![]() ISSN 0798 1015

ISSN 0798 1015

![]() ISSN 0798 1015

ISSN 0798 1015

Vol. 40 (Number 30) Year 2019. Page 28

IVANOVA, Oksana E. 1; SIKYR, Martin 2 & ABRASHKIN, Mikhail S. 3

Received: 29/05/2019 • Approved: 30/08/2019 • Published 09/09/2019

ABSTRACT: The paper presents the methodology of cost management of industrial production based on the system of production rules where each rule has its own model of linking production, labor, innovation and financial potential. The structure of information was created and tested with emphasis on the specifics of the development of industrial production. A cognitive map of cost management of industrial production with cause-effect relationships among selected concepts in the analysis of complex situations was designed. |

RESUMEN: O artigo apresenta a metodologia de gestão de custos da produção industrial baseada no sistema de regras de produção, onde cada regra possui um modelo próprio de vinculação entre produção, trabalho, inovação e potencial financeiro. A estrutura da informação foi criada e testada com ênfase nas especificidades do desenvolvimento da produção industrial. Um mapa cognitivo do gerenciamento de custos da produção industrial com relações de causa e efeito entre conceitos selecionados na análise de situações complexas foi projetado. |

The essence of the development of the state lies in industrial production as a fundamental segment of the national economy. Industrial production accounts for about 30% of gross domestic product at basic prices, while the share of the mining industry is increasing. The domestic industry operates in a competitive environment with foreign producers, which is reflected in financial and economic results (see Factors restricting the activities of organizations of basic industries in 2017, 2018). This is confirmed by the presence of limiting factors of industrial production growth, economic uncertainty, the insufficient demand for products on the domestic market and the lack of human, financial and material resources (Kuvalin et. al., 2018). The development of industrial enterprises is important for the economic growth and increasing competitiveness (Romanova, 2018), the functioning of internal and external markets (Fang & Sun, 2018), and the development of high value-added production (Brenner & Dorner, 2017) and innovation activities (Kapp, 2017).

Cost management is the basis of the activities of business systems and has always been the subject of study by both Russian and foreign scientists (Becker & Gaivoronski, 2018; Hoozée & Ngo, 2018). A number of researches are based on an information-analytical system of cross-sectoral equilibrium of the input-output model (Ksenofontov, et. al., 2018; Mardalena, et. al., 2019; Miller & Blair, 2009), computable general equilibrium (CGE) models (Uzyakov, 2018), and dynamic stochastic general equilibrium (DSGE) models (Shirov, 2017), relating to the relationships among economic actors at the economic level, where the set of elements reflects the costs associated with the production of a particular type of product. The diversified nature of industrial production means the need to develop new methods of cost management to measure and control the performance of structural units under the constant influence of external and internal variables (Vidal-Carreras, Garcia-Sabater & Garcia-Sabater, 2017; Gupta & Vardhan, 2016). The authors of the paper analyzed existing methods of cost management and concluded that the existing studies have defined different criteria for cost evaluation depending on the research method.

However, some previous authors' studies Ivanova & Kozlova, 2014 concluded that using conventional cost control methods, it is difficult to focus on basic information and qualitatively describe the effect of addictions. Therefore, the classification of costs, usable for cost management of industrial production, was specified and extended. From this point of view, quality cost management of industrial production should directly influence production decisions and eliminate the risk of inefficient use of scarce resources. That is why the demand for quality methods of cost management of industrial production is constantly growing.

The goal of this paper is to define a system of production rules for cost management of industrial production, which will allow looking at cost management issues from a new perspective.

In the context of creating a new approach to business management, the ideology of management is changing and the task is to create a system of management that would allow specific objectives to be efficiently achieved. It should be noted that the current methodology of cost management is not sufficiently developed. There are no unified analytical tools for cost management. Therefore, the authors develop the methodology of cost management based on a systematic approach that includes three parts. The first part is based on the cluster approach, the grouping method, the discriminant analysis, and the method of multidimensional modelling based on the additive model. The second part includes the stages of cognitive modelling. The third part includes the system of production rules.

The data obtained during the study of the various methods make it possible both to evaluate the overall level of the development of industrial production and to identify the key problems and directions of the development by modifying the target indicators of activities based on the method of analysis and synthesis. The key idea of cost management of industrial production is based on the processing of information collected over a period of time. The study was focused on industrial activities of the Russian economy based on data published by the State Statistical Committee of Russian Federation (Rosstat) in 2007-2016. This time period is sufficient to identify key trends and validate the concept of this study because the structure of industrial production is changing slowly and it is possible to use average values of indicators in calculations. The authors identified the studied objects on the basis of selected blocks in accordance with selected indicators and defined the main characteristics of the features and relations among them. To emphasize cause-effect relationships, the information obtained was structured on the basis of a cognitive approach. The authors defined components of the cognitive map, including critical variables, control objects, and target factors. Based on the method of deduction and induction, the methodology of cost management of industrial production is proposed using the system of production rules for decision making and selection of the appropriate solution.

