![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 40 (Issue 42) Year 2019. Page 27

PAVLENKOV, Michael N. 1 & REIMOV, Rinat Zh. 2

Received: 22/08/2019 • Approved: 02/12/2019 • Published 09/12/2019

3. Development and testing of forecasting models

ABSTRACT: This manuscript is about the development of a forecasting method for the product sales of an industrial enterprise based on the study of the theory of regression analysis. The authors present an approach to the development of product sales models; they also propose the main stages of development and methods for assessing their adequacy and accuracy. Additionally, the authors executed retrospective data and forecasted sales volume of products. This procedure was executed using the forecasting method proposed in current work. The authors developed recommendations to reduce prices, which allowed for increasing sales and product profitability. |

RESUMEN: Este manuscrito trata sobre el desarrollo de un método de pronóstico para la venta de productos de una empresa industrial basado en el estudio de la teoría del análisis de regresión. Los autores presentan un enfoque para el desarrollo de modelos de venta de productos. También proponen las principales etapas de desarrollo y métodos para evaluar su adecuación y precisión. Además, los autores ejecutaron datos retrospectivos y pronosticaron el volumen de ventas de productos. Este procedimiento se ejecutó utilizando el método de pronóstico propuesto en el trabajo actual. Los autores desarrollaron recomendaciones para reducir los precios, lo que permitió aumentar las ventas y la rentabilidad del producto. |

At the present stage, the activities of enterprises are complicated, as, with market competition, there remain enterprises whose products are sold. Therefore, the effective organization of marketing activity becomes an essential factor in the production process of selling an enterprise's products.

Realization in economic theory is investigated as a circuit of capital, which, when it moves, passes through the sphere of circulation twice: purchase of a resource for production and for customer satisfaction, as well as for further production. Products for sale have a value form and a real one. Implementation means that the consumer acquires the factors of production intending to develop production. Competition complicates the system of sales of enterprise products, which requires an analysis of the market, its demand structure, and improvement of sales processes.

Functionally, sales activities are associated with the organization and creation of distribution channels, the sale of finished products of the enterprise (Sannikov, A. (2004); Suma, T. (2003)).

The effective functioning of the sales system is based on the long-term strategy of the enterprise.

Effective sales system requires the following (Chernyakovskaya, T. (2008)):

- Investigate and find out both the advantages and disadvantages of their products with competitors' products;

- Study the sales market, the dynamics of market capacity and sales volume;

- Analyze the competition in the market and identify the factors of competitiveness.

In this regard, the most essential tasks of enterprises are the tasks of increasing competitiveness and compliance of product quality with the demands of the domestic and foreign markets.

All this requires improvement of the management mechanism aimed at improving the efficiency of using the capabilities of the enterprise and adapting sales activities to changes in the external environment.

The sale of products for an industrial enterprise requires various organizational-technical and financial-economic processes, which ensure the solution of the problems of supply and sale are aimed at meeting the demand and achieving the enterprise's strategic and tactical goals.

Sales are the result of production and economic activity of the enterprise (Khan, D. (1997). Sales plays the following roles of usefulness:

- Estimating resulting development of production and profit;

- Creation of efficient sales scheme, which increases chances of competition;

- Providing feedback on the finalization of products;

- Identifying and studying consumer preferences.

The effectiveness of the sales system depends on the strategy of the enterprise, which describes the mechanism for achieving goals (Bezpalov et al., 2019; Batkovskiy et al., 2018). Chemical industry enterprises more often use an advantage strategy, a pricing strategy, or a combination of these (Milner B. (2010), Sannikov,А. (1994).

Strategic sales objectives usually derive from an enterprise strategy:

- Maximum use of sales opportunities;

- Expanding range and increasing sales;

- Reduction of income turnover;

- Enhancing economic and financial sustainability;

- Meeting demand for consumer products.

Sales volume affects the financial condition of the company. Therefore, forecasting sales volume is essential for the company's success.

It can be stated that the need to introduce new forecasting methods is increasing, which contributes to making marketing activities more sustainable and strengthening the competitive market position of the enterprise (Brinza et al., 2015; Novikova et al., 2016; Golovina, 2013).

