locales hasta los globales. Sin embargo, todavía no existe una teoría coherente que tenga en cuenta los aspectos específicos del producto de información como un producto y que satisfaga a todos los economistas. Si bien la información se ha utilizado como un producto durante bastante tiempo y en gran escala, los precios de los productos de información se llevan a cabo de manera inconsistente, esto significa un inconveniente considerable tanto para los productores como para los consumidores. Por lo tanto, la fijación de precios debe considerar necesariamente el costo principal de los productos de información, incluso cuando no se obtiene ningún beneficio de la venta de estos productos. El objetivo de esta investigación es desarrollar principios para calcular el costo principal de la información distribuida en los medios disponibles públicamente. |

The information market is currently expanding, and the global turnover of information is huge. Information is the most popular product, representing a significant share in the operation of any company, no matter what field or industry it belongs to. Information products are part of the working capital used for a company’s tangible and intangible production, as well as the basis for the subsequent promotion and sale of the goods or services created. Information products play a crucial role in the company’s activities.

Having conducted research on this issue, the authors outlined the following problems: a company often purchases and sells information products in an inconsistent manner, since currently all companies rely almost solely on their own experience when paying for an information product. At present, there is no universal approach to estimating the prime cost of an information product. Having studied the publications on the research problem, the authors determined that the cost of information depends on many factors.

Information products as an object of market economy have been studied since the1970s-1980s. Due to certain specifics of the information product (relative alienability, dependence of price on the product’s relevance, etc.) it should be differentiated from other goods and services (Limarev & Limareva, 2018; Potrebin, 2015).

Information products are a particular type of a product, and the successful sale of information depends both on the market demand for it and the expenditures required for the production of an information product, i.e. from its prime cost. Information is different from other goods, and this requires a special approach to estimating its prime cost.

Principles of estimating prime cost were determined quite long ago. The labor theory of value (K. Marx) assumed that the prime cost of any commodity should be calculated as the value of labor invested in it (Marx, 1951). Modern methods of estimating prime cost were created by American Economists C. McConnell, S. Brue, and S. Flynn (2014), and later developed by many scientists, for instance, T. Johnson (1988), R. Kaplan (1988) and others. The principles they formulated are accurate, easy to use and are widely applied nowadays.

The prime cost of certain types of information products was estimated by C. Fink (1988), D. Orr (1987), S.P. Anderson, J. Waldfogel and D. Strömberg (2015), T. Bao, T. Chang (2016), B.А. Kuznetsov (2016) and other scientists.

However, these publications do not provide a complete picture of the principles for calculating the cost of an information product. Defining information as an independent resource, S. Jones claims that an information product is evaluated “intuitively”, that is the cost of information is calculated according to a manager’s experience (Jones, 2012). A. Andina-Díaz (2011) mentions the dependence of information products sold through mass media on the means of their production; however, she differentiates between active demand information and motivating information (advertising, passive demand information). She does not consider the fact that the production of a motivating information product actually costs the same as the production of active demand information. C. Crampes, C. Haritchabalet, B. Jullien (2005) share the same opinion.

S.M. Gurevich (2004) examines in detail the basic activities of a print media, describing the principles and technology of creating an information product and naming the sale of motivating information as the source of income. However, the researcher does not pay enough attention to estimating the costs of producing information.

Thus, despite the fact that the information market and information products have been researched for more than 30 years, the principles for estimating the prime cost of information products still require further study.

In this paper the authors applied the methods of analysis and synthesis which allowed determining the parameters of the object under study – the prime cost of the information product by cost elements, as well as studying the object of research in general. The method of analysis was used to divide the studied object into components – the prime cost of an information product into its constituent parts. This allows studying in detail all the cost elements characteristic of the information product. The method of synthesis was applied to combine cost elements into a single whole, highlighting within it the elements that occur due to the specifics of the object under study.

The methods used enable a systematic approach to investigating the complex research object which the prime cost of information products sold through publicly available media is.

In this article, publicly available media are defined as the ones the use, alienation or transfer of which are not limited by legislation or in any other way and which are available to everyone, while an information product uploaded on such media is intended for the categories of consumers with particular economic interests. Information products sold in this way can be classified into three categories: information products with a positive value, information products with zero value and information products with a negative value (Limarev, 2014). Apart from consumer’s perception, these types of information products differ from each other according to the ways they satisfy consumer preferences: the consumer pays for a transfer of a product with a positive value, a product with zero and negative value is transferred to the consumer at the expense of the producer [7].