To understand the genesis of the dynamic processes of the development of industrial production and to analyze the problems of cost management, it is necessary to focus on the source information and the qualitative character of its dependences, which is difficult with generally accepted methods of management. There is no doubt that in order to define the essence and context, it is necessary to determine the position of industrial production and its economic potential (Ayvazyan et. al., 2018). Studies by the Institute of Economic Forecasting of the Russian Academy of Sciences show that the creation of economic models requires data that reflect the dynamic and structural characteristics of economic development (Shirov, 2017; Shirov, 2019). A comprehensive review of the development of industrial production requires detailed analysis of production processes, their interaction with working factors, mechanisms of development of innovation processes and financial situation of industrial businesses (He, Zhu & Yang, 2017). In addition to the traditional methods of cost management of industrial production, the authors have developed a system of indicators in the context of industrial activities of the Russian economy, which allows comparing the indicators in a common space.

In the context of defining priorities of the development of industrial production, it is necessary to create new sources of growth based on the development of technological, labor and innovation resources. Modern trends in global technological development increase the demand for quality workforce (Borgersen & King, 2016). The current differences in demand and supply on the Russian labor market are associated with an increase in the average age of employees, changes in socio-demographic characteristics or inconsistencies in employment and education (Korovkin, 2018; Lenchuk, 2018; Romanova, 2018). Effective management of available resources through gained knowledge enables mobilizing innovation potential of industrial business. The support of innovation activities is the main source of economic growth, which enables increasing labor productivity and efficiency of production processes and ensures the competitiveness of the economy (Zhukov et. al., 2018). However, one of the main problems of the development of innovation activities is their financing (Prokhorova et. al., 2016; Tsatsulin, 2018). The logical consequence is the need to evaluate the financial activities of industrial businesses (Alikaeva et. al., 2016; Malkina, 2016).

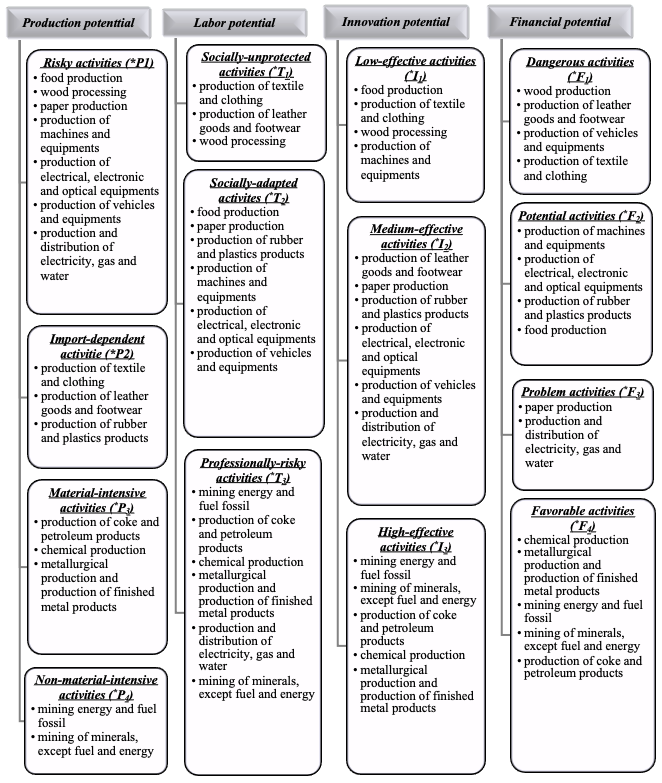

Therefore, the evaluation of the current state of industrial production was made with regard to its production potential, labor potential, innovation potential, and financial potential. Figure 1 shows the proposed structure of these potentials and industrial activities of the Russian economy usable for cost management of industrial production. Each of these potentials represents an evaluation of indicators that characterize the development of industrial production and thus the impact on production costs (see table 1).