Many domestic and foreign economists have devoted their work to the study of managing an industrial enterprise's sale of products. These economists are G. J. Bolt (1991), I.A. Blank (1998), L.A. Bragin (2003), I.T. Balabanov (2001), W. Witt (1996), V.P. Gruzinov (1997), F. Kotler (2009), R. Kaplan (2004), Yu. Matsuro (2009), B.Z. Milner (2010), A.A. Sannikov (1994), E.A. Utkin (1999), D. Khan (1997), P.M. Khorvat (2000), and T.N. Chernyakhovskaya (2008).

However, until now, forecasting an enterprise's sales activities regarding the chemical complex requires further study, and given that volume is the basis for the formation of a sales plan, more research is required in regard to the conduct of commercial and production operations, the formation of current production plans, and the determination of the company's revenues.

The variability of the external environment significantly increases uncertainty in the process of product sales planning and, as a result, increases the risks in realizing the company's goals. Therefore, product sales plans should be consistent with the overall strategy of the company (Azoev, 2006; Weber and Knorren, 1999; Drucker, 2002; Kozlov and Uvarov, 2000; Omelchenko, 2005; Pavlenkov, 2005; Khan, 1997; Khorev et al., 2003; Chernyshev, 2009).

Statistical methods allow for research indicators, such as: comparing and determining relationships, observing current trends and important patterns, conducting quantitative analyses of indicators and choosing the most effective solution, and evaluating the consequences of decisions made without using complex and expensive experiments. (Orlov, 2011; Omelchenko, 2005; Orlov, 2011; Pavlenkov and Kulikov, 2004; Trifonov et al., 2012).

The efficiency of operation and long-term presence in the market depends largely on the accuracy of the forecast sales volume. In other words, forecasting allows the enterprise to clarify goals and develop plans for the near future (Aniskin and Pavlova, 2005; Weber and Scheffer, 2000; Omelchenko, 2005; Suma, 2003; Khan, 1997; Chernyshev, 2009; Gorfinkel, 1998; Golovina & Golovin, 2013; Akhmetshin et al., 2018).

Forecasting the volume of sales of industrial enterprises can be viewed as the initial stage of budget planning, as an ideology that provides completely new opportunities for more informed decisions in the field of sales management and enterprise economics. Forecasting allows for building a more systematic relationship between the various departments of the enterprise in the process of organizing the development, adoption, and implementation of management decisions in the commercial and industrial sectors of the enterprise (Weber and Knorren, 1999; Pavlenkov, 2005; Khan, 1997; Chernyakhovskaya, 2008).

Forecasts of product sales are the most essential tool of enterprise management, allowing the formation of prices, production volume, and financial indicators (Bolt, 1991; Matsuro, 2009).

Based on the forecast plan and contracts, the current (annual) plan is developed, which contains in-kind as well as cost indicators for the product range or types, consumers and sales directions for the planned period with the breakdown by quarter and month.

The implementation plan is formed, taking into account year-end balances of unsold products in terms of value.

The supply plan for suppliers is an obligation to ship finished products of corresponding quality, of the agreed volume in physical and monetary terms for each product named within the terms established by the contract.

The shipment volume is the planned quantity of products that the company must ship to the consumer directly or using a system of intermediaries.

In the process of developing a sales plan, the volume of resources is determined, as well as their leading suppliers. This allows specialists to ensure that the enterprise will be provided with sufficient material resources for the planned period.

At the final stage, transportation schemes are developed and product shipment schedules and product delivery plans to various customers are created.

A forecasting method for product sales is shown in Figure 1.

Module 1. The information necessary for forecasting sales should be contained in the information database of the company. If such information is not in the database, then to perform calculations, it is necessary to organize the process of collecting and processing data.

In this module, a time series for each type of product is formed in the information base based on retrospective data.

Figure 1. Forecasting method for the products sales volume.

Module 2. The main problem solved at this stage is the analysis of the time series and the definition of objective patterns of product sales. Random fluctuations of the series are smoothed out, and the primary trend of the series, as well as the development law, is determined. The time series is evaluated to determine the type of development, and possible seasonal variations are investigated (Aiwazyan, 2001; Orlov, 2011; Pavlenkov, 2006; Trifonov et al., 2012).

For the study of anomalous indicators of a series, the well-known Irwin criterion is used (Aiwazyan, S. (2001), Orlov, А. (2011)).

Smoothing the series is necessary in order to smooth out random oscillations of the series, as well as to reveal the main one. Various methods are used for smoothing:

- Simple moving average method (arithmetic average);

- Time average method;

- Exponential smoothing method.

