![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 40 (Number 27) Year 2019. Page 25

SUNYOTO, Yonathan 1; LELY, Nur 2 & AGUS, Andi 3

Received: 23/04/2019 • Approved: 01/08/2019 • Published 05/08/2019

2. Literature Review and Hypothesis

ABSTRACT: This study wants to prove empirically the influence of motivation, experience, commitment and regulation of public accounting laws affecting auditor performance and job satisfaction with auditor knowledge as an intervening variable. By using purposive sampling with judgment sampling with the number of samples used as many as 355, the results of the study indicate that experience variables, and commitment can influence performance through knowledge variables. Performance has a positive and significant influence on job satisfaction. This shows that auditor knowledge variables function as mediators in the relationship between experience and auditor's commitment to performance. |

RESUMEN: Este estudio quiere demostrar empíricamente las influencias de la motivación, la experiencia, el compromiso y la regulación de las leyes de contabilidad pública El desempeño del auditor del conocimiento y la satisfacción laboral con el auditor es una variable interviniente. Al utilizar el muestreo intencional con el número de muestras utilizadas hasta 355, los resultados del estudio indican que las variables de experiencia y el compromiso influyen en el rendimiento a través de las variables de conocimiento. Desempeño positivo e influencia significativa en la satisfacción laboral. Esto muestra que las variables de conocimiento del auditor funcionan como mediadores en la relación entre la experiencia y el compromiso del auditor con el desempeño. |

Some corporate fraud and failures by multinational companies often involve large audit firms. One of the most important cases and marking reforms in auditing and accounting is the involvement of audit firm Arthur Andersen in Enron's in 2001 with financial statement manipulation, where financial conditions are reported to be substantially sustained by institutionalized, systematic and creatively planned accounting fraud. In addition, Deloitte and Touche was also involved in fraud in the case of Nortel of Canada (2003), which carried out inappropriate recommendations by distributing company bonuses to 43 top-level managers, and on Royal Ahold (Netherlands, 2003), where it did overstate the promotion reserve (Starkman, 2005), as well as in the case of Autonomy Corporation (2012), where itrecorded unprecedented sales of USD 3 million (Fisher, 2012). In addition, the firm Ernst and Young also did in the Anglo-Irish Bank case in Ireland (2008) by not making adequate disclosures regarding large loans, and in the case of Olympus Corporation of Japan (2011), by hiding losses (tobashi) in the form of acquisition costs. This has resulted in regulatory and public concerns and finally led to the strong desire of the regulators and stakeholders of the financial statements to limit creative accounting practices to overcome these problems, namely the regulation of public accounting laws (Lathif & Habibaty, 2019; Adjie, 2018). The impact of the auditor's poor performance on financial report fraud several times in this decade has made the auditor's profession in several countries change from independent industries to industries regulated by government regulations (Peecher et al. 2007). In Indonesia, government regulations applied to auditors working in the Public Accounting Firm are Law No. 5 of 2011. Act No. 5 of 2011 concerning public accountants, will have a positive impact in providing the existence of legal certainty for public accountant.

Libby and Luft (1990) reveals a model that influences knowledge and experience. An auditor's assessment will depend on their knowledge, because the information needed to perform tasks comes from memory. Experience also produces structure in the auditor's assessment process. These structures are the basis of decision making by interpreting the meaning and implications of specific information information (Gibbins, 1984). This is also supported by the Simon model of decision process in Abdolmohammadi and Shanteau (1992) which proves that experience significantly influences knowledge when an auditor must make considerations and control over the complexity of the task.

According to Paloniemi (2006), there are several important things to measure a person's work experience, such as the tenure of employment that has been held, the types of work that have been held, and the relevance of the work to their educational background. As is known work experience represents how broad and profound a person's understanding of his field of work. This can be built when there is a process of reducing past experience related to the field of work. The results of research conducted by Kvalsaughen (2009) show that there is relevance between educational background and work experience with managerial competencies owned by company managers.