To accurately assess the expenses of a company related to the production of information products, it is necessary to consider both the production and business processes of this company.

A company which is focused on creating information products has certain specifics. Its business processes differ both from the business processes of companies producing material values (tangible products) and from the business processes of companies producing services. However, all business processes of any company obey certain laws.

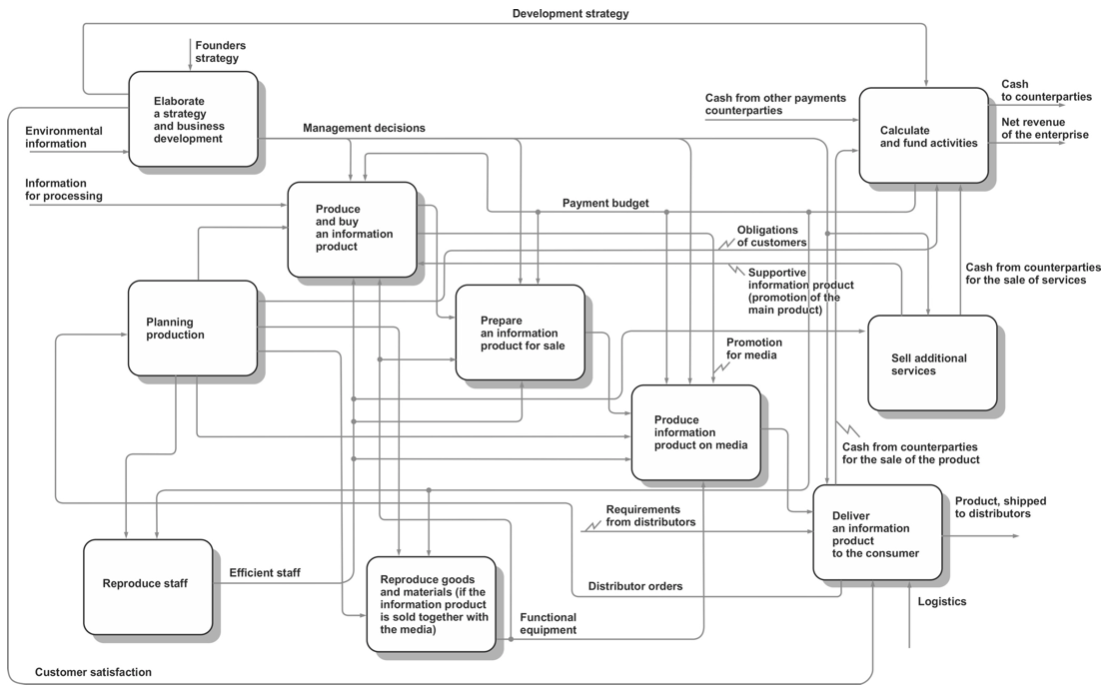

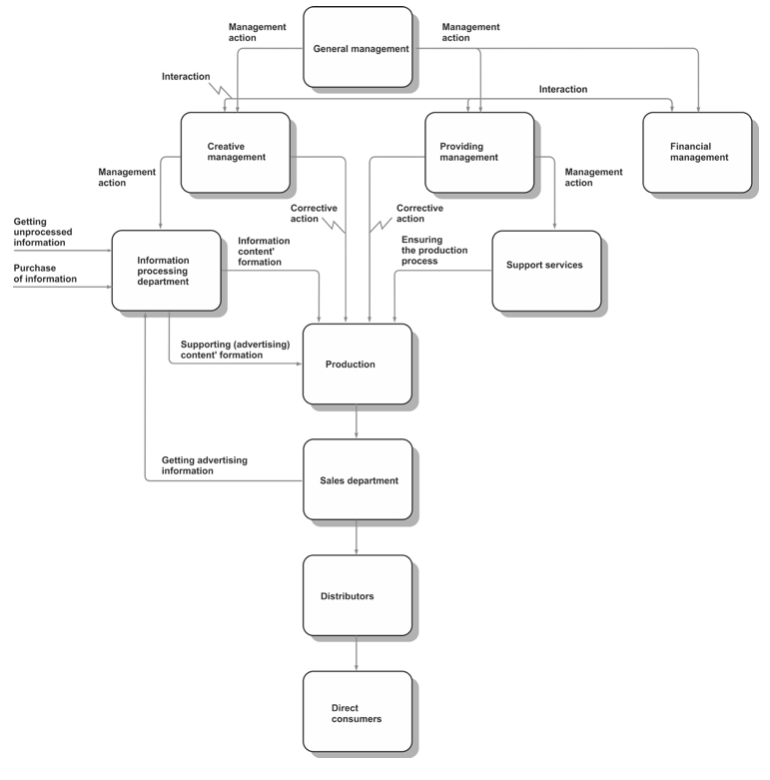

Figure 1 shows business processes characteristic of a company producing information products, while Figure 2 presents production processes. The company’s costs for the production of information products are estimated on the basis of these diagrams.