Row analysis and trend research are applied:

- T-criterion, which allows for determining the presence of trends and the mathematical form of the trend of the time series (Orlov, А. (2011);

- The Wallis and Moore criterion, which is a non-parametric method for studying time series trends (Aiwazyan, S. (2001);

- The Foster-Steward method, which is used to identify trends in the time series, both in variances and in the average (Orlov, А. (2011).

To identify the type of development of the time series, one can use the methods of analytical alignment and moving average, as well as the Cox-Steward criterion (Aiwazyan, S. (2001).

Time series must be investigated for seasonal fluctuations, and the well-known Chetverikov method is suitable for this purpose (Orlov, А. (2011). This method allows for identifying the presence of the seasonal component of the time series.

Thus, an assessment is performed and the type of development of the time series under study is determined, and seasonal variations are identified in this module.

Module 3. According to the time-series data for forecasting, functions reflecting the main trends are determined. Such functions can be, for example, linear, exponential functions, polynomials, logical curves, and many other functions. The possibility of using a particular function for forecasting is determined after assessing its adequacy.

Module 4. In order to be able to use the model for forecasting, it is necessary to establish its adequacy.

The quality of the approximation is estimated by the confidence value R2 of the model approximation (Aiwazyan, S. (2001). Its value may lie in the range from 0 to 1. The closer is to 1, the more accurately the model describes the data of the time series.

To estimate the significance of the model, the Fisher criterion F (Aiwazyan, S. (2001) is used. At a given significance level, the hypothesis of the trend model is accepted.

A time series model is considered adequate if the residual component satisfies many properties (Aiwazyan, S. (2001), Pavlenkov,M. (2006) :

- The randomness of fluctuations of residual sequence levels;

- Random component corresponds to the distribution according to the ordinary law (the asymmetry index (A) and the kurtosis index (E) are used);

- Equality to zero of the expectation (using Student's criterion);

- Independence of the random component (using the Durbin-Watson criterion).

A trend model is considered adequate if the model satisfies all the considered properties.

Module 5. The accuracy of the model is characterized by the deviation of the model values of the levels from the actual values.

The following are used as statistical indicators (criteria) of accuracy:

- “Standard deviation” criterion;

- “Average relative error of approximation” criterion;

- “Convergence coefficient” criterion;

- “Determination coefficient” criterion.

In this module, using the accuracy assessment criteria, decisions are made on the accuracy of the developed trend model, which is used to forecast the product sales.

Module 6. The point value is determined by substituting time into the trend equation. For practical purposes, the limits of variation of the forecasted indicator are determined, since the actual data may not coincide with the point forecast. This can be caused by the following:

- An error when choosing the type of model;

- Error when estimating the model parameters;

- Error caused by the deviation of some observations from the trend.

The significance level, the forecast period, the degree of the polynomial, and the standard deviation from the trend can affect the magnitude of the variation limit of the confidence interval.

This stage determines the point value of the forecast and the boundaries of the interval in which the actual value of the forecasted sales volume of products is expected.

Module 7. Forecasting of sales volume is performed for each type of production n (n = 1,2,...N). As a result of forecasting, the forecasted sales volume of products is determined using the developed trend model.

Module 8. When calculating sales volumes in value terms, it is necessary to proceed from the pricing policy of the enterprise, and the following factors influencing the pricing policy should be considered:

- Market elasticity of demand;

- The reaction of competitors;

- Product quality;

-Product life cycle;

- The image of the company.

The pricing policy is that the company makes a specific decision on the prices of its products.

In practice, some enterprises develop and implement perhaps several policies simultaneously for different product groups.

For the calculation of sales in terms of value at the stage of forecasting, prices can be taken:

- Based on the expert reviews;

- Based on forecasting;

- Base year;

- Current year;

- Based on benchmarking.

A generalized estimate of the forecast sales is indicators of profit and profitability.

The pricing policy of an enterprise reflects the financial relations with consumers that are directly related to the prices of their finished products and financial relationships with suppliers that are directly related to the prices of products received from suppliers (Kotler, F. (2009), Matsuro, Y. (2009). This is explained by the fact that in order to increase competitiveness, it is necessary to substantiate the pricing policy for manufactured products, and as a result, develop pricing policies with suppliers of the necessary resources. At the same time, the company strives to minimize costs by reducing unit costs of resources for finished products (Azoev, 2006; Drucker, 2002; Pavlenkov, 2007; Gorfinkel, 1998).