In conjunction with performance, Owhoso and Weickgenannt (2009) on auditors in conducting audits found an increase in audit resource requirements and improvement in auditor quality which can be achieved by more intensive training and a more effective performance appraisal system. The experience of auditors who work in audit firms is very supportive in their work, because an auditor with high experience will tend to have a higher performance.

H1. The auditor's experience has a positive effect on auditor knowledge.

H2. The experience of auditors positively influences auditor performance

The commitment developed by Porter (1974) is defined as a relative strength of individual identification of an organization and its involvement in a particular organization, characterized by three psychological factors: (a) a strong desire to remain a member of a particular organization, (b) a desire to striving for the best of the organization, (c) confidence and acceptance of organizational values and goals.

High auditor commitment, so the effort to increase knowledge by training or education, especially in the field of audit is very necessary. The commitment study of professional accountants continues to develop affective professional commitment. Various dimensions of professional commitment have been found in other occupations and professions (Meyer 1993; Irving, 1997), it can be said that the focus is only on one dimension of professional commitment that is only providing a partial description of the accountant's professional commitment. This can also lead to incomplete understanding and the consequences of professional commitment, which may differ for each dimension (Meyer.1991; Irving. 1997).

Elias (2006) stated that professional commitment is a form of individual attachment to his profession. Furthermore, Pai, Yeh, & Huang (2012) wrote in his article that professional commitment is a mental dependence on the profession, beliefs and individual identification of various goals and values, where the individual is willing to offer hard work to his profession.

H3. The professional commitment of auditors has a positive effect on auditor knowledge.

H4. The professional commitment of auditors has a positive effect on auditor performance.

Motivation is an internal factor that can affect auditor performance. High motivation is more likely to produce quality work and quantity. The auditor in carrying out his work refers to the general audit standard which must have a special education criterion in accordance with his profession. Ashton (2011) conducted a study and found that motivation significantly affected auditor performance.

Previous comprehensive research into the effect of financial performance on incentives (Hertwig & Ortmann, 2001) has yielded three major conclusions about the relationship between financial incentives and performance. First, financial incentives can have both positive and negative effects on performance. Second, financial incentives are often found to have little or no performance (Camerer and Hogarth, 1999). Third, theoretically establish that individual and organizational variables can interact with incentives that determine performance. Auditors feel motivated in carrying out their duties as auditors, which in turn will be associated with greater organizational effectiveness, namely improving performance (Kohlberg, 1999).

H5. Auditor motivation has a positive effect on auditor performance.

Accounting regulations can also emphasize the importance of the role of the auditor in disclosure so that it can provide assurance for the performance of the auditor, protect financial report stakeholders and the auditor himself from financial report fraud and preventive efforts to prevent and reduce fraudulent financial statements (Hakim, 2017). Peecher et al. (2007) explained that the substantial focus of regulation in the last decade was to regulate how to reduce financial statement fraud and clarify the auditor's responsibility for financial report fraud. Further, the regulation is a reform of financial reporting weaknesses which explain that a reasonable guarantee is a high guarantee of material misstatement in financial statements due to fraud (Anis, 2013).

Watts and Zimmerman (1986) in their research found that accounting regulation was first applied in the United States (US) based on the Capital Market Act (Securities Act) 1933 and 1934 following the chaos of the country's capital market in 1929. The regulation was made by The Securities Exchange Committee (SEC) as US capital market authority is in the form of a minimum requirement for disclosure of financial reporting of companies listed on the stock exchange.

H6. Understanding of the Public Accountants Act has a positive effect on auditor performance.

Practice knowledge, focused on the function of knowledge, for example in problem solving and decision making. Conceptually, for example Clarke (1998) defines knowledge as "understanding why and how things work". Furthermore, the third one is philosophical, for example Wiig (1993) defines "knowledge consists of truth and belief, perspectives and concepts, assessment and expectations methodology, and know-how".

