![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 40 (Number 24) Year 2019. Page 21

KHUSAINOVA, Natalya 1 & VOROZHEYKINA, Tatyana 2

Received: 02/04/2019 • Approved: 24/06/2019 • Published 15/07/2019

ABSTRACT: The fur industry is currently in a crisis, one of the main reasons for which is the free access of imported fur products and skins to the Russian market. At the same time, Russian farming is also influenced by the general negative trends characteristic of fur farming: high price volatility for fur products with price growth rates below inflation. This requires, on the one hand, an increase in the efficiency of production of skins, and on the other hand, an increase in sales efficiency. Replacing imported products in the domestic market at the expense of domestic production will be a solution to the problem in conditions of a limited growth in the purchasing power of the population. The creation of a cluster in the Kaliningrad region is proposed for the realization of this, which will ensure the growth of production of both mink skins and finished products with a gradual replacement of imported products. |

RESUMEN: La industria de las pieles se encuentra actualmente en una crisis, una de las razones principales es el acceso gratuito al mercado ruso de pieles y productos de piel importados. Al mismo tiempo, la agricultura rusa también está influenciada por las tendencias negativas generales características del cultivo de pieles: alta volatilidad de los precios para productos de piel con tasas de crecimiento de precios por debajo de la inflación. Esto requiere, por un lado, un aumento en la eficiencia de la producción de pieles, y por otro lado, un aumento en la eficiencia de ventas. Reemplazar los productos importados en el mercado nacional a expensas de la producción nacional será una solución al problema en condiciones de un crecimiento limitado en el poder de compra de la población. Se propone la creación de un grupo en la región de Kaliningrado para la realización de esto, que garantizará el crecimiento de la producción de pieles de visón y productos terminados con un reemplazo gradual de los productos importados. |

In recent years, there has been a decline in the Russian market of mink fur production, which is accompanied by both a decrease in production volumes and the arrival of fur products from China to the Russian market – more affordable but of poor quality. The reduction of import customs duties on fur raw materials, tanned and dressed fur skins has a negative effect on the Russian animal industry. According to the National Fur Association, about 40 Russian enterprises with a total production of 2–2.5 million pelts per year worth more than 3.5 billion rubles are now engaged in the production of cell fur-bearing animals (Hansen, 2014; Goriainova, 2017). These enterprises are village-forming and bear the full social burden of life support of rural settlements in 25 regions of Russia. At the same time, the world fur market has been in crisis since 2014: for example, overproduction of mink skins has led to a fall in world prices by more than three times (Fur Commission USA, 2018). Thus, reducing import duties on imported products - the domestic industry loses a significant share of profits. In addition, from January 1, 2018, the tax burden on fur farming in the form of value added tax from which enterprises were previously exempted (in addition to the single agricultural tax) has increased, which also does not allow in the current conditions to increase the potential of the domestic industry. Also, on fur farming, the federal law of November 27, 2017 No. 335-FZ (Government of the Russian Federation, 2017) on amending tax legislation, namely, on taxation of VAT at a rate of 10%, does not apply to the sale of the breeding fur animal under leasing contracts (Government of the Russian Federation, 2017). These measures lead to higher prices for breeding animals. For comparison: in case of sale on the sale and purchase of pedigree mink by installments, the rise in price per year is approximately 8% (against 2% in cattle). The relevance of the research topic is due to the fact that in the current situation on the Russian market of mink farming and global trends in the development of this industry, there are negative trends, which in turn does not allow domestic producers to increase production rates by increasing production volumes, including for export.

The purpose of the study is to determine the prospects for developing the fur industry and searching for alternative ways out of the crisis. Analysis of the situation on the world market and the activities of animal breeding enterprises in the region, the search for initiatives of potential solutions for the development of the industry in the region are included in the research tasks. Authors, such as A. Kolokolnikov, D. V. Neskoromny, H.O. Hansen, studied the trends and prospects for the development of the fur industry. The current study is a contribution to the dynamic body of knowledge on this topic.

Fur farming is a branch of animal husbandry for captive breeding of valuable fur-bearing animals and supplying animal skins to the domestic and global market (Dolgosheva & Milyutkina, 2011).

In the 1980s, 12 million skins per year were produced in Russia (up to 40% of global production). By the beginning of the 2000s, our country lost its leading position, reducing the production of fur to 3% of the world total. Global production of furs, in contrast, over the past 20 years has increased from 30 million pelts in 1990 to 83 million pelts in 2015. Now the main production of furs is concentrated in the European Union (38 million mink pelts per year) and China (10 million pieces) (Dyatlovskaya, 2018).

According to Rosstat (2018), at the end of 2017, the breeding stock of fur-bearing animals of cell breeding in agricultural organizations was about 430 thousand animals. The main herd of salable fur animals accounts for mink. In Russian agricultural organizations by the beginning of 2017, there were 352 thousand individuals (compared with 2010, a decrease of 14%). During 2017, 1.2 million minks were slaughtered by producers of skins (by 2.9% less than in 2016), 52 thousand sables (a decrease by 18%), 39 thousand foxes (10% less), 15 thousand arctic foxes (56% reduction).

