![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 40 (Number 32) Year 2019. Page 2

KHAMZINA, Dilya R. 1; GOLOVIZNIN, Sergey M. 2; NOGOVITSINA, Olesya V. 3; SARAPULOVA Anna V. 4; ARISHINA Elina S. 5 & AYGUMOV Timur G. 6

Received: 05/04/2019 • Approved: 12/09/2019 • Published 23/09/2019

ABSTRACT: Key elements of the accounting and analytical support system for calculations with counterparties: accounting, economic analysis and internal control are examined in the paper. We formed model of interaction based on the stages of information processing, which allows us to consider all elements in unity. The definition of accounting and analytical support is clarified, the features of the information hierarchy approach are considered through responsibility centers of the enterprise. |

RESUMEN: Los elementos clave del sistema de apoyo contable y analítico para acuerdos con contrapartes: contabilidad, análisis económico y control interno se examinan en el documento. Modelamos su interacción en función de las etapas del procesamiento de la información. Se aclara el concepto de soporte contable y analítico, y se consideran las características del enfoque de proceso para la implementación de procedimientos contables y analíticos. |

Commercial enterprises have diverse types of calculations in modern business conditions. While functioning in unstable macroeconomic conditions organizations face the problems developing of appropriate accounting and analytical support calculations with counterparties, which allow to ensure compliance with contractual and settlement discipline, fulfill obligations to supply products in a given assortment and quality, reduce the amount of receivables and payables, therefore, improve the financial condition of the company. Thus our research has scientific interest and practical significance.

The concept of calculations arose in economics for a long time. The concept of calculations traditionally is interpreted as "making a payment for something." V.A. Chernov [2] defines calculations as an "extended order of human cooperation" fueled by the development of the market and trade system, progress and mutual influence of the exchange and distribution system. Bukhantsev [1] under the term calculation considers the disposal of funds to another person, or the receipt of funds from another person accompanied by economic connection between the producer and the consumer. In general in economics the term "calculations with counterparties" is understood as making payments with suppliers and customers.

The field of calculations with counterparties is one of the key for the organization due to effects on financial condition. The analysis of the literature allowed us to identify the following problems negatively affecting the buyer ability to reduce expenses and declare deductions:

- bad faith of the supplier in terms of tax payments;

- incorrect documentation filling which should confirm the execution of the contract by the parties;

- incorrect interpretation of the legislation or legal terms when signing the contract.

Basic tools aimed on to deal with problems of inter-firm cooperation are: factoring [6], insurance mechanisms [5], differentiation of counterparties [3]. There are different approaches to define accounting and analytical support in economic literature (table 1).

Table 1

Definitions of «accounting and analytical support»

Author |

Definition |

M. A Vakhrushina [10] |

Collection, processing and transfer of financial and non-financial information used by managers to plan and monitor the activities of their departments, measurement and evaluation of the results. |

M I Kutter [4] |

Interrelation of operational, accounting (financial and managerial) and statistical accounting due to the general accounting methodology in the entire economy of the state, as well as indicators of forecasting, accounting and reporting. |

H A Sokolova [9] |

The information system arising from the basis of the organizational structure of management - the hierarchy of functions or the combination of business processes. |

Source: own processing

In our opinion, accounting and analytical support of calculations with counterparties represents a holistic information system aimed at harmonizing accounting procedures, economic analysis and internal control for making management decisions. However, given the significance of the proposed “fragmented” measures within the theoretical background there is no integral model based on the stages of information processing by accounting, economic analysis and control subsystems, what predetermined the purpose of this article.

Among the methodological foundations of Studying the accounting and analytical support of calculations with counterparties we can highlight traditional book-keeping assumptions:

double-entry recording; principles of continuity of enterprise; principle on liability; temporary certainty of economic activity.

Furthermore, we have used next accounting practices:

Calculations with counterparties in the financial management are essential parts of accounting (Savitskaya, 2010, Sheremet, Saifulin, Negashev, 2000). Results of interaction are receivables and payables, which are the constituent elements of working capital. Working capital, in turn, is a factor determining financial stability and the level of firm competitiveness.

Organization of calculations with counterparties is an integral management area of a successfully developing enterprise and includes following interrelated elements: analysis of the economic feasibility transactions; evaluation of legal aspects; documentation of transactions and their recording in accounting; internal regulations for calculations with counterparties.

The most important element of the settlement organization system is documentary support of transactions and their recording in accounting. The implementation of this function is the primary fact-fixing of the economic life of the organization and the subsequent recording in the registers and financial statements. Traditionally, the document flow with suppliers and customers is as follows: agreement for the sale, documents for the delivery of goods and materials, registers, accounting statements. The most popular accounting errors: the absence of appropriate payment documents, bookkeeping errors in the completing of payment documents, absence of list concluded contracts with counterparties, divergences in reconciliation reports, lack of original documents. To manage calculations with counterparties the managers are advised to set up a monthly schedule of expected payments for auditing receivables and payables. An example of this schedule for debts is presented in Table 2.