Table 1

Production potential of industrial activities of

the Russian economy on average for 2007-2016

Indicator |

Risky activities |

Import-dependent activities |

Material-intensive activities |

Non-material-intensive activities |

Production index (%) |

100.31 |

105.41 |

101.80 |

101.67 |

Coefficient of renewal of fixed assets |

11.02 |

15.13 |

14.52 |

15.12 |

Degree of depreciation of fixed assets (%) |

41.89 |

40.19 |

40.83 |

47.22 |

Intensity of production (%) |

59.54 |

46.22 |

61.58 |

26.07 |

Import share in the volume of products shipped (%) |

32.76 |

27.65 |

7.70 |

0.47 |

Export share in the volume of products shipped (%) |

6.69 |

0.21 |

68.70 |

86.17 |

Investment per worker (thousand rubles/person) |

175,84 |

61,73 |

323,32 |

1293,16 |

Source: The calculation was based on data provided by the State Statistical

Committee of Russian Federation (Rosstat), the codes classifier OKVED OK 029-2007

The analysis of "risky" industrial activities in the production potential group showed weak competitors, limited product ranges, poorly developed markets of key products, or limits in the production of some high-tech components. As a result, there is no stable, effective domestic demand due to the large volume of imports on the volume of products supplied. Obsolete fixed assets and underdeveloped technologies cause a high energy intensity of industrial production, which reduces its efficiency and increases its dependence on energy supply. In this context, it can be concluded that there are risks of dependence of industrial production on the supply of imported equipment due to the lack of financial resources, the cyclical demand for final products, or the problem of non-fulfilment of business agreements.

Given the dependence of production potential on imports, the results of the analysis show that the structure of industrial production varies depending on the following factors:

• weakly developed market infrastructure, distribution network and business cooperation with neighboring countries;

• high dependence of industrial production on imports;

• low consistency of industrial production, product range and product quality with demand of the Russian and world markets;

• low investment activity;

• obsolete fixed assets and underdeveloped technologies.

The industrial production depends on the stability of supplies of raw materials and energy, their quality and price. In addition, as a result of the growing gap between consumer requirements for the quality of final products and the ability of industrial businesses to meet them, the costs of advertising, certification and standardization have been increasing in order to promote the image of industrial businesses. High costs, especially high energy consumption, are typical for "material-intensive" industrial production and therefore there is reason to believe that there is a limited supply and low quality of raw materials, leading to a disruption of the raw material base reproduction mechanism and a reduction in production volumes. In the long term, the authors propose to apply a systematic approach to cost management, based on the development of new technology sectors, the modernization of technologies, and the introduction of cost-effective technologies. The authors also suggest improving customs regulatory procedures and deepening integration processes with the countries of the Commonwealth of Independent States and the European Union.

The results draw attention to the development of "non-material-intensive" industrial production, which includes industrial activities with a high level of automation. The development of industrial production requires the development of key technology sectors, the technological renewal of production capacity, the introduction of resource- and energy-saving technologies, the stimulation of private businesses to participate in the exchange trade, the active participation in the international negotiation process, the balance of interests of importers and exporters, or the development of transport infrastructure.

Figure 1

Structure of potentials and industrial activities of the Russian economy

usable for cost management of industrial production (* symbols)

Source: The data provided by the State Statistical Committee of

Russian Federation (Rosstat), the codes classifier OKVED OK 029-2007

The analysis of "socially-unprotected" industrial activities in the labor potential group showed a low level of labor productivity, a lack of highly skilled professionals and a lack of opportunities to create the conditions necessary to attract young professionals. The lack of quality workforce, unfavorable working conditions, or the hidden unemployment leads to the outflow of labor, the underemployment, or job reorganizations. "Socially-adapted" industrial activities are faced with the insufficient development of internal infrastructure or increasing social tensions in individual regions. This may be indirectly influenced by knowledge, skills and abilities of employees, taking into account the requirements of the innovative economy and the development of new organizational forms of management. "Professionally-risky" industrial activities are faced with unfavorable working conditions, the lack of specialists or limited opportunities for retraining of employees. The development of these industrial activities requires the improvement of working conditions and employee training, especially young specialists (see table 2).

Table 2

Labor potential of industrial activities of the

Russian economy on average for 2007-2016

Indicator |

Socially-unprotected activities |

Socially-adapted activities |

Professionally-risky activities |

Proportion of trained employees (%) |

7.03 |

15.37 |

22.52 |

Average age of the average number of employees (years) |

48.00 |

47.00 |

46.00 |

Employee retirement rate (%) |

43.90 |

35.54 |

26.02 |

Index of non-compliance with normal working conditions |

0.17 |

0.25 |

0.61 |

Index of compensations for work in unfavorable working conditions |

0.14 |

0.28 |

0.66 |

Index of individuals unable to work |

0.57 |

0.60 |

0.61 |

Source: The calculation was based on data provided by the State Statistical Committee

of Russian Federation (Rosstat), the codes classifier OKVED OK 029-2007

The analysis of "low-effective" industrial activities in the innovation potential group showed low share of innovative products and a lack of policies to support innovation activities and their financing. Low investment in technological innovation limits the achievement of expected scientific and technological development. "Medium-effective" industrial activities are faced with similar problems. On the other hand, "high-effective" industrial activities are characterized by the active development of new investment projects, the introduction of new technologies and the strengthening of global market positions (see table 3).