In addition, a significant weakening of the industry was due to a decrease in import duties on imported furs. Currently, they are minimal and do not allow the development of the domestic industry, although the potential for increasing the production of skins and ensuring the needs of the market for fur farming is available.

The study of the fur industry using the matrix model of the Boston consulting group (Khusainova, 2014) allowed us to identify the leaders in exports/imports of mink pelts. Russia's position in exports cannot be classified as advanced, and in terms of imports Russia is in the forefront, which means an increased demand for imported furs and, at the same time, low competitiveness in the foreign fur farming market.

In order to strengthen the Russian economy in the fur industry, it is necessary to increase the potential in the field of animal breeding, and also to carry out breeding work to increase the mink gene pool, which will allow foreign goods to be crowded out with goods of high quality. This creates prerequisites for the development of import substitution in the industry. Consider the concept of “import substitution”. The founders of the concept of import substitution include representatives of the theory of mercantilism Thomas Mans, Antoine Montchretien, and Jean-Baptiste Colbert, who substantiated the need for active state intervention in economic activity, mainly in the form of protectionism — setting high import duties, issuing subsidies to national producers, etc. At present, all developed countries apply protectionism; however, this is not open but hidden protectionism, since to overcome the technological backwardness and active growth of the industry, it is necessary to introduce protectionist measures and restrict the import of competing industrial good (Reinert & Reinert, 2011).

Import substitution is the reduction or cessation of imports of a particular product through the production, release in the country of the same or similar goods (Borisov, 2004).

We can formulate own definition of “import substitution of domestic fur”: the development of the domestic animal industry by increasing the production of fur and increasing sales in the domestic market by integrating advanced technologies in the technology of growing fur animals and the production of finished products.

There is also an opinion that the emergence of mass poverty in countries with insufficient raw materials and agricultural base precisely led to the lack of import substitution and their insecurity from the penetration of foreign goods (Bruton, 1998).

In Russia, according to R. Connolly (Connolly et al., 2016), a certain shift in the policy of import substitution towards localization occurs, namely, the transfer of production of foreign goods to the territory of the Russian Federation, thus changing the nature of Russia's integration with the global economy in order to stimulate both the domestic economy and national security.

To protect and support domestic fur farming by the state, some steps have been taken. Thus, in 2013, the sectoral target program was adopted by the Ministry of Agriculture of the Russian Federation “Development of cellular fur farming in the Russian Federation for 2013-2020”. The creation of economic and technological conditions for the restructuring of the branch of the fur cell farming industry and the restoration of furs production volumes within the limits of the value of domestic demand and export opportunities of Russia was its main task (Ministry of Agriculture of the Russian Federation, 2013). According to this program, the livestock of animals by 2020 should increase by half, and the production of skins schould reach the level of 3.9 million.

In turn, the regional program for the support of local fur farmers was adopted by the Government of the Kaliningrad region (Government of the Kaliningrad region, 2013). The program provides for the modernization and construction of cells for the maintenance and cultivation of mink, the purchase of equipment for the preparation and distribution of feed, the purchase of equipment for the primary processing of furs and the acquisition of highly productive breeding young cell mink. For the development of the fur industry, this article proposes to consider creating a model of a fur farming cluster.

A cluster is an association of enterprises, suppliers of equipment, components, specialized production and service services, research and educational organizations connected by relations of geographical proximity and functional dependence in the production and sale of goods and services (Ministry of Economic Development of the Russian Federation, 2008).

Also according to S. N. Kotlyarova, the definition of a cluster is understood as a set of economic entities of an adjacent profile, interconnected and complementary to each other, closely spaced and contributing to the overall development and growth of each other’s competitiveness (Kotlyarova, 2012).

The potential points of economic growth of the industry can be modeled through the development of a cluster theory, which includes the concept of closely located economic entities and institutions that are interconnected and deeply integrated into the regional economic system.

The locality of a regional cluster does not limit the possibility of forming points of world growth and reproduction systems that have access to the world economic space and are marked by economic boundaries many times exceeding administrative. Within the cluster, the basic components of the export potential are formed, namely its production, labor, marketing, and financial components (Sapir, Karachev & Chzhan, 2016).

To study this problem, general scientific methods and methods of analysis (general logical and empirical), economic research methods (abstract logical method, method of comparative and selective analysis, statistical methods) were used in this article.

Official statistics of Russia, the Kaliningrad region; data from the International Fur Federation International Fur Federation, data from the European Association Fur Europe, data from the Economic Information Agency "PRIME" of financial statements; the sectoral target program “Development of cellular fur farming in the Russian Federation for 2013–2020” served as the information base for the research. The development of a cluster model for the development of the animal industry in the Kaliningrad region was obtained by analyzing data on producers and potential feed suppliers, as well as on analyzing the current state of the industry as a whole. The theory of cluster development and the theory of import substitution formed the theoretical basis of the study. Data on world mink production and data on the fur industry in the Kaliningrad region are analyzed in the article.