In this module, the calculation of profit and profitability of the projected sales volume of products, which are analyzed by the relevant services of the enterprise, is performed. Based on this analysis, measures are being developed to refine the indicators.

Module 9. As a result of the assessment and analysis of indicators, proposals are developed to refine the indicators, which are agreed with the various services of the enterprise.

Target sales are the basis for the formation of organizational and economic activities. If the goals cannot be achieved, then new activities need to be developed.

The system of the food complex analyses previously taken measures on design, quality, and brands of products to identify the necessary changes in the structure and assortment of the company's product program.

The system of price planning in the existing conditions of the contract policy analyses and develops the measures on:

- Specifying the size of discounts for various types of products;

- Clarifying the terms of sales of various types of products;

- Clarifying the terms of sales of products for various markets;

- Clarifying the credit conditions for sales of products for some consumers;

- Expanding product distribution channels;

- Stimulating sales of products.

The quality assessment of the developed measures is the results of the implementation of plans and the achievement of goals.

Developed targets and measures are coordinated with financial services. The decisions to change them are the basis for the adjustment of sales volumes. The coordination cycle ends with coordination with all the services of the enterprise, which is the basis for the formation of the production plan for the enterprise.

The company produces four types of products that make up more than 90% of sales. Let us analyze the retrospective data on the sales volume for 2013-2017 and form a time series for each type of product (see Table 1).

Adequate models were investigated and identified (linear and exponential).

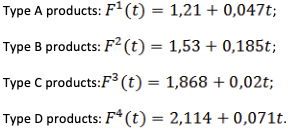

For each product type, the following linear models were obtained:

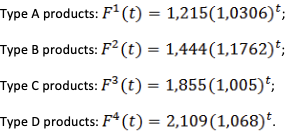

Similar calculations were performed using the exponential equation. For each product type, the following exponential models were obtained:

Table 1 shows the actual data and data obtained from trend models to compare the obtained forecast results. To determine the volume of production for 2018, substitute t instead of 3, and for 2019 t = 4 (the base year 2015). Using the accuracy criteria for assessing the adequacy of the models, we determine that linear models provide more accurate results for all types of products, so they are adopted to forecast sales.

Table 1

Actual data and sales forecasts.

year |

t |

Actual data |

Linear model |

Exponential model |

|||||||||

A |

B |

C |

D |

A |

B |

C |

D |

A |

B |

C |

D |

||

2013 |

-2 |

1.12 |

1.15 |

1.84 |

2.01 |

1.116 |

1.16 |

1.828 |

1.972 |

1.144 |

1.044 |

1.837 |

1.850 |

2014 |

-1 |

1.23 |

1.28 |

1.91 |

2.12 |

1.163 |

1.345 |

1.848 |

2.043 |

1.179 |

1.228 |

1.846 |

1.975 |

2015 |

0 |

1.14 |

1.63 |

1.75 |

1.94 |

1.21 |

1.53 |

1.868 |

2.114 |

1.215 |

1.444 |

1.855 |

2.109 |

2016 |

1 |

1.26 |

1.75 |

1.83 |

2.15 |

1.257 |

1.715 |

1.888 |

1.185 |

1.252 |

1.698 |

1.864 |

2.252 |

2017 |

2 |

1.34 |

1.84 |

1.95 |

2.35 |

1.304 |

1.9 |

1.908 |

2.256 |

1.290 |

1.998 |

1.874 |

2.406 |

2018 |

3 |

1.35 |

1.85 |

1.96 |

2.36 |

1.351 |

2.085 |

1.928 |

2.327 |

1.330 |

2.350 |

1.883 |

2.569 |

2019 |

4 |

1.398 |

2.27 |

1.948 |

2.398 |

1.371 |

3.096 |

1.892 |

2.744 |

||||

Note: data in line 2018 correspond to the planned values

The forecast values of the sales volume for each type of products allow for determining the volume in terms of value for 2019, as well as profit (Table 2), and Table 3 shows the calculation of profitability.