Table 3

Innovation potential of industrial activities of the

Russian economy on average for 2007-2016

Indicator |

Low-effective activities |

Medium-effective activities |

High-effective activities |

Proportion of businesses introducing technological innovation (%) |

8.82 |

11.84 |

15.56 |

Proportion of businesses introducing organizational innovation (%) |

3.24 |

4.68 |

6.49 |

Proportion of businesses introducing marketing |

2.70 |

2.78 |

2.98 |

Proportion of businesses introducing environmental innovation (%) |

27.09 |

29.53 |

37.76 |

Proportion of federal budget financing in the total cost of technological innovation (%) |

2.25 |

5.97 |

1.51 |

Source: The calculation was based on data provided by the State Statistical

Committee of Russian Federation (Rosstat), the codes classifier OKVED OK 029-2007

The analysis of "dangerous" industrial activities in the financial potential group showed a low level of business activities, a lack of working capital and high financial costs. "Potential" industrial activities are characterized by stable business activities. "Problem" industrial activities are characterized by unprofitable business activities. "Favorable" industrial activities lack a unified state strategy aimed at developing cooperation between government agencies at all levels (see table 4).

Table 4

Financial potential of industrial activities of the Russian economy on average for 2007-2016

Indicator |

Dangerous activities |

Potential activities |

Problem activities |

Favorable activities |

Current ratio (%) |

125.84 |

127.66 |

139.54 |

164.78 |

Equity ratio (%) |

26.01 |

36.07 |

57.33 |

54.42 |

Turnover of current assets (days) |

198.55 |

169.84 |

119.60 |

155.48 |

Maturity of payables (days) |

91.40 |

80.76 |

56.10 |

45.24 |

Profitability of sold products (%) |

5.12 |

9.84 |

8.18 |

28.42 |

Share of unprofitable businesses (%) |

1.37 |

1.25 |

3.70 |

2.07 |

Source: The calculation was based on data provided by the State Statistical Committee

of Russian Federation (Rosstat), the codes classifier OKVED OK 029-2007

The presented structure of production, labor, innovation, and financial potential of industrial activities usable for cost management of industrial production can serve as an objective guide for the formulation of effective strategies and policies over time for state and regional institutions.

An important aspect that should be taken into account when managing costs of industrial production is the identification of potential problems based on a cognitive approach to the analysis of complex situations. A cognitive map of the situation is an oriented weighted graph in which the peaks correspond to the underlying factors of the situation and the cause-effect relationships are highlighted, reflecting the influence of each factor on the selected concepts (Maksimov, Kornoushenko & Kachaev, 2007; Waris, Sanin & Szczerbicki, 2018). The sets of measures in the table 5 are suggested by the authors as concepts describing the mechanism of cost management of industrial production.

Table 5

Set of concepts of cognitive map of cost

management of industrial production

Name |

Symbol |

Name |

Symbol |

Name |

Symbol |

|

Control objects |

Target indicators |

|||

Research and development |

UV1 |

Costs of energies |

TZ1 |

Average annual value of fixed assets |

PF1 |

Industrial design |

UV2 |

Cost of depreciation |

TZ2 |

Production of goods and services |

PF2 |

Purchase of machines and equipment |

UV3 |

Cost of process innovations |

TZ3 |

Export of industrial products from Russia |

PF3 |

Purchase of new technologies (patents, licenses) |

UV4 |

Environmental costs |

TZ4 |

Import of industrial products to Russia |

PF4 |

Environmental measures |

UV5 |

Cost of raw materials |

TZ5 |

Environmental impact factor |

PF5 |

Introduction of new or radically modified organizational structures |

UV6 |

Cost of product innovations |

TZ6 |

Average annual number of employees of industrial businesses |

TF1 |

Introduction of logistics systems and purchase of resources |

UV7 |

Administrative costs |

OZ1 |

Average monthly wage of employees of industrial businesses |

TF2 |

Implementation of corporate structures |

UV8 |

Representation costs |

OZ2 |

Number of industrial businesses |

TF3 |

Implementation of employee development activities |

UV9 |

Costs of organizational innovations |

OZ3 |

Average annual working time |

TF4 |

Application of quality control systems and certifications of goods and services |