According to the International Fur Federation (IFF), 71.27 million mink hides were produced in the world in 2015, the total value of which amounted to 3.57 billion USD (International Fur Federation, n.d.). The fur industry encompasses the global fur trade and industry, which employs over a million people worldwide and is an important part of the economies of many countries.

Also, the report of the International Fur Association emphasizes how many different countries are involved in the production of various types of fur used throughout the world. Only Brazil is in the sixth part of the global economy of chinchillas, while most of the rest is in Europe, including Denmark, Hungaryб and Romania. Almost 95% (9 million) of furs produced globally in 2015 accounted for Finland and China (International Fur Federation, n.d.).

According to the European Association (European Fur Manufacturers Association “Fur Europe”, 2018), Denmark is in the first place in mink production in Europe in 2016 (17 million heads), Poland is in second place (8 million heads), Holland is in third place (4.8 million heads) followed by Finland and Lithuania (1.9 million heads).

In 2015, mink production in China declined to 18 million, mainly due to mixed economic prospects in the Chinese market, especially for luxury goods. Slowing production in China has certainly affected sales in this market, which, in turn, has led to a reduction in production worldwide. Nevertheless, China remains a strong market participant with a large increase in production.

According to H. O. Hansen (Hansen, 2017), countries export fur clothing to Russia for $ 2.0-2.5 billion a year, while there has been a steady increase since 2008, despite financial, economic, and political crises.

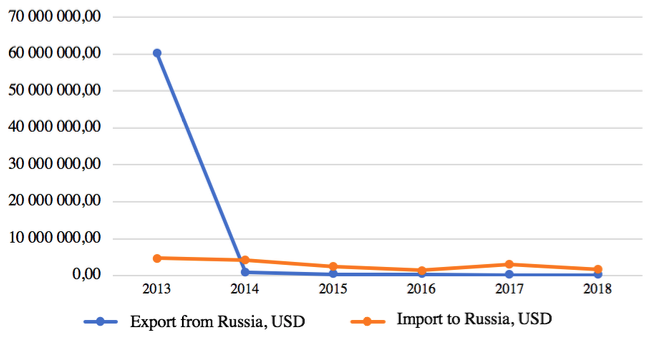

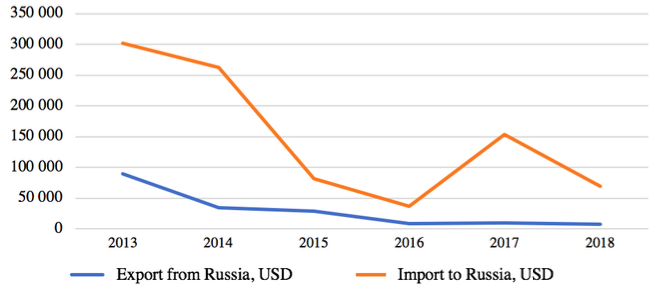

Analyzing the data for 2013-2018 for a product from the group of "tanned mink fur skins” (Russia: Statistics of foreign trade, 2013; Russia: Statistics of foreign trade, 2018), it can be noted that the export of mink fur raw materials from Russia has significantly decreased in recent years, and the import of mink skins has intermittent changes due to the cyclical nature of the demand for fur products.

Exports from Russia for the period 2013-2018 for the group of goods “tanned mink fur skins” as a whole amounted to 62.3 million USD (177 thousand pieces). In terms of exporting countries, Germany is in the first place (54%), Anguilla is in the second place (38%), which can be considered an exception, since there was a single delivery in 2013; therefore, the Netherlands and China are more correct to consider being on the second place (Table 1).

Figure 1

Dynamics of export and import of dressed mink skins for the period 2013-2018, USD

-----

Figure 2

Dynamics of export and import of dressed mink skins for the period 2013-2018, in pieces

Imports to Russia for the period 2013–2018 for the group of goods “tanned or dressed mink fur skins whole” amounted to 17.7 million USD in the amount of 903 thousand pieces. In the structure of imports by country, China ranks first (26%), Germany is second (19%) (Table 1).

Also, in terms of production in Russia (Rosstat, 2016), it can be noted that for the period 2010-2015, abrupt changes in the volume of finished fur products have occurred, which means unstable production, as well as in the number of production of mink skins after the 2010 (Table 2). Significant reduction in production is noticeable in parts of long-haired furs such as arctic fox, fox.