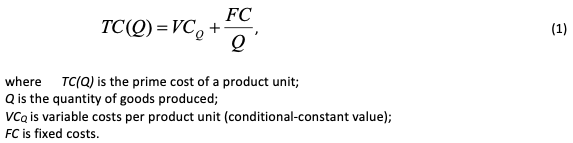

The prime cost of production includes two types of costs: variables that represent the direct costs of a company for producing each unit, and fixed costs reflecting the costs of a company that are not directly related to production and output (indirect costs). The main challenge for a company creating information products is estimating direct, i.e. variable costs – that share of it which is directly connected with the representation of knowledge recorded on the medium, in some cases – the creative component in the generation of the information product.

Figure 1

Business processes in a company creating information products

-----

Figure 2

Production processes in a company creating information products

The prime cost of any product unit, including intangible cost, as well as any service (work), is estimated as the sum of variable costs per product unit, and the share of fixed costs related to this unit (reduced costs). The prime cost of the product can be expressed by the formula:

When calculating prime cost, let us consider fixed costs as the costs of the production process, as well as sale and general running costs. In Figure 2 (production processes), these costs are marked as “Management” (creative and providing), support services (this component can have a fairly complex structure; however, in this research support services are considered only from the perspective of a resource consumer), and the sales department, including the service of interaction with distributors.

The cost of producing a supporting information product (advertising support for production) can be considered in two ways: 1) the cost of support for the brand should be regarded as fixed (indirect) costs, or, 2) the cost of promoting a specific information product should be seen as variable (direct) costs. Here one should note the following:

a) the cost of creating a supporting information product should be included in the variable cost of the production of the main information product; b) these expenses cannot be seen as directly dependent on the volume of the main information product generated, which is the case, for example, for the production of commodities and materials. Thus, to include a supporting information product in the variable cost of the main information product, one should apply a method that takes into account all these details.

In some cases, creation of a supporting information product can depend on the created volume of the main information product. This requires, firstly, a well-developed method of producing a supporting product, and secondly, the budget for its production should estimate the amount (a certain percentage) that will be fully spent. Thus, it will be possible to reduce the costs of supporting information product to direct costs.

In some cases, when using this method, production of the supporting information product cannot be regarded as direct costs, or sometimes this line of action is not reasonable. Then, the production of a supporting information product should be attributed to indirect costs, and they should be included in the cost of the main product as part of fixed costs and ranked in accordance with their share.

Thus, the volume of fixed costs as a whole can be expressed as follows:

Variable costs include all costs directly related to the creation of the main information product that vary in a monotonous dependence on the volume of the generated product and remain constant per product unit.

According to Figure 1 (business processes), these costs relate to the objects “Produce and buy an information product”, “Prepare an information product for sale,” “Produce an information product on media,” and “Deliver an information product to the consumer” (determined by the dependence of delivery costs of the information product to distributors on the volume of the generated product). These include: the cost of production or preparation of the media (if the information product is alienated with the media – print media, information on a CD, DVD, etc.), salaries of line personnel, and other expenses that vary linearly depending on the volume of the generated product.

The most challenging task in this case is the assessment of the creative component of variable costs. Since the volume and quality of an information product cannot be directly linked with the labor invested, the amount of labor cannot be used as a basic element of prime cost. To accurately estimate the share of creative work in the cost of an information product, one should use specifying coefficients that take into account a number of parameters (employee training level, overall work quality of an employee, employee’s status, etc.) and similar coefficients used in a pay scale. The creative management of the production company is responsible for choosing the coefficients when carrying out the estimation (Figure 2).