UV10 |

Wages without social security contributions |

OZ4 |

Coefficient of working conditions |

TF5 |

Creation of new forms of strategic alliances and partnerships with consumers and suppliers |

UV11 |

Costs of training |

OZ5 |

Innovative products |

IF1 |

Application of outsourcing services |

UV12 |

Costs of housing |

OZ6 |

Proceeds from the sale of goods and services of industrial businesses |

FF1 |

Application of pricing strategies for the sale of goods and services |

UV13 |

Costs of social security |

OZ7 |

Current assets of industrial businesses |

FF2 |

Expansion of consumers and markets |

UV14 |

Costs of advertising |

MZ1 |

Receivables of industrial businesses |

FF3 |

Introduction of changes in the design of goods and services |

UV15 |

Costs of external services |

MZ2 |

Accounts payable of industrial businesses |

FF4 |

Costs of marketing innovations |

MZ3 |

||||

Source: authors

The authors developed a cognitive map of cost management of industrial production in the form of a character chart in which the peaks represent fundamental processes and their parameters and edges represent signs "+" or "-". In this model, the cognitive map represents a subjective view of cost management of industrial production. Based on the analysis of the cause-effect relationships, the following conclusion can be drawn: the introduction of energy-saving technologies, the modernization of technological infrastructure and the development of technological production will lead to the progress of the material and technical base of industrial production and the increase in the production of goods and services. The support of research and development, the implementation of pilot projects, the preservation of the system of bilateral international agreements, the intensification of integration processes with foreign countries or the achievement of the balance of interests of importers and exporters will contribute to the development of investment activities of industrial businesses, the development of market infrastructure and the reduction of the dependence of industrial production on imports. The development of human resources, the modernization of production processes and the improvement of working conditions will increase the interest of quality people in working in industrial businesses. The development of modern technologies, high-tech products and private-state partnerships based on technology platforms will increase the share of innovative products in total industrial production. The change of target factors of the development of industrial production based on cost management will continue on the basis of a scenario approach taking into account the complex management activities and external conditions of the economic development, using a defined cognitive map.

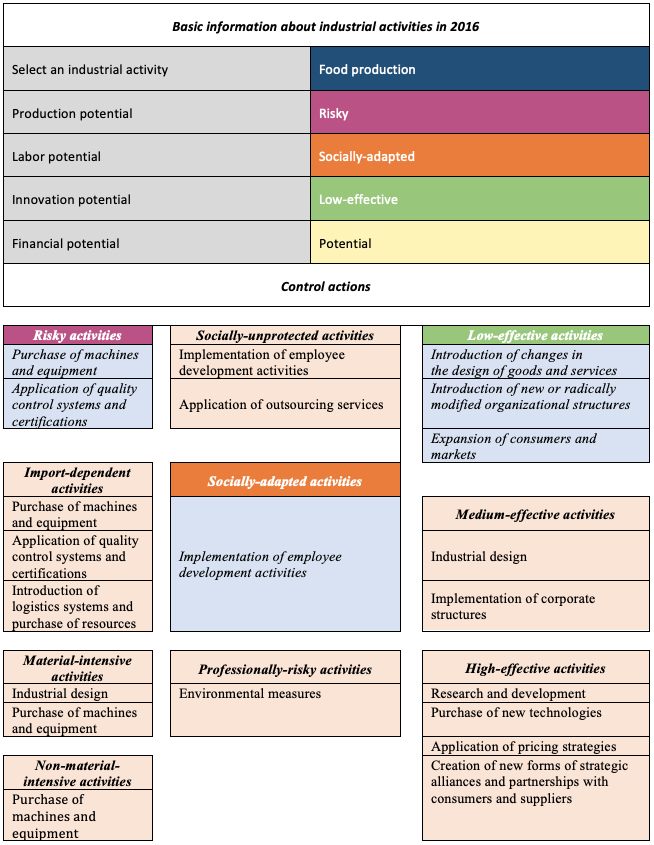

Figure 2 shows a fragment of an information-analytical system of cost management of industrial production in the context defined potentials and industrial activities of the Russian economy usable for cost management of industrial production.

The author's vision of the methodology is to build an information core based on the creation of a data base and a knowledge base. The information obtained from the information-analytical system allows to identify a specific production activity to the appropriate potential group. Based on the definition of the basic requirements of the examined situation, its conditions and limitations, the main control actions associated with the cost management are identified and possible changes in the objective development of the situation are identified. The authors believe that the production potential is considered to be a constant value when determining the frequency of defined potential combinations.