Table 2

Cost indicators of sales volume (2019)

No. of products |

Volume (ths. t.) |

Price (ths. RUB) |

Volume (mln. RUB) |

Expenditures for item. (ths. RUB) |

Expenditures mln. RUB |

Profit mln. RUB |

1. А- |

1.398 |

165.0 |

230.67 |

138.0 |

198.924 |

37.746 |

2. B |

2.27 |

176.0 |

399.52 |

152.0 |

345.04 |

54.480 |

3. С |

1.948 |

125.0 |

243.50 |

102.0 |

198.696 |

44.804 |

4. D |

2.398 |

155.0 |

371.690 |

128.0 |

306.944 |

64.746 |

Total: |

1245.38 |

1043.604 |

201.776 |

|||

-----

Table 3

Return on sales volume

No. of products |

Volume (mln RUB) |

Profit (mln RUB) |

Return |

Return of the current year |

1. А |

230.67 |

37.746 |

0.1636 (16.36%) |

16.45% |

2. B |

399.52 |

54.480 |

0.1364 (13.64%) |

15.15% |

3. С |

243.50 |

44.804 |

0,184(18,4%) |

19.41% |

4. D |

371.690 |

64.746 |

0.1742 (17.42%) |

18.3% |

As can be seen from Table 3, the profitability for all types of products, except for products of type A, is lower than the profitability of the current year. Therefore, it is necessary to analyze prices and costs. Price change entails a change in sales.

The performed calculation of the forecasted sales volume and their analysis allowed the company's specialists to develop in time recommendations for making adjustments to the planned indicators. Thus, based on the recommendations, the price for products of type A was reduced by 6.2%, which made it possible to increase sales (concluded contracts for 2019) by 1.175 million rubles, and increase profitability by 0.34% compared with 2018. These results were obtained at the operating enterprise.

The authors proposed the method of forecasting and analyzing the sales volume of industrial enterprise products based on the use of trend analysis. Forecasting sales volume of products is the basis for all commercial and industrial operations, and the formation of production plans, the formation of the financial results of the company.

Using real statistical data of an industrial enterprise, trend forecasting models have been developed for the main types of products. The sales volume forecast for 2019 was made based on the linear models. Analysis of the forecast figures for sales volume for 2019 made it possible to develop recommendations for lowering prices for products, which led to an increase in sales of products by 6.2% and profitability by 0.34% compared with the plan proposed for 2019.

Aiwazyan, S. (2001). Basics of econometrics. Moscow: YUNITI-DANA.

Akhmetshin, E.M., Vasilev, V.L., Mironov, D.S., Zatsarinnaya, Е.I., Romanova, M.V., Yumashev, A.V. (2018). Internal control system in enterprise management: Analysis and interaction matrices. European Research Studies Journal, 21(2), 728-740.

Aniskin, Y., & Pavlova, A. (2005). Planning and controlling: Textbook on “Organization’s Management” discipline. 2nd ed. Moscow: Omega-L.

Azoev, G. (2006). Competition: analysis, strategy, and practice. Moscow: Center of Economics and marketing.

Balabanov, I. (2001). Innovative management. Saint Petersburg: Piter.

Batkovskiy, A.M., Efimova, N.S., Kalachanov, V.D., Semenova, E.G., Fomina, A.V., Balashov, V.M. (2018). Evaluation of the efficiency of industrial management in high-technology industries. Entrepreneurship and Sustainability Issues, 6(2), 577-590.

Bezpalov, V.V., Fedyunin, D.V., Solopova, N.A., Avtonomova, S.A., Lochan, S.A. (2019). A model for managing the innovation-driven development of a regional industrial complex. Entrepreneurship and Sustainability Issues, 6(4), 1884-1896.

Blank, I. (1998). Trade management. Kyiv: Ukrainian-Finnish Institute of management and business.

Bolt, G. (1991). Practical Sales Management: textbook. Moscow: YUNITY.

Bragin, L. (2003). Organization of commercial activities. Moscow: Akademiya.

Brinza, V.V., Ilyichev, I.P., Ugarova, O.A., Loginova, V.V. (2015). Prognostic simulation of external economic activity for an industrial company. CIS Iron and Steel Review, 10, 27-39.

Chernyakovskaya, T. (2008). Marketing activities of the enterprise: theory and practice. Moscow: Higher education.

Chernyshev, M. (2009). Strategic management. Fundamentals of Strategic Management. Moscow: Phoenix.

Drucker, P. (2002). Practice of management. Moscow: Publishing house “Williams”.