Table 1

Structure of exports / imports of mink pelts in the

structure of countries, cumulatively for 2013-2018

№ |

Exports from Russia |

Import to Russia |

||

A country |

total exports for the period 2013-2018 |

A country |

total imports for the period 2013-2018 |

|

1 |

Germany |

$33.6 million |

China |

$4.5 million |

2 |

Anguilla (British overseas territory) |

$23.5 million |

Germany |

$3.3 million |

3 |

Netherlands |

$2.4 million |

Hong Kong |

$3.2 million |

4 |

China |

$1.1 million |

Belarus |

$1.5 million |

5 |

Greece |

$686 thousand |

Poland |

$1.4 million |

6 |

Italy |

$493 thousand |

Greece |

$1.1 million |

7 |

Hong Kong |

$491 thousand |

Italy |

$744 thousand |

8 |

Belarus |

$52.7 thousand |

England |

$418 thousand |

-----

Table 2

Production of main types of products of textile

and clothing manufacture in Russia

Name of the indicator |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

Furs and fur products made of natural fur, thousand pcs. |

|

|

|

|

|

|

including: |

||||||

mink skins, dressed, whole, with or without head, tail or paws, unassembled |

477 |

364 |

361 |

481 |

474 |

545 |

blue fox pelts, fur, dressed with or without head, tail or paws, unassembled |

96.5 |

42.8 |

43.9 |

50.7 |

67.9 |

48.1 |

silver-black and silver-black white-skinned skins of foxes, dressed with or without head, tail or paws, unassembled |

24.9 |

12.3 |

13.2 |

6.8 |

14 |

10.8 |

fur collars |

79.3 |

94.4 |

91.2 |

44.9 |

37.8 |

26.8 |

coat, short coat, men's, made of natural fur |

3.5 |

0.8 |

2.6 |

1.1 |

0.7 |

2.2 |

coat, short coat, female, with natural fur |

82.6 |

93.6 |

100 |

115 |

108 |

89.9 |

In addition, Russian indices of the physical volume of retail sales of fur goods were analyzed (as a percentage of the previous year). The data (Rosstat, 2017; Rosstat, 2018) show that the demand for fur products for many years has practically no sharp fluctuations, and only a slight decrease was observed in 2015 (Table 3).

Also, according to the data of (Kolokolnikov, 2013), finished fur products are purchased in China – more than 400 million USD. It turns out that the demand for finished products in Russia is high (about 10 million skins per year), the demand for products in Russia remains, and according to (Russia: Foreign Trade Statistics, 2017), the share of imports from China and Hong Kong is quite large (for 2017, imports amounted to 1.2 million dollars or 38% of the total imports of mink skins).

Table 3

Volume indices of retail sales

of selected goods in Russia

Indicator (as a percentage of the previous year) |

Years |

|||||||||

92 |

00 |

05 |

10 |

12 |

13 |

14 |

15 |

16 |

17 |

|

Fur clothes |

117 |

105 |

108 |

101 |

103 |

101 |

101 |

89 |

94,3 |

97,3 |

Consequently, the import and export of mink raw materials has noticeably decreased over the past 5 years, and the import of finished products to Russia has not decreased (it increased by 0.4 million USD in 2017). It should be noted that the decline in exports of dressed mink pelts from Russia shows 2 aspects of the industry development trend: 1) decline in production (according to Rosstat, by the beginning of 2018 there were 357 thousand minks, which decreased by 15% compared to 2016); 2) most of the products are purchased by domestic manufacturers of finished products.

As of the beginning of 2018, in the Kaliningrad region, 3 animal breeding facilities are operating: the Open Joint-Stock Company “Agrofirm “Bagrationovskaya”, the Open Joint-Stock Company “Agrofirm “Prozorovskaya”, the Closed Joint-Stock Company “Animal Breeding “Guryevskoe”. The Closed Joint Stock Company “Beregovoy” ceased to exist in 2017.

In recent years, the farming industry has significantly reduced economic indicators. In addition to common problems typical of the entire domestic animal industry, Kaliningrad animal producers after 1991 faced the problem of separation from the main territory of the country (Neskoromny, 2009).

The profitability of this field decreased from 11% in 2015 to 1% in 2017. At the same time, the share of Kaliningrad furs in the Russian market decreased from 30% in 2015 to 17% at the end of 2017. In 2014, in connection with the sanctions imposed against the Russian Federation, along with Latvian sprats and dozens of other food products for animal farms, they no longer enter the Russian market, namely substandard fish, which is the basis of the mink ration. Despite the difficulties, many enterprises, thanks to state support, were able to reorient themselves, although not fully to Russian products, which are more expensive for Kaliningrad animal farms (by 6 rubles per kilogram on average).

On the basis of the annual accounting reports (Agency of Economic Information “PRIME”, 2018) presented for the disclosure for 2010-2017, Table 1 presents a quantitative characteristic of the livestock of Kaliningrad animal farms for the analyzed period. As indicated in (Khusainova, 2014), about 30% of the Russian mink (the main herd of breeding stock) accounted for the Kaliningrad region in 2011-2014. In 2017, this figure was less than 17%. At the same time, the trend is currently reducing the production of regional mink. This is indicated by the statistics data (Agency of Economic Information “PRIME”, 2018), as well as according to the data of the Research Institute of Fur Breeding and Rabbit Breeding named after V. A. Afanasyev, in the Kaliningrad region, the number of females of the main herd (heads) over the past 3 years has decreased by almost 40 thousand heads (in 2014, the number was 11.7 thousand heads, by 2017 the number was reduced to 70.9 thousand heads). A significant drop in mink production is due to the bankruptcy of one of the leaders in mink production in the region – the “Beregovoy” CJSC.