Ashton (2011) conducted a study and found that dispositional motivation significantly influenced the performance of auditors with knowledge as mediation. Detecting errors, an auditor must be supported with knowledge of what and how the error occurred (Tubbs, 1992). In general, an auditor must have knowledge about general auditing, functional areas, computer auditing, accounting issues, industry specifics, general world, knowledge, and problem-solving knowledge. Cloyd (1997) found that the amount of effort a person devotes to completing a job varies according to the level of knowledge possessed. Cloyd (1977) also found that a person's level of knowledge can improve performance.

H7. Knowledge positively influences auditor performance.

Kotter and Heskett (1977) mean that performance as a result of work produced by an employee in a certain time unit. Andrea (2007), Fakhimuddin (2018) found that two key aspects of a company's control system, namely performance feedback and reward systems, can have a significant impact on employees related to, task motivation, and performance. Likert's (1967) research suggests that satisfaction and positive attitudes can be achieved by maintaining a positive social organization environment such as by providing communication, positive autonomy and participation and mutual trust. Besides that, satisfaction obtained from performance can be explained by social exchanges, ie employees are given several gifts of social status will experience satisfaction and feel the obligation to provide remuneration (Organ, 1977).

Lawler and Porter (1967) found that performance can produce rewards, and this award is what causes satisfaction. Job satisfaction is a person's attitude towards his work that reflects a pleasant and unpleasant experience in his work and his hopes for future experiences. Based on the expectation theory perspective, Lawler and Porter (1967) stated that performance can produce rewards, and rewards that cause satisfaction.

H8. The auditor's performance has a positive effect on auditor job satisfaction.

Sampling in this study was using purposive sampling technique that this sample was selected using certain considerations (Ferdinand, 2011). The number of samples used in the study 355 emails to audit firms with respondents from public accountants, managers, senior supervisors and auditors, and junior auditors. The minimum sample size for SEM analysis is 100 to 200 (Hair et al., 2005).

Measurement of auditor motivation using instruments developed by Ganesan and Weitz (1996). Measurement of auditor experience using an instrument developed by Libby (1993). Measurement of the auditor's professional commitment using an instrument developed by Aranya et al (1981) and Ferris (1984). Performance measurement uses instruments developed by Kalbers and Forgarty (1995). Job satisfaction measurement uses the instrument The Minnesota Satisfaction Questionaires (MSQ) developed by Weiss et al (1967). Each respondent was asked to state their level of experience by answering a 7-point Likert scale question, starting with point 1 (Strongly Disagree), to 7 (Strongly Agree). Low scores indicate low auditor experience and vice versa.

The main method used for data analysis is Structural Equation Modeling (SEM). While data processing is done using the Analysis of Moment Structure (AMOS) version 21.0 application program.

The test results show that there is a correlational relationship between variable experience and motivation of 0.800. Statistical testing also showed a positive relationship between variable experience and commitment, and motivation and commitment respectively 0.349 and 0.334. In relation to understanding regulation, variable experience and motivation have a positive correlational relationship of 0.365 and 0.416, respectively. However, the commitment variable has a negative relationship with the understanding of regulation of -0.15.