Golovina, T. (2013). Concept Application «Management Future» for Forecasting of Financial Results Industrial Enterprises. Journal of Contemporary Economics Issues, 1. https://doi.org/10.24194/11304

Golovina, T., & Golovin, R. (2013). Organization of System of Administrative Strategic Control of Expenses for Production and Realization of Production of the Industrial Enterprise. Journal of Contemporary Economics Issues, 2. https://doi.org/10.24194/21304

Gorfinkel, V. (1998). Enterprise Economics. Moscow: Banks and Stock Exchanges, YUNITI.

Gruzinov, V., & Gribov, V. (1997). Enterprise Economics: Tutorial. Moscow: Finance and Statistics.

Kaplan, R., & Norton, D. (2004). Strategy-Oriented Organization. Moscow: Olympus Business.

Khan, D. (1997). Planning and control: the concept of controlling. Moscow: Finance and Statistics.

Khorev, A., Zhuravlev, Y., & Balabanova, L. (2003). The economic stability of enterprises based on the introduction of the controlling system. Theory, and practice of crisis management: Collection of articles of the International Scientific and Practical Conference, (pp. 83-85). Penza.

Khorvat, P. (2000). Balanced scorecard as a means of enterprise management. Problems of theory and practice of management, 4, 108-113.

Kotler, F. (2009). Marketing in the third millennium: How to create, conquer, and keep the market. Moscow: AST Publishing House.

Kozlov, V., & Uvarov, S. (2000). The commercial reality of the enterprise: strategy, organization, management: studies. Textbook. Moscow: Polytechnic.

Matsuro, Y. (2009). Sales promotion. Marketing, advertising, and sales, 1, 56.

Milner, B. (2010). Innovative development. Economy, intellectual resources, knowledge management. Moscow: Infra.

Novikova, N.V., Barmuta, K.A., Kaderova, V.A., Il’Yaschenko, D.P., Abdulov, R.E., Aleksakhin, A.V. (2016). Planning of new products technological mastering and its influence on economic indicators of companies. International Journal of Economics and Financial Issues, 6(8Special Issue), 65-70.

Omelchenko, I. (2005). Methodology, methods, and models of the management system of organizational and economic sustainability of high-tech production of integrated structures. Moscow: Publishing House of Bauman Moscow State Technical University.

Orlov, A. (2002). Econometric support of controlling. Controlling, 1, 42-53.

Orlov, A. (2011). Organizational-economic modeling: decision-making theory: a textbook. Moscow: KNORUS.

Pavlenkov, M. (2005). Development of technology management solutions: monograph. Nizhny Novgorod: Publishing House of the Volga-Vyatka Academy of State Services.

Pavlenkov, M. (2006). Development of methodological support for controlling an industrial enterprise: monograph. Nizhny Novgorod: Publishing House of the Volga-Vyatka Academy of State Services.

Pavlenkov, M. (2007). Controlling of an industrial enterprise: methodology, theory, practice: monograph. Nizhny Nobgorod: Publishing House of the Volga-Vyatka Academy of State Services.

Pavlenkov, M., & Kulikov, A. (2004). Methods, and models of management decision making in economic systems. Nizhny Novgorod: Publishing House of the Volga-Vyatka Academy of State Service.

Sannikov, A. (2004). Effective sales management. Moscow: Progress.

Suma, T. (2003). Economics of Enterprise: studies, allowance. Minsk: New edition.

Trifonov, Y., Lapaev, D., & Ruzanov, A. (2012). Economic and mathematical methods for making optimal decisions: Textbook. Nizhny Novgorod: Publishing house of Nizhny Novgorod State University.

Utkin, E., & Myrynyuk, I. (1999). Controlling: Russian practice. Moscow: Finance and Statistics.

Weber, Y., & Knorren, N. (1999). Ensuring rationality through planning, focused on increasing the value of the enterprise. Problems of the theory and practice of management, 3, 74-79.

Weber, Y., & Scheffer, W. (2000). On the way to active management with the help of indicators. Problems of theory and practice of management, 5, 107-111.

Witt, W. (1996). Sales management. Moscow: INFRA-M.

1. Doctor of Sciences (Economics), Professor of Lobachevsky State University of Nizhni Novgorod. Contact e-mail: michael.pavlenkov@yandex.ru

2. Post-graduate student of Lobachevsky State University of Nizhni Novgorod.