![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 41 (Issue 08) Year 2020. Page 16

KHARITONOVICH, Alexander V. 1

Received: 09/09/2019 • Approved: 12/12/2019 • Published 12/03/2020

ABSTRACT: The paper classifies the factors of investment and construction complex management for territorial development. The research method is classification. Results: the investment and construction complex functioning factors with seven interrelated groups are classified (international, country-specific, regional, subdivision, investment and construction complex factors, certain participant and personal employee factors). Conclusion: the most frequent approaches regarding investment and construction complex are discrete and discrete-continuous; in comparison, the continuous approach to a greater extent reflects the complexity of the management process, without analyzing the sequence of management stages. |

RESUMEN: El artículo analiza de los factores que deben tenerse en cuenta en el proceso de la gestión del complejo de inversión y construcción para asegurar el desarrollo de los territorios. El método del estudio es la clasificación. Resultados: se propone la clasificación de los factores de funcionamiento del complejo de inversión y construcción, según la cual estos factores se examinan en siete grupos interrelacionados (internacionales; del país determinado; regionales; factores del complejo de inversión y construcción; factores del participante determinado; factores de la unidad dentro del participante del complejo de inversión y construcción en cuestión; factores personales del empleado). |

The functioning of investment and construction complexes (ICCs) has a significant impact on the social and economic situation both within individual cities and regions and in the whole country, since the construction sector is the most important component of the national economy and is one of the sources of the economic growth of the state that largely determines the success of the implementation of various social and economic objectives of the development of a particular territory.

It is necessary to continuously improve the ICC management system to perform its crucial tasks. Meanwhile, the issue of forming a unified concept of improving the ICC performance remains open, and the problems of evaluation (Thomson & El-Haram, 2019), analysis and forecast of ICC development receive insufficient attention.

In the uncertainty conditions of the external environment, at a high level of complexity, dynamism, and mobility (Zaguskin, 2015, p. 5; Häkkinen & Belloni, 2011; Mohd-Rahim, Mohd-Yusoff, Chen, Zainon, Yusoff & Deraman, 2016), the ICC acts as a field of economic activity associated with the expanded reproduction of the main production and non-production funds (Vakhmistrov, 2004, p. 5) and is a complex systemic formation. The link between lack of flexibility and organizational management has the greatest impact on the failure of construction projects; cooperation difficulties are also among important impact factors (Chen, Merrett, Lu & Mortis, 2019).

Drawing attention to the ICC complexity, Khrustalev, Gorbunov and Musatova consider it to be a complex multilevel system including interrelated economic subsystems characterized by self-sustainability and independence. Since such independent functioning of the mentioned subsystems affects the ICC as a whole, it is necessary to have external regulatory actions which will contribute to the achievement of results of ICC activity taking into account the minimization of resource and time losses (Khrustalev, Gorbunov & Musatova, 2015, p. 8).

The complexity of the ICC as a management entity also becomes very apparent when considering it as an organizational system with a large number of participants and with a certain structure, goals, functions, and needs that must be combined to achieve key objectives in the economic reproductive cycle.

Within a specific territory, the ICC can be considered as a set of industries, sectors, and organizations that have stable economic, organizational, technical and technological ties in order to create fixed assets within the territorial boundaries.

Voronin offers a classification of factors affecting the ICC, which includes (Voronin, 2007, p. 28):

• state factors affecting the regional ICC (social environment, economic conditions, political environment);

• regional factors, the essence of which is revealed in the conditions of ICC functioning in a specific territory, characterized by natural factors, management features, and regional policy);

• location factors that are determined by the territorial mobility of construction;

• intra-system environmental factors (management systems, labor market).

Berkovich and Golubkina pay attention to three levels of factors (Berkovich & Golubkina, 2010, p. 25): environmental factors, territorial factors, and internal environment factors (industry factors).

According to researchers, the negative impact of environmental factors contributes to the formation of regional problems. The mentioned regional problems are considered as territorial factors, under the influence of which internal (industry) factors are formed. The latter may also have a negative impact on the ICC activities.

External environment factors include economic, social, environmental, political, international, as well as institutional, technological, and technical factors.

The internal (industry) factors that affect ICC activities are represented by three groups (Berkovich & Golubkina, 2010, p. 26):

• specific characteristics of construction products;

• specifics of the construction production;

• organizational and economic specifics of construction.