Table 2

Calculation schedule for customers

Customer |

Advance payment |

Progress payment |

Final payment |

|||

Plan/fact |

Plan/fact |

Plan/fact |

Plan/fact |

Plan/fact |

Plan/fact |

|

X1 |

Date/ amount |

Date/ amount |

Date/ amount |

Date/ amount |

Date/ amount |

Date/ amount |

…. |

Date/ amount |

Date/ amount |

Date/ amount |

Date/ amount |

Date/ amount |

Date/ amount |

Source: own processing

Acts of reconciliation should be requested monthly from the largest suppliers, with smaller suppliers it is possible to conduct reconciliation once a quarter.

Analysis of receivables and payables requires data which could be obtained from an analytical accounting and balance sheet. The purpose is to identify the amounts of justified and unjustified debt, changes for the analyzed period, the reality of the amounts of receivables and payables, the causes and prescription of receivables. In general we can determine next tasks of analysis: assessment of the size, dynamics and structure of receivables and payables; analysis of the ratio receivables and payables; study of the age structure debts; determining the quality and turnover of accounts receivable; forecasting the optimal amount of receivables and payables; development basic provisions of the settlement policy and justification conditions for granting a commercial loan to individual buyers.

Examination of receivables begins with a study of the structure, status and dynamics of receivables in absolute amount and in relative magnitude as well. Specialists study the personal composition of debtors, the timing of debt, the reasons, amounts, measures taken to recover the debt using data of the analytical accounting (journals, warrants, analytical cards for settlement accounts, contracts, commercial correspondence). At the same time, it is necessary to differ permissible and unacceptable debts.

At present internal control of settlements with counterparties is usually ensured by distributing functions between departments of organizations, allocating persons responsible for verifying compliance with the terms of contracts and for bookkeeping.

Internal control procedures are aimed at identifying errors and reducing company risks, the main ones are: purchases from an unreliable supplier and (or) at an inflated price;

unauthorized purchases, payment of non-existent obligations; accounting of suppliers' accounts while deliveries were not actually made; emergence of uncollectible receivables as a result of the decision to work with an insolvent buyer; transactions with an insolvent buyer; material misstatement of the financial statements if a provision for doubtful debts is not created correctly (Kobeleva, Konova, 2015; Peshchanskaya,2011; Samoilova, Magomedova, 2016).

From our point of view the internal audit department capable to perform the functions of control over the preparation of objective financial information, assess the effectiveness of the internal control system, identify and manage risks because internal auditors able to make a significant amount of control functions assigned to the management of the organization. Internal audit departments are used in the vast majority of countries and confirm their effectiveness in practice. Despite the similarity of performed functions, internal audit and revision are completely different forms of internal control. The main goal and the actual content of the revision are narrower than the functions of internal audit, including monitoring the compliance of the organization's financial and business activities with the legislation requirements.

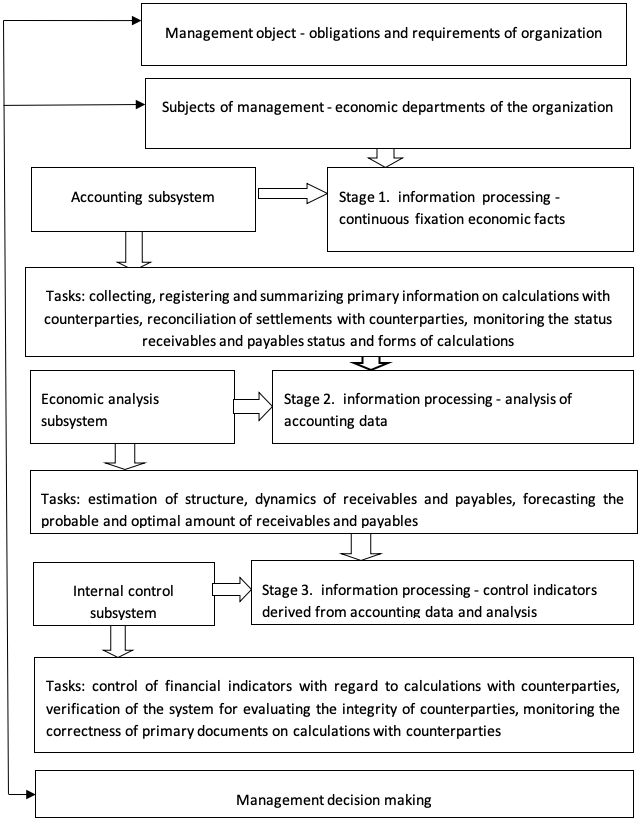

All the above-mentioned parts of accounting and analytical support system (accounting, economic analysis and internal control) are interconnected through the management function. We elaborate the model of accounting and analytical support system, based on information processing stages (figure 1).