Figure 2

A fragment of an information-analytical system

of cost management of industrial production

Source: authors

The total number of combinations of allocation of industrial activities to a potential group over the observed period is 128. The most common combinations are as follows:

• 17 combinations: production potential group – "risky" industrial activities, labor potential group – "socially-adapted" industrial activities, innovation potential group – "low-effective" industrial activities, financial potential group – "dangerous" industrial activities (P1 → T2 → I1 → F1);

• 16 combinations: production potential group – "risky" industrial activities, labor potential group – "socially-adapted" industrial activities, innovation potential group – "high-effective" industrial activities, financial potential group – "dangerous" industrial activities (P1 → T2 → I3 → F1);

On average over the observed period, in the labor potential group, 3 units were included among "socially-unprotected" industrial activities, 10 units were included among "socially-unprotected" industrial activities, and 2 units were included among "professionally-risky" industrial activities. In the innovation potential group, 6 units were included among "low-effective" industrial activities, 2 units were included among "medium-effective" industrial activities, and 9 units were included among "high-effective" industrial activities. In the financial potential group, 9 units were included among "dangerous" industrial activities, 3 units were included among "potential" industrial activities, 2 units were included among "problem" industrial activities, and 3 units were included among "favorable" industrial activities.

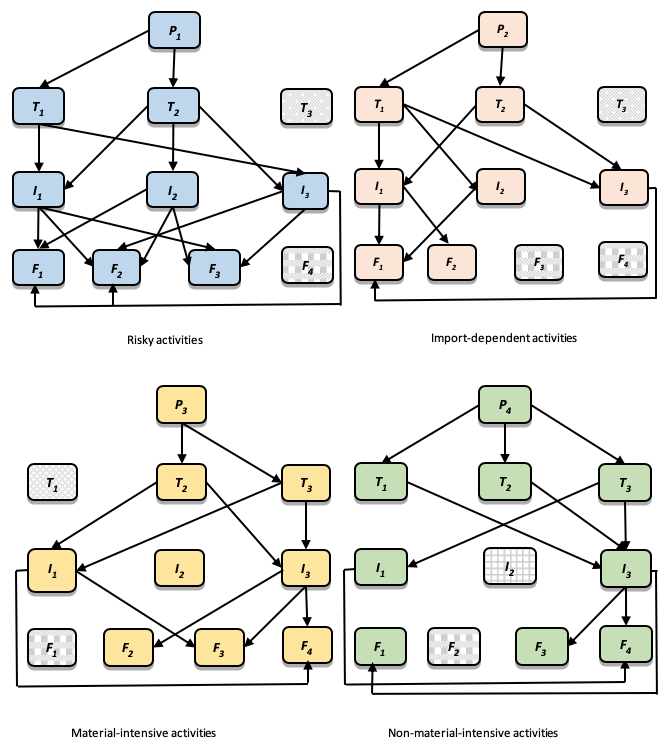

Taking into account defined control actions, trends characterizing the current situation, desired objectives of the development of fundamental factors, a set of control actions to change the situation, and a system of monitored costs illustrating the activity of processes, the authors formulated a system of production rules reflecting the relationship between defined potential groups in a temporary time interval (see figure 3).

In terms of "risky" industrial activities, the authors conclude that these activities have a low level of production index as well as a low level of cost recovery and therefore they cannot enter the "favorable" financial zone (P1 → F4). A low level of equipment use is reflected in a low level of labor productivity, which is related to labor costs, so a combination with "professionally-risky" industrial activities is not acceptable (P1 → T3). The shortage of skilled employees reduces the share of technological innovation and innovative products in total industrial production. The employee turnover limits the implementation of organizational innovations (T1 → I2). The financial capacity of individual industrial activities ensures employee social security only at the level of working conditions (T1 → F3).

The dominance of import over export does not allow "import-dependent" activities to ensure sufficient turnover of current assets and profitability of products. The dominance of short-term liabilities compared to current assets does not ensure the solvency of businesses with respect to business conditions (P2 → F3; P2 → F4). The low labor productivity does not allow saving raw materials and leads to poor technical equipment (P2 → T3). The favorable trend of increasing the share of innovative products in total industrial production reflects employees' interest in the results of their work while ensuring an optimal level of average monthly wages and working conditions as a result of organizational and environmental measures resulting from the development of industrial production (T2 → I2).

Material capacity of production potential of industrial production does not allow lower current ratio, long-term turnover of current assets, or increase of slow assets over marketable assets (P3 → F1). In order to achieve the desired labor productivity, industrial businesses should have enough full-time employees and should ensure their systematic training to develop their knowledge, skills and abilities (P3 → T1; P3 → I2). The innovation activities within "material-intensive" industrial activities have a positive impact on the assets, liquidity and solvency of industrial businesses and their business activities (I1 → F2).