Table 1

Correlations

Estimate |

|||

Motivation |

--> |

Experience |

.800 |

Experience |

--> |

Commitment |

.349 |

Commitment |

--> |

Regulation _ |

-.015 |

Experience |

--> |

Regulation _ |

.365 |

Motivation |

--> |

Regulation _ |

.416 |

Motivation |

--> |

Commitment |

.334 |

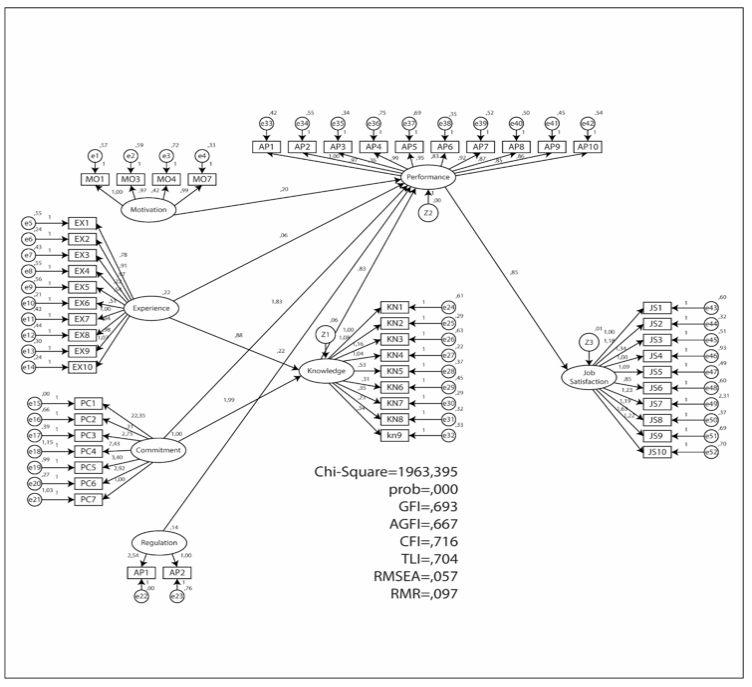

The selection of the estimation method for the research model is done by testing the match model by looking at some Goodness of Fit model criteria such as Chi Square value, probability, df, GFI, AGFI, TLI, CFI RMSEA and RMR. The following is the SEM model and the results of the model suitability test. Based on the estimation results of the structural model, the results of the model suitability test are as follows.

Table 2

Goodness of Fit Test Results

No |

Goodness of fit index |

Cut off value |

results |

1 |

Chi – Square |

small |

1963.395 |

2 |

Probability |

> 0.05 |

0.000 |

3 |

GFI |

> 0.9 |

0.693 |

4 |

AGFI |

> 0.9 |

0.667 |

5 |

CFI |

> 0.9 |

0.716 |

6 |

TLI |

> 0.9 |

0.704 |

7 |

RMSEA |

< 0.08 |

0.057 |

8 |

RMR |

< 0.5 |

0.097 |

Based on the table above, the model has fulfilled 1 criterion of goodness of fit (RMSEA <0.08), so the model can be assumed to meet the goodness of fit model criteria. Solimun (2002) states that if there are one or two goodness-of-fit criteria that have been fulfilled, then it can be said that the model built is good.

Convergent validity test and construct reliability are used to test the validity and reliability of loading factors (factor dimensions) with latent variables (constructs). Confirmatory factor analysis (CFA) is used to test the factor structure of variables. CFA is analyzed to test the relationship between variables and based on the constructs used as proxy variables (Suhr, 2006). Test results with detailed constructs used as variable proxies are shown in Table 3.