The total number of mink business output in the Kaliningrad region also decreased over the past 3 years: 482 thousand heads in 2013, 450 thousand heads in 2014, 486 thousand heads in 2015, 293 thousand heads in 2017.

The number of workers in fur farming enterprises (Agency of Economic Information “PRIME”, 2018) (Table 4) also significantly decreased after 2013 (by almost 50%), the main reason was the bankruptcy of one of the leading enterprises, which led to an increase in unemployment and a decrease in tax revenues to the regional budget.

Table 4

Information on the average annual number and

accrued wages of employees of organizations

Indicator |

Years |

|||||||

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

|

Agricultural workers, people |

474 |

475 |

483 |

529 |

491 |

458 |

407 |

278 |

Accrued wages of employees of organization, mln. rubles |

88.2 |

104.6 |

118.4 |

142.9 |

135.9 |

138.8 |

118.5 |

87.0 |

For the period from 2010 to 2017, regional authorities provided support to Kaliningrad animal farms in the total amount of 217.842 thousand rubles, including 116.120 thousand rubles from the federal budget (Table 5). During the period from 2010 to 2017, regional authorities provided support to the Kaliningrad animal breeding industry in the total amount of 217.842 thousand rubles, including 116.120 thousand rubles from the federal budget (Table 5).

Table 5

The amount of state support for Kaliningrad

animal farms for the period 2010 - 2017

Indicator |

Years |

|||||||

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

|

Volume of state support total, thousand rubles |

18 724 |

16 294 |

24 295 |

47 965 |

35 450 |

38 684 |

26 797 |

9 633 |

including at the expense of the federal budget, thousand rubles |

12 700 |

9 768 |

16 929 |

20 808 |

14 720 |

23 894 |

17 301 |

- |

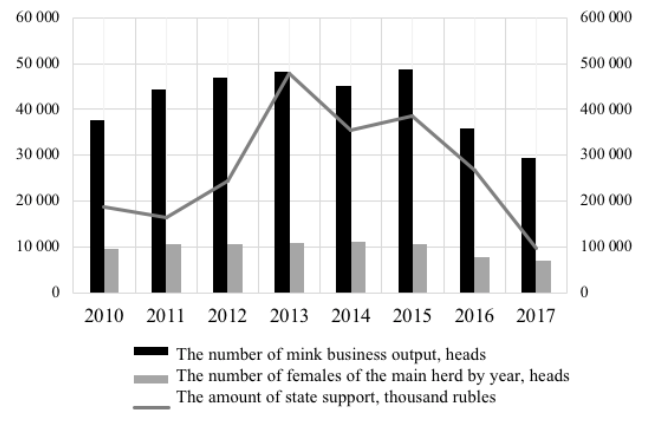

Analyzing information on state financial assistance, it can be noted that regional farming improved the production of females of the main mink herd, which is characterized by an increase in their number during the years of receiving the greatest state support (Figure 3).

Figure 3

Dynamics of indicators of the impact of state support on

the performance of animal farms in the Kaliningrad region

As can be seen from Figure 3, the influence of state support increases the potential for the development of local animal farms, for the subsidies received there is an opportunity to re-equip equipment, purchase new breeds of mink, due to which it is possible to stimulate labor productivity by increasing the remuneration of employees.

Logistics components can be attributed to the main problems of the region in fur farming: 1) the EU competition, 2) the supply of feed, 3) the import of mink animals, and 4) the export of fur from the region. In addition, since there are no such well-known mink brands in Russia as Saga furs (Scandinavian mink) or Black Glam (American mink), a small number of Russian furs at world auctions, the heterogeneity of skins make them unattractive in the eyes of buyers, and they disperse at the lowest price.

The high cost of feed is one of the main problems in the development of animal farming in the region. Fodder is mainly purchased abroad and in Russia, since the entire branch of the mink farming of the region cannot be provided with regional fodder. The quality of mink fur is directly dependent on feed: one needs a variety of foods rich in phosphorus, vitamins, rich in saturated fats. In addition, domestic fur farmers have to compete with Western manufacturers of fur, the quality of which is at a high level. Also, on the quality of the skins and the demand they enjoy on the market, the overall decline in the level of breeding control is negatively affects. The use of new technologies for raising animals, the development of their own food supply, competent breeding work with animals, improving the quality and competitiveness of products, the development of production and processing base of animal breeding farms can be the main ways to stimulate the development of the industry.

On the basis of the formulated task, attempts are made to comprehend the main ideas of strategizing in relation to the enlarged structure of the socio-economic system of the Kaliningrad region, including the agro-industrial and tourist-resort complexes, industry, infrastructure, and human capital.