The main management activity related to costs of "non-material-intensive" industrial activities is the purchase of machines and equipment, which does not correspond to the "medium-effective" industrial activities within the innovation potential group. With regard to the export and raw materials orientation of the industrial production, the authors believe that this sector is not a leader in terms of the share of innovative products in total of industrial production (P4 → I2). Therefore, assets must be kept at the right level (P4 → F2). The high level of professionalism and qualification of employees contributes to the development of innovative activities and employee engagement (T1 → I1). At the same time, the contribution of employees to the development of industrial production is not able to prevent the loss of industrial business (T1 → F3) and achieve an acceptable level of profitability of the products sold, optimal asset turnover time and dept repayment (T1 → F4). The significant division of labor within "socially-adapted" industrial activities, as well as the effort to develop knowledge, skills and abilities of employees, cannot affect the realization of innovation activities of industrial businesses within the labor potential group (T2 → I1). Average cross-sectoral differences within "socially-adapted" and "professionally-risky" industrial activities do not affect the relation to risk with regard to financial conditions (T2 → F1; T3 → F1). The need of innovation activities within "low-effective" industrial activities cannot be ensured by "dangerous" and "problem" industrial activities within the financial potential group (I1 → F1; I1 → F3).

Figure 3

Linking units of cost management of industrial

activities to define the system of production rules

Source: authors

The results show the distribution of production, labor, innovation and financial potential in order to manage costs of industrial production based on the information-analytical system of control actions.

The authors present one of the possible approaches to cost management of industrial production. This approach seems to be more specific and sophisticated than the approaches presented in other studies on cost management. The main characteristic of the research is the review of available theoretical knowledge and generally accepted management approaches, with a focus on finding an acceptable solution to the problem of cost management. To achieve the maximum economic effect, a methodology of cost management of industrial production based on a structure of specific potentials (production, labor, innovation, financial) and related industrial activities of the economy were defined. It was shown that, on the basis of structuring information, it is possible to create a unified information base for identifying specific problems that limit the development of industrial production. Cost control of industrial production based on a system of production rules allows defining a set of control actions to achieve target indicators. The methodology is based on economic laws, logical data formalization, and mathematical interpretation of the axiomatic nature. The results make it possible to explain the observed trends based on defined assumptions. The research meets the reliability criterion based on compliance with official statistics provided by the Federal State Statistic Service of the Russian Federation.

The proposed system of production rules represents a basic methodology of cost management of industrial production. The results confirm the assumption that the decomposition of potentials of industrial production determines the influence of control actions on the value of costs in order to achieve the target indicators through the combination of block nodes. The system of production rules will enable a scenario approach to cost management of industrial production, taking into account current trends, underlying factors, control actions, target indicators and monitored costs. The application of this system implies modeling the current situation in three ways with regard to stability or instability of the external environment: the prediction of the development of the current situation with a full set of control actions; the prediction of the development of the current situation with a variable set of control actions, including high-cost, medium-cost, and low-cost control actions; the prediction of the development of the current situation with absence of control actions. These results can be focused on confirming the nature of the identified trends, taking into account differences in time.

Alikaeva, M. V., Novoselova, N. N., Kaziyeva, B. V., Gurfova, R. V. and Kerefova, L. G. Assessment of Potential Companies Based on Performance and Financial Component under Conditions of New Economic Growth Model. International Journal of Economics and Financial, 6, 2016, pp. 6-13.

Ayvazyan, S. A., Afanasyev, M. Yu. and Kudrov, A. V. Indicators of economic development in the basis of characteristics of regional differentiation. Applied Econometrics, 50, 2018, pp. 4-22.

Zhukov, R. A., Polyakov, V. A. and Vasina, M. V. The impact of innovation, labor and capital on the gross regional product as an indicator of sustainable development of the regions: regions of the Central Federal District and the Tula region. Research and Development. Economy, 5, 2018. pp. 4-9.

Ivanova, O. E. and Kozlova, M. A. Structuring information development of the industrial sector of the economy to manage costs. Online Journal of Science, 23, 2014, pp. 50-51.

Korovkin, A. G. Macroeconomic assessment of the state and prospects for the development of employment and the labor market in Russia. Journal of the New Economic Association, 37, 2018, pp. 168-176.

Ksenofontov, M. Yu., Shirov, A. A., Polzikov, D. A. and Yantovsky A. A. Estimation of multiplicative effects in the Russian economy based on the input-output tables. Problems of Forecasting, 167, 2018, pp. 3-13.

Kuvalin, D. B., Moiseev, A. K. and Lavrinenko P. A. Russian enterprises at the end of 2017: the absence of generally significant economic changes and progress in mechanical engineering. Studies on Russian Economic Development, 168, 2018, pp. 105-121.