Table 3

Reliability and Construction AVE of Variables

Indicator |

λ |

λ2 |

1-λ2 |

CR |

AVE |

MO1 |

0.527 |

0.278 |

0.722 |

0.530 |

0.229 |

MO3 |

0.552 |

0.305 |

0.695 |

|

|

MO4 |

0.276 |

0.076 |

0.924 |

|

|

MO7 |

0.509 |

0.259 |

0.741 |

|

|

EX1 |

0.468 |

0.219 |

0.781 |

0.800 |

0.299 |

EX2 |

0.664 |

0.441 |

0.559 |

|

|

EX3 |

0.603 |

0.364 |

0.636 |

|

|

EX4 |

0.224 |

0.050 |

0.950 |

|

|

EX5 |

0.342 |

0.117 |

0.883 |

|

|

EX6 |

0.668 |

0.446 |

0.554 |

|

|

EX7 |

0.548 |

0.300 |

0.700 |

|

|

EX8 |

0.592 |

0.350 |

0.650 |

|

|

EX9 |

0.587 |

0.345 |

0.655 |

|

|

EX10 |

0.600 |

0.360 |

0.640 |

|

|

PC1 |

0.267 |

0.071 |

0.929 |

0.566 |

0.179 |

PC4 |

0.318 |

0.101 |

0.899 |

|

|

PC5 |

0.199 |

0.040 |

0.960 |

|

|

PC7 |

0.493 |

0.243 |

0.757 |

|

|

PC8 |

0.250 |

0.063 |

0.938 |

|

|

PC9 |

0.621 |

0.386 |

0.614 |

|

|

PC10 |

0.591 |

0.349 |

0.651 |

|

|

RG1 |

0.609 |

0.371 |

0.629 |

0.562 |

0.391 |

RG2 |

0.641 |

0.411 |

0.589 |

|

|

PR1 |

0.566 |

0.320 |

0.680 |

0.764 |

0.275 |

PR2 |

0.57 |

0.325 |

0.675 |

|

|

PR3 |

0.581 |

0.338 |

0.662 |

|

|

PR4 |

0.672 |

0.452 |

0.548 |

|

|

PR5 |

0.385 |

0.148 |

0.852 |

|

|

PR6 |

0.528 |

0.279 |

0.721 |

|

|

PR7 |

0.603 |

0.364 |

0.636 |

|

|

PR8 |

0.248 |

0.062 |

0.938 |

|

|

PR9 |

0.437 |

0.191 |

0.809 |

|

|

Note: MO= Motivation, EX= Experience, PC= professional commitment,

RG= Regulation Understanding, PR= Performance

After obtaining a fit model with the data and determining the appropriate estimation method for the model that has been formed, then the next SEM analysis phase is to estimate the structural model. The estimation results of the structural model can be seen in table 4.

Table 4

Results of Structural Model Estimates

Hypotheses |

Estimate |

S.E. |

C.R. |

P |

||

Knowledge |

<-- |

Knowledge |

.851 |

.162 |

5.302 |

*** |

Knowledge |

<-- |

Commitment |

.148 |

4.504 |

.443 |

.658 |

Performance |

<-- |

Knowledge |

.785 |

.161 |

3.914 |

*** |

Performance |

<-- |

Motivation |

.410 |

.073 |

4.092 |

*** |

Performance |

<-- |

Regulation |

.208 |

.073 |

2.945 |

.003 |

Performance |

<-- |

Knowledge |

.074 |

.124 |

.483 |

.629 |

Performance |

<-- |

Commitment |

.169 |

4.102 |

.446 |

.656 |

Job satisfaction |

<-- |

Performance |

.947 |

.159 |

5.361 |

*** |

Based on the test results, the estimation results obtained and the significant value of the influence of experience variables on knowledge is equal to 0.00 <0.05 with a positive loading factor of 0.851 indicating that the variable experience has a positive and significant effect on experience, the more experience a worker has, the higher his knowledge will be, and vice versa.

Second, the significant value of the commitment to knowledge variable influence is 0.658> 0.05 with a positive loading factor of 0.148 which indicates that commitment does not affect knowledge, a person's high commitment does not necessarily indicate high experience.

Third, the significant value of the influence of the motivation on performance variable is equal to 0.00<0.05 with a positive loading factor of 0.410 indicating that the Motivation variable has a positive and significant effect on the variable Performance. The higher the motivation of the worker, the higher the performance, and vice versa. Fourth, the significant value of the Experience variable on performance is 0.629> 0.05 and the loading factor value is 0.074 which indicates that experience has no effect on performance.

Fifth, the significant value of commitment to performance is 656 with a positive loading factor of 0.169 which indicates that commitment does not affect performance. Sixth, the significant value of the regulation understanding variable on performance is 0.003 with a positive loading factor of 0.208 which indicates that the regulation has a positive and significant impact on performance, the better the regulation, the better the performance of workers, vice versa.

Figure 1

Signifiant Values

Seventh, the significant value of knowledge to performance variable is equal to 0.00<0.05 with a positive loading factor of 0.785 which indicates that knowledge has a positive and significant effect on performance, the higher the knowledge of the worker, the higher the performance, and vice versa. Eighth, the significant value of the performance variable on job satisfaction is 0.00<0.05 with a positive loading factor of 0.947 which indicates that performance has a positive and significant effect on job satisfaction, the better the worker's performance, the higher his job satisfaction, and vice versa.