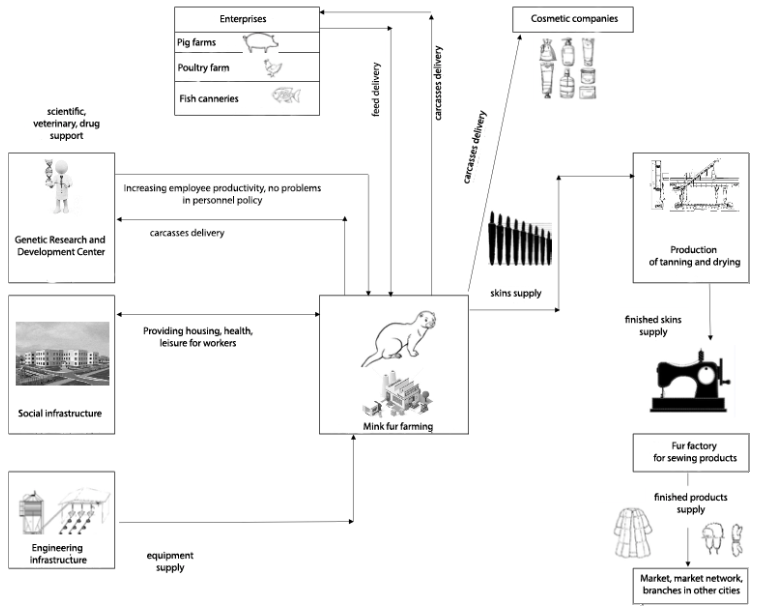

Supply of feed base, as well as the sale of finished products and the purchase of breeding animals, are the main problems of the Kaliningrad region in organizing the production of mink. The organization of a cluster model on the territory of the Kaliningrad region may be a possible solution. The proposed model of a full-complex cluster on the organization of mink farming (Figure 4) includes various subcomplexes both accompanying and ensuring the functioning of farming from the initial stage of growing mink to the final stage of selling fur products to the final consumer.

Figure 4

Organization of a fur farming cluster

The primary conditions for the functioning of farming is its interaction with the breeding and genetic center, since successful breeding of the mink, the development of a better breed, resistance to various diseases, and more depend on the selection.

Engineering infrastructure includes the provision of animal breeding with the necessary equipment, namely sheds, feed dispensers, feed truck, and other necessary equipment for the functioning of animal breeding.

For the cultivation of mink, a continuous work on the preparation of feed must be carried out; therefore, another important block in the organization of the animal breeding complex is an established supply of feed from suppliers. Taking into account the fact that the cost of feed is up to 80% in the cost of mink skins, the use of local suppliers will reduce the cost of finished products [9].

The main ration of mink is feed:

Due to climatic conditions and location (availability of access to the Baltic Sea), there are fish processing enterprises in the Kaliningrad region: according to Rosstat, as of January 1, 2018, 149 units of fisheries and fish farming enterprises were registered in the Kaliningrad region, it was processed and mothballed 369.7 thousand tons in 2017, (231.6 thousand tons were frozen, 175.6 million services were produced) (Kaliningradstat, 2018).

Also, according to Rosstat (Kaliningradstat, 2018), over the past 5 years, from 2013 to 2017, poultry production in the region increased by 30% (1952.2 thousand heads in 2013; 2508.6 thousand heads in 2017). In the region, a new factory was opened in 2018, the Poultry-breeding complex “Food Products” LLC, due to which the production of chicken meat will increase by 10 thousand tons of units per year. In addition, other poultry farms are located in the region: the Poultry Farm Guryevskaya LLC, the TPK LLC, the Baltic Poultry Company LLC, with a total production of about 25 thousand tons of meat per year.

In turn, fur farming after slaughter of mink faces the problem of disposal of its carcasses. The agreement on the supply of carcasses to the poultry farm must be concluded to solve it for grinding into meat and bone meal, which can be used to feed poultry. In addition, the processing of meat of fur animals can be used to obtain a useful hydrolyzate, which in turn can solve other problems of domestic farming. The drug is able to dispose of waste and increase the number of mink. Thus, mink meat undergoes enzymatic hydrolysis: it is placed in the reactor, an enzyme is added that promotes the breakdown of the protein molecule to amino acids and the process is carried out at certain temperature and time parameters. The enzyme, in turn, can be obtained from the biological waste of the pancreas of cattle or pigs. Under the influence of the enzyme, the meat turns into a liquid hydrolyzate, which can be dried to a powder. The liquid product is stored in clean containers in refrigerated chambers, the powder is stored in a sealed package for years.

Also, when disposing of mink carcasses, it is possible to interact with cosmetic companies, since mink carcasses contain technical fat that can be used in the manufacture of creams and soaps.