When determining the prime cost of a product unit, variable costs are a constant value [8] that include material costs and labor costs. Given the specifics of an information product, variable costs per unit of production are the following:

Functional staff is the employees who participate in the production of an information product, but are not in charge of generating the creative content (a proofreader, a layout designer, etc.). The cost of functional staff’s work does not depend on the number of employees or other features, so it can be estimated as a constant value connected with the production of an information product. Creative staff are the employees who prepare the content of a generated information product (authors, illustrators, camera men, etc.). If a creative group takes part in the creation of an information product, then it is possible to use the following specifying coefficients for each employee:

Thus, the cost of an information product can be estimated as follows:

The proposed method for calculating the prime cost of information products allows one to consider both the costs directly linked with the production and sales of products, and the costs related to the activities of the functional and creative groups, as well as to consider the qualitative characteristics of the information product arising due to the involvement of different creative professionals in making the product, their skills, work experience and talent.

The method proposed by the authors for estimating the cost of information products allows to take into account both the costs associated with the production and sale of products, the costs related to the work of the functional and creative groups, as well as the quality characteristics of the information product resulting from the involvement of creative staff with different levels of qualification, work experience and talent. This, in turn, enables businesses and companies to accurately estimate their production costs.

The presented method of estimating the prime cost of an information product distributed on publicly available media can be used to calculate the cost of any information on rewritable media with unlimited service life. In addition, the principles for calculating the prime cost of an information product formulated in this article can be used as to estimate the value of an information product created in different conditions.

Anderson S.P., Waldfogel J., Strömberg D. (eds.). (2015). Handbook of Media Economics. Vol. 1. URL: https://www.sciencedirect.com/handbook/handbook-of-media-economics.

Andina-Díaz A. (2011). Mass media in economics: Origins and subsequent contributions. Cuadernos de Ciencias Económicas y Empresariales, 61, 89-101.

Bao T.T. and Chang T.S. (2016). The Product and Timing Effects of eWOM in Viral Marketing. International Journal of Business, 21(2), 99-111.

Crampes C., Haritchabalet C., Jullien B. (2005). Advertising, Competition and Entry in Media Industries. CESifo Working Paper No. 1591. URL: http://www.cesifo-group.de/DocDL/cesifo1_wp1591.pdf.

Fink C.C. (1988). Strategic Newspaper Management. New York: Random House.

Gurevich S. (2004). Economy of Domestic Media. Moscow: Aspect Press.

Johnson T. (1988). Activity-based information: A blueprint for world class management accounting. Journal of Management Accounting, 23-30.

Jones S. (2012). Why ’Big Data’ is the fourth factor of production. Financial Times. URL: https://www.ft.com/content/5086d700-504a-11e2-9b66-00144feab49a.

Kaplan R. (1988). One cost system isn’t enough. Harvard Business Review, 66(1), 134–147.

Kuznetsov B. (2016). Economic and Organization in Publishing. Moscow: AST.

Limarev P. (2014). Estimation of the information product on the regional television information market. Marketing in Russia and Abroad, 6, 72-79.

Limarev P. and Limareva Yu. (2018). Characteristics of the market information used for illegal purposes. Scientific and Technical Information. Series 1. Organization and Methods of Information Work, 4, 13-15.

Marx K. (1951). Capital: A Critique of Political Economy. Vol. 1. Moscow: Gospolitizdat.

McConnell C.R., Brue S.L., Flynn S.M. (2014). Economics: Principles, Problems, & Policies. New York: McGraw-Hill.

Orr D. (1987). Notes on the mass media as an economic institution. Public Choice, 53(1), 79-95.

Potrebin A. (2015). Features of information as a commodity and the media consumption. Medialogic and web journalism. In: Journalism-2015 (pp. 446-448). Minsk.

1. Nosov Magnitogorsk State Technical University, Magnitogorsk, Russia. pavel.limarev.67@bk.ru

2. Nosov Magnitogorsk State Technical University, Magnitogorsk, Russia

3. North-Eastern Federal University named after M.K. Ammosov, Yakutsk, Russia

4. Nosov Magnitogorsk State Technical University, Magnitogorsk, Russia

5. Nosov Magnitogorsk State Technical University, Magnitogorsk, Russia

6. Nosov Magnitogorsk State Technical University, Magnitogorsk, Russia

7. Sometimes motivating information can be actively demanded: for instance, if the consumer is interested not in the content of the motivating information product, but the form. In this case, consumers are most often people working in the advertising industry who are looking for ideas for broadcasting motivating messages.

8. This statement does not take into account the change in variable costs that depend on the volume of production, or the so-called returns to scale.