Analysis of the influence of determination is used to determine the contribution of exogenous variables to endogenous variables can be seen from the adjusted R square. The coefficient of determination (R2) essentially measures how far the model's ability to explain endogenous variation (Ghozali 2008). Adjusted R2 has been adjusted to the degrees of freedom of each square covered in the calculation of adjusted R2. The coefficient of determination can be seen in the Squared Multiple Correlations in table 5.

Table 5

Determination Coefficient

Endogen Constructs |

Estimate |

Knowledge |

.745 |

Performance |

.801 |

Job satisfaction |

.897 |

The coefficient of determination of the Knowledge variable is 0.745, in this study knowledge variables are influenced by experience and commitment variables, this indicates that the influence of the variable commitment and experience on knowledge is 74.5% while the remaining 25.5% is influenced by other factors outside experience and commitment. Furthermore, the coefficient of determination of the performance variable is 0.801. In this study, the performance variable is influenced by the motivation, experience, commitment and regulation of the law variables that show that the influence of motivation, experience, commitment and regulation of the UU on the performance is 80.1% while the remaining 19.9% is influenced by other factors in beyond the motivation, experience, commitment and regulation of the UU. The coefficient of determination of the variable job satisfaction is equal to 0.897, in this study the variable job satisfaction is influenced by performance which means that the influence of performance on job satisfaction is 89.7% while the remaining 10.3% is influenced by other factors outside the performance variable.

In this study, there are direct and indirect pathways that connect exogenous variables of experience and commitment to performance variables. The following is a test of the direct and indirect effects of exogenous variables on experience and commitment to the performance variable through knowledge variable.

Table 6

Direct and Indirect

Influence Test Results

Exogenous variable |

Intervening Variables |

Direct Influence |

Indirect Influence |

Conclusion |

Experience |

Knowledge |

0,169ns |

0.851 X 0.785 = 0.668 ** |

Indirect Influence through knowledge |

Commitment |

Knowledge |

0,074ns |

0.148 X 0.785 = 0.116** |

Indirect Influence through knowledge |

Based on the results of the test, it was obtained the results that the experience variables did not significantly influence the performance variables. However, experience variables can influence performance through knowledge variables, this shows that actual experience variables can affect performance variables mediated by knowledge variables. The experience of workers can improve their performance if followed by an increase in knowledge of workers. Commitment variables have no significant effect on performance variables, but commitment variables can influence performance through knowledge variables. This shows that the commitment variable can actually affect the performance variables mediated by knowledge variables. The experience of employees is able to improve their performance if followed by an increase in employee knowledge.