ICC functioning can be considered in the light of an even greater number of levels and factors. The mentioned levels include the company level, ICC level, ICC subject level, subdivision level, as well as the employee level (Lyulin, 2015, p. 237).

ICC management is the impact of the managing subsystem, i.e. the management subject, on the managed, i.e. the management object, and there is a direct connection between the management subject and the management object (Semenova & Dzhambaev, 2010, p. 15). ICC managers are required to "manage project risks, develop project policies and procedures" (Subramanyam & Haridharan, 2017). Effective ICC management requires an understanding of the process content, which can be disclosed through an examination of the relevant management functions.

Firstly, object management requires consideration of various aspects of its functioning, which contributes to the emergence of diverse approaches to the classification of management functions. Secondly, the authors use concepts that are similar in meaning but use different terms to refer to them. There are also situations where researchers use the same term to refer to different concepts, which eventually leads to terminological confusion. Thirdly, the content of the management function in question is not always clear and precise. In addition, some authors consider management functions in an integrated manner, while others consider them in more detail. In view of the above circumstances, in the author's opinion, the significance of classification of management functions is beyond doubt.

As to various composition options of management functions, which are presented in the Russian works, first of all, it is necessary to notice that this structure is presented as per GOST 24525.0-80 "Management of an industrial association and industrial enterprise. Basic provisions" (1983). In accordance with the standard, the following general functions are considered to be typical elements of the management cycle: forecasting and planning (Gluch, Gustafsson, Baumann & Lindahl, 2018); organization of work; coordination and regulation (Guner & Benli, 2019); activation and stimulation; monitoring, accounting, and analysis. In addition to the functions listed, some of them can be grouped based on a number of features. For example, these include human resources (Abuazoom, Hanafi & Bin Ahmad, 2019), procurement and financial management (Qian, Chan & Khalid, 2015; Ali, Zhu & Hussain, 2018).

Prediction of these functions is of particular interest, as its interpretation is characterized by some features. To denote this function, Fayol used the French word "prévoyance", which is translated as foresight, providence. In the English edition, both the word "foresight" and the word "planning" are used to denote the same function. However, in the English edition of the work, the word "planning" is used in the subsection title devoted to the first management function (Fayol, 1949, p. 43). Probably, this situation arose because, in fact, the first function involves both forecasting and planning. However, Fayol focused on forecasting and the English edition shifted this focus to some extent towards planning.

On the contrary, according to Mintzberg, a world-renowned scientist, the description of the management work proposed by Fayol has lost its relevance and the functions mentioned above do not really reflect the essence of management activity and represent a kind of "folklore" (Mintzberg, 1975). At best, they only allow identifying some of the vague objectives that managers are guided by in their work. In addition, Mintzberg calls to abandon this perception of management functions and to perceive them more true-to-life.

Among the approaches to ICC management, there are those that focus on broad management categories, rather than on the details of specific methods. Approaches that distinguish the main (general) or basic management functions, as well as linking functions (Rokhchin, Zhilkin & Znamenskaya, 2010, p. 147) and binding processes, are selected. The performance of linking functions provides the realization of the basic functions. Besides, the author considers it necessary to include a number of specific functions (GOST 24525.0-80, 1983, p. 8), which reflect the most significant spheres of its functioning, in the classification of ICC management functions.

The author supports the opinion of the researchers, who consider the function of target formation as the first main management function (Timms, 1962, p. 80). If this function is not considered to be one of the main functions (Addis, 2016), but, for example, is included in planning or forecasting, such an approach to some extent deflects attention from the true management content, instead offering a rough abstraction that is difficult to use in practice (Timms, 1962, p. 21). It is hardly possible to carry out forecasting, planning at an adequate level if there are no objectives formulated at least in the first approximation. Resources are often limited and must be used with specific targets that can be adjusted in the process.

The main goal of the ICC development is the creation of completed construction objects that act as the infrastructure for the organization of the population's life processes in the whole variety of its components (Asaul, Asaul, Alekseev & Lobanov, 2009, p. 63).

Since the effectiveness of the ICC management largely depends on understanding the influence of various factors on its functioning, the issue of its internal as well as external management is presented in more detail in Table 1.