Figure 1

Model of accounting and analytical support system

Source: own processing

From the other side the system of accounting and analytical support of calculations can be represented as a multifactorial model of interaction between the firm departments during the implementation of business processes. It should be noted that the organizational structure of this model is most significantly influenced by three factors:

- hierarchy of information formation (organization as a whole, its structural divisions, responsibility centers);

- current regulatory framework within accounting and taxation and industry characteristics as well;

- information needs of internal and external users.

Consequently, the model of the accounting and analytical system for providing calculations with counterparties should has individual nature, depending on the specifics of the activity.

Let us consider benchmark example model of accounting and analytical support, based on information hierarchy (table 3).

Table 3

Example of accounting and analytical support model

Stage |

Responsibility center |

Aim / Result |

Procedures |

1.Planning

|

Departments in charge both for supplies of resources and sale of the produce |

Aim: identifying potential suppliers and consumers Result: assessment of the need for transaction |

Analysis the financial condition based on the data of the accounting financial statements |

2. Work with agreements |

Departments in charge for contracting |

Aim: contracting Result: formation legal basis for calculations system with counterparties |

Determination the timing delivery goods and payment procedures. |

3. Delivery of inventory |

Departments in charge for delivery of inventory |

Aim: compliance with the terms of contract Result: timeliness of supply/sales |

Timely accurate reflection in the primary documents |

4.Accounting

|

Departments in charge for bookkeeping

|

Aim: reflection facts of economic life in the accounting system. Result: grouping the facts of economic life in the accounts |

Reflection information about the occurrence of receivables and payables, its availability |

5. Financial |

Departments in charge for calculation and payment operations |

Aim: payment of debts Result: completion of the payment operations |

monitoring of the schedule for payment |

6. Internal control and audit

|

Departments in charge for internal controls |

Aim: evaluation of misstatements identified during payment operations Result: ensuring the reliability of financial information |

Verification of the completeness posting and registration facts concerning payments, accuracy of documents. |

Source: own processing

Literature analysis showed that issues of accounting and analytical support in respect to calculations with counterparties are considered through research its main pillars: accounting, economical analyses and internal control. But an integral approach is needed due to low efficiency management decisions aimed on improvement certain aspects of calculations with counterparts. Unlike the existing approaches this article clarifies the concept of accounting and analytical support, which is characterized by the interconnectedness of three functional subsystems: accounting, analytical and control, united by common managerial focus. We developed a model of accounting and analytical support, revealing three successive stages of information processing from continuous registration facts of calculations with counterparties to monitoring indicators obtained from accounting data and analysis. Its implementation in the management system will reduce the risks caused by contractual policy and its execution.

Bukhantsev Yu.A. (2009) Calculations and liabilities as objects of accounting. Bulletin of Volgograd State University, 2(15):222-226.

Chernov V.A., 2013. Accounting,Third edition. Moscow

Kobeleva S.V., Konova O. Yu. (2015) Receivables: the emergence, analysis and management. Science Territory, 2:109 - 115.

Kutter M.I., Taranets N.F. Ulanova I.N., 2016. Accounting (financial) statements, Second edition. Moscow

Peshchanskaya I. V. (2011) Insurance mechanisms in the management of accounts receivable of enterprises. News of the Russian Economic University G.V. Plekhanov: electronic scientific journal, 5:50-55.

Samoilova L.B., Magomedova R. M. (2016) Factoring in the management of receivables. Transport and Service, 4: 133-143.

Savitskaya G.V., 2010. Analysis of the economic activity of the enterprise. Second edition. Moscow

Sheremet A.D, Saifulin R.S, Negashev E.V, 2000. Methodology of financial analysis, Third edition. Moscow

Sokolova H.A.,2015. Management Analysis, Third edition. Moscow

Vakhrushina M. A., 2007. Management accounting, Second edition. Moscow

1. Nosov Magnitogorsk State Technical University, Russia, Chelyabinsk Region, Magnitogorsk, bel-mgtu@yandex.ru

2. Nosov Magnitogorsk State Technical University, Russia, Chelyabinsk Region, Magnitogorsk

3. Nosov Magnitogorsk State Technical University, Russia, Chelyabinsk Region, Magnitogorsk

4. Nosov Magnitogorsk State Technical University, Russia, Chelyabinsk Region, Magnitogorsk

5. Nosov Magnitogorsk State Technical University, Russia, Chelyabinsk Region, Magnitogorsk

6. FSBEI HE «Dagestan State Technical University» (FSBEI HE «DSTU»), Russia, Republic of Dagestan, Makhachkala