Table 7

Evaluation of Hypothesis Testing

through Mediating Analysis

Dependent Variables |

Direction |

Independen Variables |

Evaluation of Direct Effect |

Evaluation of Indirect Effect |

Knowledge |

<-- |

Knowledge |

accepted |

accepted |

Knowledge |

<-- |

Commitment |

rejected |

rejected |

Performance |

<-- |

Knowledge |

accepted |

accepted |

Performance |

<-- |

Motivation |

accepted |

accepted |

Performance |

<-- |

Regulation_ |

accepted |

accepted |

Performance |

<-- |

Knowledge |

rejected |

accepted with mediation |

Performance |

<-- |

Commitment |

rejected |

accepted with mediation |

Job satisfaction |

<-- |

Performance |

accepted |

accepted |

Empirical test results show that the experience variable does not significantly influence the performance variable. However, experience variables can influence performance through knowledge variables. This shows that the actual experience variables can influence the performance variables mediated by knowledge variables. The experience of workers can improve their performance if followed by an increase in knowledge of workers. In the context of intermediation relationships, commitment variables can influence performance through knowledge variables. This shows that the commitment variable can actually affect the performance variables mediated by knowledge variables. The experience of workers is able to improve their performance if followed by an increase in knowledge of workers. Based on the findings of this study, improving auditor knowledge is influenced by auditor motivation, auditor experience and auditor professional commitment. Judging from the size of the estimation that is the most important in improving auditor knowledge is experience. Here, it should be noted in the formation of the auditor's experience is understanding the auditor as a profession. Furthermore, auditor performance in this study is influenced by auditor motivation, auditor experience and auditor professional commitment and regulation of public accountant law. Based on data analysis to improve auditor performance that needs to be considered is auditor knowledge, in improving auditor performance, because the higher the auditor's knowledge the better the performance. Improving auditor performance in turn tends to increase auditor job satisfaction. The auditor in improving its performance is through coordination and supervision in completing the work. This will increase the auditor's job satisfaction related to getting support from the supervisor.

Abdolmohammadi, M. J., & Shanteau, J. (1992). Personal attributes of expert auditors. Organizational Behavior and human decision processes, 53, 158-158. 999Aranya, N., Pollock, J., & Amernic, J. (1981). An examination of professional commitment in public accounting. Accounting, Organizations and Society, 6(4), 271-280.

Adjie, H. (2018). Joint Responsibilities of Internal Shareholders against Credit Agreements on Limited Company Bankruptcy: Considering Provisions of Law of Llc. Journal of Legal, Ethical and Regulatory Issues, 21(SI).

Anis, M. (2013). Pengungkapan Keuangan Perkara Secara Memadai Dalam Laporan Keuangan Satuan Kerja Peradilan. Jurnal Hukum dan Peradilan, 2(2), 277-290.

Ashton, R. H. (1990). Pressure and performance in accounting decision settings: Paradoxical effects of incentives, feedback, and justification. Journal of Accounting Research, 148-180.

Bedard.J & Machelene., 1992. Experience Current Directions in Psychological Science. Vol.1.pp.135-139.

Camerer, C. F., & Hogarth, R. M. (1999). The effects of financial incentives in experiments: A review and capital-labor-production framework. Journal of risk and uncertainty, 19(1-3), 7-42.

Cloyd, C. B. (1997). Performance in tax research tasks: The joint effects of knowledge and accountability. Accounting Review, 111-131.

Drake, A. R., Wong, J., & Salter, S. B. (2007). Empowerment, motivation, and performance: Examining the impact of feedback and incentives on nonmanagement employees. Behavioral research in accounting, 19(1), 71-89.

Elias, R. Z. (2006). The impact of professional commitment and anticipatory socialization on accounting students’ ethical orientation. Journal of Business Ethics, 68(1), 83-90.

Fakhimuddin, M. (2018). Reconsidering Accounting Information Systems: Effective Formulations for Company's Internal Control. Arthatama Journal of Business Management and Accounting, 2(1)

Ferris, K. R. (1981). Organizational commitment and performance in a professional accounting firm. Accounting, Organizations and Society, 6(4), 317-325.

Ganesan, S., & Weitz, B. A. (1996). The impact of staffing policies on retail buyer job attitudes and behaviors. Journal of retailing, 72(1), 31-56.

Gibbins, M. (1984). Propositions about the psychology of professional judgment in public accounting. Journal of Accounting Research, 103-125.

Hakim, F. (2017). The Influence of non-performing loan and loan to deposit ratio on the level of conventional bank health in Indonesia. Arthatama: Journal of Business Management and Accounting, 1(1).

Hertwig, R., & Ortmann, A. (2001). Experimental practices in economics: A methodological challenge for psychologists?. Behavioral and Brain Sciences, 24(3), 383-403.

Irving, P. G., Coleman, D. F., & Cooper, C. L. (1997). Further assessments of a three-component model of occupational commitment: Generalizability and differences across occupations. Journal of applied psychology, 82(3), 444-452.

Kadous, K., Leiby, J., & Peecher, M. E. (2013). How do auditors weight informal contrary advice? The joint influence of advisor social bond and advice justifiability. The Accounting Review, 88(6), 2061-2087.