Lenchuk, E. B. Formation of Russia's industrial policy in the context of the challenges of new industrialization. Journal of the New Economic Association, 39, 2018, pp. 138-145.

Maksimov, V. I., Kornoushenko, E. K. and Kachaev S. V. Cognitive Technologies to Support Management Decision Making. Moscow: Institute of Control Sciences (РАН), 2007.

Malkina, M. Yu. Contribution of regions and industries to the financial instability of the Russian economy. Terra Economicus, 16, 2016, pp. 118-130.

Mardalena, M., Ardi, A., Suhel, S., Sri, A. and Harunurrasyid, H. How Leading Economic Sectors Stimulate Economic Growth, Income and Labor Absorption? Input - Output Approach. International Journal of Economics and Financial Issues, 9, 2019, pp. 234-244.

Miller, R. E. and Blair, P. D. Input-Output Analysis: Foundations and Extensions. Cambridge University Press, 2009.

Prokhorova, M. P., Prodanova, N. A., Reznichenko, S. M., Vasiliev, V. P. and Kireev, V. S. Innovation Performance and its Influence on Enterprise Economic Efficiency in the Market. International Journal of Economics and Financial Issues, 6, 2016, pp. 78 – 83.

Romanova, O. A. Priorities of Russia's industrial policy in the context of the challenges of the fourth industrial revolution. Economy of Region, 14, 2018, pp. 420-432.

Uzyakov, M. R. The use of intersectoral tools in the analysis of the dynamics of the Russian economy in 1991-2013. Problems of Forecasting, 168, 2018, pp. 13-17.

Factors restricting the activities of organizations of basic industries in 2017. Moscow: National Research University, Higher School of Economics, 2018.

Shirov, A. A. The role of instrumental methods of analysis and forecasting to substantiate economic policy. Problems of Forecasting, 161, 2017, pp. 121-126.

Shirov, A. A. Socio-economic forecast as a mechanism for strategic economic management. Budget, 2019.

Vidal-Carreras, P. I., Garcia-Sabater, J. P. and Garcia-Sabater, J. J. A practical model for managing inventories with unknown costs and a budget constraint. InternationalJournalofProductionResearch, 55, 2017, pp. 118-129.

Becker, D. M. and Gaivoronski, A. A. Optimisation approach to target costing under uncertainty with application to ICT-service. InternationalJournalofProductionResearch, 56, 2018, pp. 1904-1917.

Hoozée, S. and Ngo, Q.-H. The Impact of Managers’ Participation in Costing System Design on Their Perceived Contributions to Process Improvement. EuropeanAccountingReview, 27, 2018, pp. 747-770.

Gupta, P. and Vardhan, S. Optimizing OEE, productivity and production cost for improving sales volume in an automobile industry through TPM: a case study. InternationalJournalofProductionResearch, 54, 2016, pp. 2976-2988.

Brenner, T. and Dorner, M. Is there a life cycle in all industries? First evidence from industry size dynamics in West Germany. Applied Economics Letters, 24, 2017, pp. 289-297

Waris, M. M., Sanin, C. and Szczerbicki, E. Smart Innovation Engineering: Toward Intelligent. Industries of the Future. Cybernetics and Systems, 49, 2018, pp. 339-354.

Tsatsulin, A. Financing Innovation Development in the Context of Foreign Experience and Domestic Practice. Problems of Economic Transition, 60, 2018, pp. 578-596.

Kapp, P. H. The artisan economy and post-industrial regeneration in the US. Journal of Urban Design, 22, 2017, pp. 477-493.

Fang, H.-Y. and Sun, Q.-M. Spatial econometric analysis of the relationship between economic growth and industrial structure: Industrial complex network perspective. Journal of Interdisciplinary Mathematics, 21, 2018, pp. 1357-1361.

He, C., Zhu, S. and Yang, X. What matters for regional industrial dynamics in a transitional economy? AreaDevelopmentandPolicy, 2, 2017, pp. 71-90.

Borgersen, T.-A. and King, R. M. Industrial structure and jobless growth in transition economies. Post-CommunistEconomies, 28, 2016, pp. 520-536.

1. Department "Accounting, analysis and audit", FSBEI HE "Kostroma State Agricultural Academy", Russia. Contact e-mail: oksivanova44@mail.ru

2. Masaryk Institute of Advanced Studies, Czech Technical University in Prague, Czech Republic. Contact e-mail: martin.sikyr@cvut.cz

3. Institute of project management and engineering business, University of Technology, Russia. Contact e-mail: abrashkinms@mail.ru