After the slaughter of mink, the obtained skins must be sent for dressing and drying; therefore, the presence in the region of an enterprise for dressing skins will significantly reduce transport costs. (Currently, some animal breeding send skins for dressing outside the region, for example, to Novosibirsk), and reduce the time spent on dressing and drying the skins. Own enterprises for the manufacture of mink skins are also available, for example, the "Prozorovskaya" CJSC is engaged in dressing mink pelts in a conglomerate collaboration with the "Profra" CJSC, located on the territory of fur farming.

The provision of housing for fur workers is related to social infrastructure. In the Kaliningrad region, this issue is resolved by providing housing for rural workers with the state support, since the fur farming located on its territory is village-forming, and in order to attract fur farming workers to the rural area, additional incentives are needed.

Also, the provision of health care for workers is related to the social infrastructure: having a dentistry office and paying insurance for employees for using the services of the office, providing a sanatorium-resort treatment by sending employees for rehabilitation once a year in a sanatorium on the Baltic coast. In addition, the presence in the farming of its own cultural and leisure complex can be attributed to the social infrastructure – a gym, swimming pool, cinema. Creating conditions of out-of-school employment for the children of the company’s employees will increase the productivity of employees because it alleviates parents’ concerns about the employment of their children while they spend most of their time at work. The same rallying of the team takes place with the help of leisure, which is also aimed at increasing the responsibility and achievement of the highest indicators in fur farming.

The considered model of the cluster functioning of fur farming affects and allows one to engage enterprises already operating in the region, as well as create new jobs, which is relevant because the number of jobs in the region's fur farming industry almost halved in 2017.

Economic feasibility in the model is as follows. First, the preservation of existing jobs and the creation of new jobs, the possibility of forming a state order for training the necessary personnel in the field of fur farming and furriering skills. Second, the involvement of foreign experts in the manufacture of fur, the opportunity to exchange experience on the territory of the Russian Federation. Third, the development of “fur fashion tourism” is possible, as an example for which one can take the fur tourism of Greece (the city of Kastoria, Paralia, Katerini). The infrastructure for tourism in the Kaliningrad region is fully secured; therefore, the interest of potential tourists can be increased not only by sea recreation, the purchase of amber products but also by finished products from mink fur. Fourth, the cost of finished products sewn in the region for the final consumer would be significantly lower than abroad, since transport costs, customs, and insurance fees are reduced for it.

The research conducted and presented in this article allow us to draw the following conclusions:

At present, the farming industry in Russia has a low production rate (compared to Denmark, Finland, the Netherlands, Poland, and China).

The availability of cheap fur products from China and Hong Kong in the domestic market of Russia makes the farming industry more unstable in Russia, destabilizing their economic condition.

The decline in Russian mink exports over the past 5 years (from 2013 to 2017) shows a lack of mink production in Russia, and does not allow competing in international fur markets;

Import of mink skins has a spasmodic development, while the need for fur products in Russia is about 10 million skins per year, with domestic production of about 2 million skins per year.

The production of fur products in Russia is also unstable (according to Rosstat data for 2010-2015), which shows both the instability of the production of mink skins and the cyclical nature of the demand for fur products.

Financial support of the state of domestic producers of fur farming directly affects the growth of their production potential (for example, the Kaliningrad region).

The development of the fur industry in the Kaliningrad region in 2017 on an all-Russian scale slowed down significantly due to the closure of one of the leading enterprises in the region.

Analysis of aspects of creating a model of cluster farming allows one to identify potential points of growth for the industry and possible prospects for further development of the industry in the region.

Agency of Economic Information "PRIME" (2018). General information about the “Agrofirm Bagrationovskaya” JSC. Retrieved from: https://disclosure.1prime.ru/portal/default.aspx?emId=3915007705.

Borisov, A. B. (2004). Large economic dictionary (2nd ed.). Moscow, Russia: Book World.

Bruton, H. J. (1998). A reconsideration of import substitution. Journal of Economic Literature, 36(2), pp. 903-936.

Connolly, R., & Hanson, P. (2016). Import substitution and economic sovereignty in Russia. Retrieved from https://www.chathamhouse.org/sites/files/chathamhouse/publications/research/2016-06-09-import-substitution-russia-connolly-hanson.pdf.

Dolgosheva E. V. & Milyutkina O. V. (2011). Rabbit breeding and fur farming: study guide Ministry of Agriculture of the Russian Federation. Samara, Russia: Samara State Agricultural Academy Samara (SSSAA).

Dyatlovskaya, E. (2018). Import threatens Russian farming. Retrieved from http://www.agroinvestor.ru/analytics/news/30107-import-ugrozhaet-rossiyskomu-zverovodstvu/.

European Fur Manufacturers Association “Fur Europe” (2018). The data of the European Association Fur Europe. Retrieved from https://www.fureurope.eu/fur-information-center/fur-industry-by-country/.