Kalbers, L. P., & Fogarty, T. J. (1995). Professionalism and its consequences: A study of internal auditors. Auditing, 14(1), 64-86. 999Ketchand, A. A., & Strawser, J. R. (1998). The existence of multiple measures of organizational commitment and experience-related differences in a public accounting setting. Behavioral Research in Accounting, 10, 109.

Kohlberg, L. (1969). Stage and sequence: The cognitive-developmental approach to socialization. Rand McNally, In Handbook Of Socialization Theory and Research. Chicago: Rand McNally.

Kotter, J. P. (2008). Corporate culture and performance. New York: Simon and Schuster.

Kvålshaugen, R. (2001). The Antecedents of Management Competence: The Role of Educational Background and Type of Work Experience.Series of Dissertation, web-bi-noforskning 255 C.. 999Lawler III, E. E., & Porter, L. W. (1967). Antecedent attitudes of effective managerial performance. Organizational behavior and human performance, 2(2), 122-142.

Lathif, A. A., & Habibaty, D. M. (2019). The suitability of sharia life insurance policy for POJK no. 69/POJK. 05/2016 and POJK no. 72/POJK. 05/2016. Jurnal Hukum dan Peradilan, 8(1), 63-83.

Libby, R., & Luft, J. (1993). Determinants of judgment performance in accounting settings: Ability, knowledge, motivation, and environment. Accounting, organizations and society, 18(5), 425-450.

Likert, R. (1967). The Human Organisation. New York: McGraw-Hill. Meyer, J. P., & Allen, N. J. (1991). A three-component conceptualization of organizational commitment. Human resource management review, 1(1), 61-89.

Organ, D. W. (1977). A reappraisal and reinterpretation of the satisfaction-causes-performance hypothesis. Academy of management Review, 2(1), 46-53.

Owhoso, V., & Weickgenannt, A. (2009). Auditors’ self-perceived abilities in conducting domain audits. Critical Perspectives on Accounting, 20(1), 3-21.

Pai, F. Y., Yeh, T. M., & Huang, K. I. (2012). Professional Commitment of Information Technology Employees under Depression Environments. International Journal of Electronic Business Management, 10(1), 17-28.

Paloniemi, S. (2006). Experience, competence and workplace learning. Journal of workplace learning, 18(7/8), 439-450. 999Peecher, M. E. (1996). The influence of auditors' justification processes on their decisions: A cognitive model and experimental evidence. Journal of Accounting Research, 125-140.

Porter, L. W., Steers, R. M., Mowday, R. T., & Boulian, P. V. (1974). Organizational commitment, job satisfaction, and turnover among psychiatric technicians. Journal of applied psychology, 59(5), 603.

Siders, M. A., George, G., & Dharwadkar, R. (2001). The relationship of internal and external commitment foci to objective job performance measures. Academy of Management Journal, 44(3), 570-579.

Starkman, D. (2005). AIG comes clean on accounting. Washington Post, Nov. 26, 2005.

Susilo, D.E. (2018). The Effects of Corporate Social Responsibility on Corporate Value. Arthatama Journal of Business Management and Accounting, 2(1).

Tubbs, R. M. (1992). The effect of experience on the auditor's organization and amount of knowledge. Accounting Review, 783-801.

Watts, R., & Zimmerman, J. (1986). Positive accounting theory. Prentice-Hall. Englewood Cliffs. NJ.

Weiss, D. J. , Dawis, R. V. England, G. W. and Lofquist, L. H. (1967), Manual for the Minnesota Satisfaction Questionnaire. Vol. 22, Minnesota Studies in Vocational Rehabilitation. Minneapolis: University of Minnesota, Industrial Relations Center.

Wiig, K. (1994). The central management focus for intelligent-acting organizations. Arlington: Schema Press. 999.

1. Sekolah Tinggi Maritim Dan Transpor (STIMART) AMNI, Indonesia. Email: ysunyoto.stieaka.smg@gmail.com

2. Bandung Islamic University, Bandung, Indonesia

3. College of Economics of Makassar Bongaya (STIEM Bongaya), Indonesia