Table 1

ICC objectives

ICC environment

ICC scope |

Internal environment |

External environment |

Investment sector |

Making investments within the internal ICC environment to maintain it in a given state, improving its elements. |

Making investments to create a product (service) for the entities of the external ICC environment. |

Production sector |

Manufacture of products, rendering of services to ensure the creation of the end ICC product. |

Production of products, provision of services for the external ICC environment entities. |

Labor sector |

Ensuring the availability of human resources with specific quantitative and qualitative characteristics. |

Creation of the necessary conditions for the realization of the labor potential within the territory of the ICC operation. |

Social sector |

Meeting the social needs of individuals within the internal ICC environment. |

Meeting the social needs of individuals within the external ICC environment. |

Management sector |

Improving the management of elements of the internal ICC environment. |

Improvement of the ICC interaction with the external environment. |

Note: author’s development

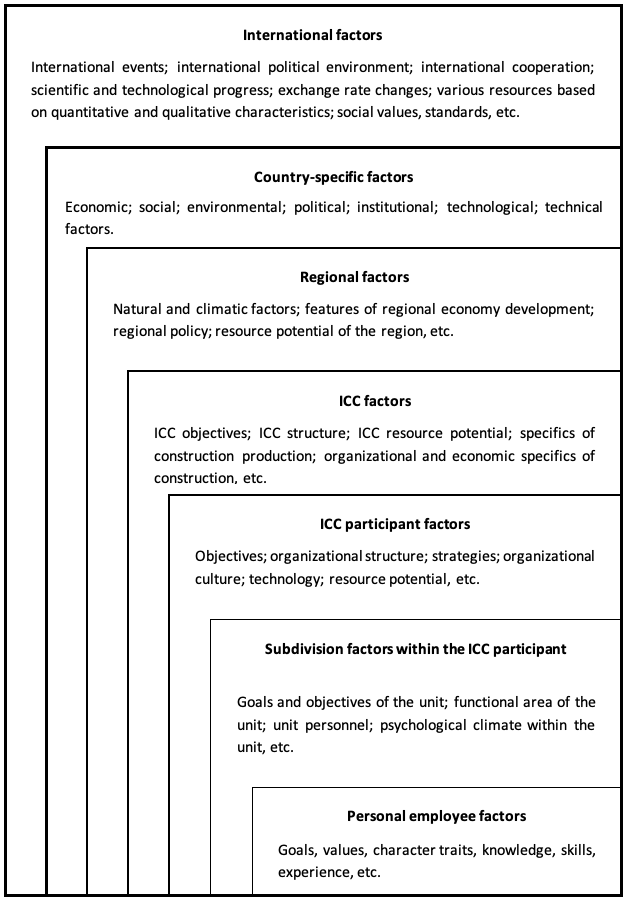

Based on different approaches to describing the ICC functioning factors (Berkovich and Golubkina, 2010, p. 25; Voronin, 2007, p. 28; Lyulin, 2015, p. 237), it is proposed to consider them within seven interrelated groups:

Relevant factors within these groups are shown in Figure 1.

Figure 1

ICC functioning factors

The first three factor groups are part of the ICC external environment. International factors and country-specific factors form the environment of indirect impact on the ICC, and the regional factors belong to the direct impact environment.

As for the factors at the ICC level, as well as of ICC participants, the units within the ICC participants and the personal employee factors, they are considered as the internal ICC environment.

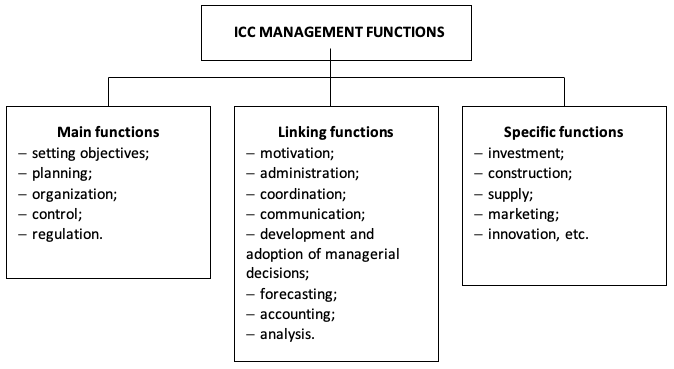

The author proposes three main approaches to the classification of management functions: discrete, discrete-continuous and continuous, and the following classification of ICC management functions (Figure 2).