Fur Commission USA. (2018). Data & statistics. Retrieved from https://furcommission.com/econimics-posts/

Goriainova, I. Yu. (2017), Leather and fur garment production in Russia: characteristics and problems. Retrieved from http://ucom.ru/doc/na.2017.04.01.086.pdf

Government of the Kaliningrad region (2013). Resolution of the Government of the Kaliningrad region of June 4, 2013 No. 383 “On the target program of the Kaliningrad region “Development of cellular fur farming in the Kaliningrad region for 2013-2015”. Kaliningrad, Russia.

Government of the Russian Federation (2017) Federal Law of November 27, 2017 No. 335-FZ “On Amendments to Parts One and Two of the Tax Code of the Russian Federation and certain legislative acts of the Russian Federation”. Moscow, Russia.

Hansen, H. O. (2017). The global fur industry in 2016-17. Retrieved from http://curis.ku.dk/portal/en/publications/the-global-fur-industry-201617(03470499-821d-4615b99ae5b7be5cf6fe).html

Hansen, H.O. (2014). The global fur industry: trends, globalization and specialization. Journal of Agricultural Science and Technology, 4, 543-551.

International Fur Federation. (n.d.). Strong global fur trade. Retrieved from https://www.wearefur.com/new-production-figures-reveal-another-strong-year-global-fur-trade.

Kaliningradstat (2018). Kaliningrad region in numbers. 2018: a brief statistical compilation. Kaliningrad, Russia: Kaliningradstat.

Khusainova, N. R. (2014). Market research of the Kaliningrad market of mink products. Bulletin of the Kaliningrad branch of the St. Petersburg University of the Ministry of Internal Affairs of Russia, 2(36), 176-182.

Khusainova, N. R. (2014). Russia's competitiveness in the global market for the sale of mink skins. Modern Competition, 3(45), 139-147.

Kolokolnikov, A. (2013). International fur trade: trends, challenges, prospects. Retrieved from http://www.theseus.fi/bitstream/handle/10024/62759/KolokolnikovAndrey.pdf?sequence=1.

Kotlyarova S. N. (2012). Formation of cluster policy in the regions of Russia. Economy of the Region, 2(30), pp. 306-315.

Ministry of Agriculture of the Russian Federation (2013). Order of the Ministry of Agriculture of Russia dated December 4, 2013 No. 450 “On approval of the sectoral target program “Development of cellular fur farming in the Russian Federation for 2013–2020”. Moscow, Russia.

Ministry of Economic Development of the Russian Federation (2008). Letter of the Ministry of Economic Development of the Russian Federation of December 26, 2008 No. 20615-ak / d19 “Guidelines for the implementation of cluster policy in the constituent entities of the Russian Federation”. Moscow, Russia.

Neskoromny D. V. (2009). The role of the institute of a special economic zone in the development of the animal industry (on the example of the Kaliningrad region). Baltic Economic Journal. Scientific and Practical Journal, 2, 184-196.

Reinert, E. S., & Reinert, S. A. (2011). Mercantilism and economic development: Schumpeterian dynamics, institution building and international benchmarking. OIKOS, 10(1), 8-37.

Rosstat. (2016). Industrial production in Russia. 2016: a statistical compilation. Moscow, Russia: Rosstat. Retrieved from http://www.gks.ru/free_doc/doc_2016/prom16.pdf.

Rosstat. (2017) Russia in numbers: Short statistical compilation (p. 511). Moscow, Russia: Rosstat.

Rosstat. (2018) Russia in numbers: Short statistical compilation (p. 522). Moscow, Russia: Rosstat.

Russia: Foreign Trade Statistics (2017). According to the Federal Customs Service of Russia. Retrieved from http://ru-stat.com/date-Y2017-2017/RU/import/world/08430211.

Russia: Foreign Trade Statistics (2018). According to the Federal Customs Service of Russia. Retrieved from http://ru-stat.com/date-Y2013-2018/RU/import/world/08430211.

Russia: Statistics of foreign trade (2013). According to the Federal Customs Service of Russia. Retrieved from http://ru-stat.com/date-Y2013-2018/RU/export/world/08430211.

Sapir E. V., Karachev I. A., & Chzhan M. (2016). Export Potential of Russian Pharmaceutical Enterprises in Forming Regional Clusters. Regional Economy, 12(4), p. 1194–1204.

UN General Assembly (1987). UN General Assembly resolution 42/187 of December 11, 1987 “Report of the International Commission on Environment and Development”. Retrieved from http://www.un.org/en/ga/search/view_doc.asp?symbol=A/RES/42/ 187&referer=http://www.un.org/depts/dhl/resguide/r42_en.shtml&Lang=R.

1. Institute of Economics and Management in AIC, Russian State Agrarian University - Moscow Timiryazev Agricultural Academy, 49 Timiryazevskaya str., 127550, Moscow, Russia. ORCID: 0000-0002-4735-5496.

2. Accounting, Analysis and Audit Department, Financial University under the Government of the Russian Federation, 49 Leningradsky prospect, 125993, Moscow, Russia. ORCID: ORCID 0000-0001-7295-13726.