Figure 2

Classification of ICC

management functions

ICC management functions are represented by three groups. The first group includes the main management functions: setting objectives, planning, organization, control, and regulation. These functions form the management cycle.

The second group contains linking functions, which, in the author's opinion, include motivation, administration, coordination, communication, development and adoption of managerial decisions, forecasting, accounting, and analysis. It should be noted that forecasting is considered as a linking function, as, in the opinion of the author, its implementation must accompany the performance of all the above basic management functions. For example, forecasting within control allows forecasting possible deviations in the management process. These possible deviations can be taken into account during the execution of the regulatory function, which requires their elimination. Thus, the forecasting function connects control and regulation, as well as all other functions of the first group.

The content of the main and linking management functions is presented in the table (Table 2).

Table 2

Main and linking

management functions

Function group |

Function name |

Function content |

Main |

Setting objectives |

Description of intentions, the image of the desired state of the management object. |

Planning |

Defining the necessary actions, their sequence, timing and resources to achieve the objectives. |

|

Organization |

Formation of the structure, distribution of powers and responsibilities. |

|

Control |

Identification of various deviations in the management process, determining the degree of achievement of goals. |

|

Regulation |

Development of corrective measures aimed at eliminating the identified deviations in order to ensure the achievement of the set goals. |

|

Linking |

Motivation |

Encourage participants in the process of achieving the goals to take the necessary actions. |

Administration |

Command through instructions, orders. |

|

Coordination |

Ensuring coherence among the participants involved in the process of achieving the objectives. |

|

Communication |

Formation and functioning of information flows (Rokhchin, Zhilkin, Znamenskaya, 2010, p. 149). |

|

Development and adoption of management decisions |

Development of solutions to management problems, a choice of a suitable option for achieving the objectives. |

|

Forecasting |

Scientific determination of the possible states of the object in question, taking into account the implementation of various management scenarios. |

|

Accounting |

Registration of information on the functioning of the management object, its internal and external environment. |

|

Analysis |

Investigation of the object functioning, its internal, external environment, and identification of cause-effect relations. |

The third group consists of specific ICC management functions, which are related to different areas of its functioning (investment, construction, supply, marketing, and innovation). Implementation of specific functions is carried out by performing basic and linking functions.

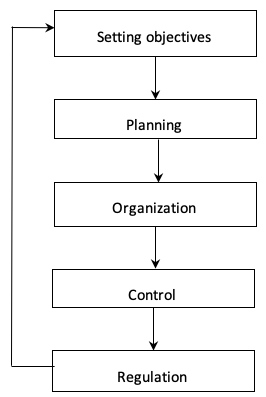

As for the approaches to the classification of management functions, in the author's opinion, one can single out discrete, discrete-continuous and continuous approaches.

The first approach (Figure 3) proposes to consider only the basic management functions and does not focus on linking functions, so this approach has been described as discrete.

Figure 3

Discrete approach to classification

of management functions

This approach can be used in situations where a novice researcher needs to temporarily abstract from the linking functions to focus on the key stages of the management process.

Thus, the discrete approach allows differentiating with a certain degree of conditionality the key stages of the management process (setting objectives, planning, organization, control, and regulation), as well as reflecting the implementation sequence of the mentioned stages. However, this approach does not reveal the complexity of the management process to ensure consistency in the performance of basic functions.

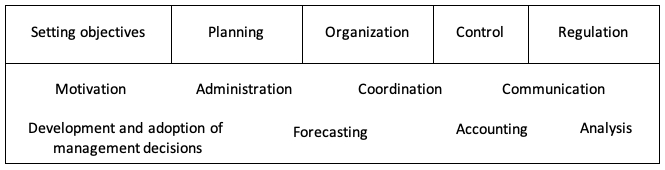

In accordance with the discrete-continuous approach, the performance of the linking management functions ensures the implementation of the main management functions (Figure 4). This approach differs from the discrete one by attention to linking functions, which are carried out at any management stage. However, there is a distinction between basic and linking functions, so this approach is called discrete-continuous.

Figure 4

Discrete-continuous approach to the

classification of management functions

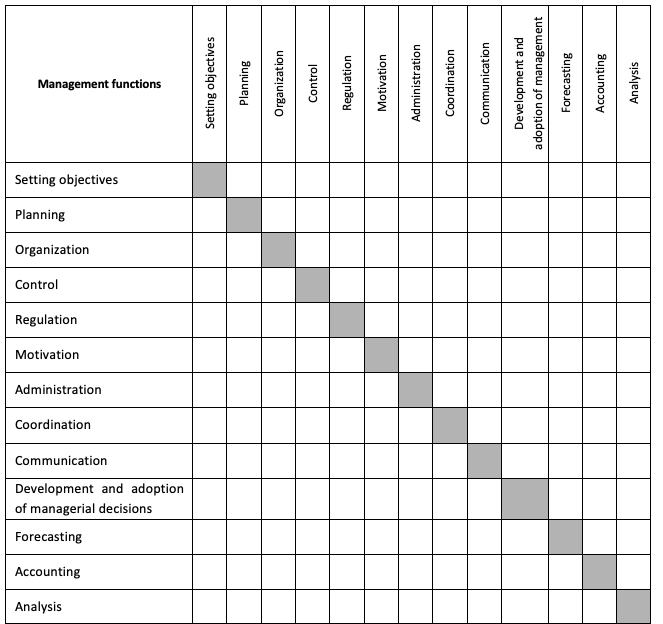

The continuous approach does not imply the division of management functions into main and linking functions. Implementation of each management function requires the performance of the entire set of management functions (Sadykov, 2015, p. 304). Each management function is performed continuously (Table 3), as it is either implemented through other functions or provides their implementation.

Table 3

The continuous approach to the

management functions classification

It should be noted that the continuous approach reflects the complexity of the management process to a greater extent (in comparison with discrete and discrete-continuous approaches), but it does not allow focusing on the sequence of management stages, which makes it difficult for novice managers.

Thus, on the one hand, the activities of the ICC and the successful achievement of its objectives depend on the specific conditions prevailing in the area of its operation. However, on the other hand, the results of the ICC own activities largely determine the opportunities for the development of territories. In the course of the study, special attention was paid to the main ICC objectives; their classification was proposed. It is proposed that the ICC objectives are considered taking into account various areas of its activities (investment, production, labor, social, management).

As a result of the study, a classification of the ICC management functions was proposed, which includes three groups of functions (basic, linking, and specific). The main functions include setting objectives, planning, organization, control, and regulation. Linking functions include motivation, management, coordination, communication, development and adoption of management decisions, forecasting, accounting, and analysis. Specific ICC management functions are related to different fields of its functioning and are represented by investments, construction, supply, marketing, and innovations.

Study limitations: if one considers different types of ICCs, it is likely that differences in the hierarchy of their functions and the success of their performance will be revealed, as recent studies have found "the significant difference" of different types of organizations (Sani, Sharip, Othman & Hussain, 2018, p. 137).

The listed functions are presented by the researcher in the form of a matrix, which shows that the implementation of each of them requires the performance of the entire complex of management functions. The main approaches to the classification of management functions (discrete, discrete-continuous and continuous) are identified and formulated.

The results of the study of the ICC functions and management factors provide an opportunity to better understand the ICC management process. In addition, the use of these results for ICC management can contribute to its more effective functioning.

Abuazoom, M.M.I., Hanafi, H.B., & Bin Ahmad, Z.Z. (2019). Do human resource management (hrm) practices improve project quality performance? Evidence from construction industry. Quality – Access to Success, 20(169), 81–86. Retrieved from https://www.srac.ro/calitatea/en/arhiva/2019/QAS_Vol.20_No.169_Apr.2019.pdf

Addis, M. (2016). Tacit and explicit knowledge in construction management. Construction Management and Economics, 34(7/8), 439–445. https://doi.org/10.1080/01446193.2016.1180416

Ali, Z., Zhu, F., & Hussain, S. (2018). Identification and assessment of uncertainty factors that influence the transaction cost in public sector construction projects in Pakistan. Buildings, 8, 157. https://doi.org/10.3390/buildings8110157

Asaul, A.N., Asaul, N.A., Alekseev, A.A. and Lobanov, A.V. (2009). Investment and construction complex: scope and boundaries of the term. Bulletin of Civil Engineers, 4 (21), 91-96.

Berkovich, M.I., & Golubkina, K.A. (2010). Investment and construction complex of the region: status, problems, performance evaluation. Kostroma, Russia: Publishing house of Kostroma State Technological University. 127 p.

Chen, W.T., Merrett, H.C., Lu, S.T., & Mortis, L. (2019). Analysis of key failure factors in construction partnering – a case study of Taiwan. Sustainability, 11, 3994. https://doi.org/10.3390/su11143994

Gluch, P., Gustafsson, M., Baumann, H., Lindahl, G. (2018). From tool-making to tool-using – and back: Rationales for adoption and use of LCC. International Journal of Strategic Property Management, 22(3), 179-190. https://doi.org/10.3846/ijspm.2018.1544

Guner, A.F., & Benli, G. (2019). Project management in conservation and restoration of historic buildings. SAR Journal, 2(1), 24-30. https://doi.org/10.18421/SAR21-04

Häkkinen, T., & Belloni, K. (2011). Barriers and drivers for sustainable building. Building Research & Information, 39(3), 239-255. https://doi.org/10.1080/09613218.2011.561948

Khrustalev, B.B., Gorbunov, V.N., Musatova, T.E. (2015). Investment and construction complex: experience and development prospects. Penza, Russia: PGUAS. 220 p. Fayol, H. (1949). General and industrial management. London: Sir Isaac Pitman & Sons. 113 p.

Lyulin, P.B. (2015). Development of the regulation system of the investment and construction complex. Doctoral thesis. Saint Petersburg, Russia: St. Petersburg State University of Architecture and Civil Engineering. 322 p.

Mintzberg, H. (1975). The manager's job: folklore and fact. Harvard Business Review, 53 (4), 49-61.

Mohd-Rahim, F.A., Mohd-Yusoff, N.S., Chen, W., Zainon, N., Yusoff, S., & Deraman, R. 2016. The challenge of labour shortage for sustainable construction. Planning Malaysia: Journal of the Malaysian Institute of Planners, 5, 77-88. http://dx.doi.org/10.21837/pmjournal.v14.i5.194

Qian, Q.K., Chan, E.H.W., & Khalid, A.G. (2015). Challenges in delivering green building projects: Unearthing the transaction costs (TCs). Sustainability, 7, 3615-3636. https://doi.org/10.3390/su7043615

Rokhchin, V.E., Zhilkin, S.F. and Znamenskaya, K.N. (2010). Strategic planning of Russian cities development: systematic approach. 2nd edition, Tolyatti, Russia: Togliatti State University. 444 p.

Sadykov, H.S. (2015). Strategy of investment and construction complex in regional development. Saint Petersburg, Russia: Publishing house of the Polytechnic University. 354 p.

Sani, J.A., Sharip, N.A.A., Othman, N., & Hussain, M.R.M. (2018). Relationship between types of organization with the quality of soft-scape construction work in Malaysia. Asian Journal of Quality of Life, 3 (12), 137-146, https://doi.org/10.21834/ajqol.v3i12.150

Semenova, F.Z. and Dzhambaev, R.A. (2010). Risk management of investment and construction complex of the region. Moscow: Prometheus. 204 p.

Subramanyam, K. & Haridharan, M.K. (2017). Examining the challenging hindrances facing in the construction projects: South India's perspective. In IOP Conference Series: Earth and Environmental Science, 80, 12-45. https://doi.org/10.1088/1755-1315/80/1/012045

Thomson, C.S., El-Haram, M.A. (2019) Is the evolution of building sustainability assessment methods promoting the desired sharing of knowledge amongst project stakeholders? Construction Management and Economics, 37(8), 433-460. https://doi.org/10.1080/01446193.2018.1537502

Timms, H.L. (1962). The production function in business. Homewood, Illinois, US: Richard D. Irwin. 546 p.

Vakhmistrov, A.I. (2004). Management of the metropolis investment and construction complex. Saint Petersburg, Russia: Publishing House Stroyizdat SPb. 224 p.

Voronin, A.V. (2007). Improvement of the regional investment and construction complex management system. Saint Petersburg, Russia: Rost. 170 p.

Zaguskin, N.N. (2015). Transformational development of subjects of the regional investment and construction complex at the self-regulation stage. Saint Petersburg, Russia: Autonomous non-profit organization IPER. 336 p.

1. Associate Professor, Department of construction management, Saint Petersburg State University of Architecture and Civil Engineering, 190005, St. Petersburg, Russia. Contact e-mail: kharitonovichav@mail.ru

[Index]

revistaespacios.com

This work is under a Creative Commons Attribution-

NonCommercial 4.0 International License